My Take on YRC Worldwide’s 4th Quarter

I was a little surprised by the reaction to the release of YRC Worldwide’s 4th quarter earnings. While the stock moved about 6% higher, I thought it would have moved more. In the first 15 minutes of trading when the stock ran up to $7.40, that seemed about right to me. But it did not stay there, quickly falling back below $7 and settling at $6.81.

I was impressed by how good the results were. I didn’t expect as much improvement as the company showed, especially what occurred at YRC Freight (the company owns 3 regional trucking businesses which they consolidate as their “regional” segment, and a nationwide LTL business called YRC Freight).

Thinking about why the share price didn’t reflect my enthusiasm, I wonder whether investors hesitated because of the poor headline EPS. The company lost $4.53 per share in GAAP terms and that does not inspire confidence in a stock that is trading for less than $7.

But that $4.53 is the result of a couple things. First, the results were impacted by a $30 million equity investment impairment (which works out to $3.95 per share). Second, the 4th quarter is seasonally weak.

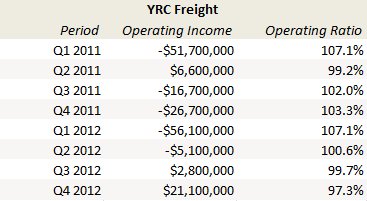

The big story of the fourth quarter was the improvement at YRC Freight. This business has been a laggard over the first year and a half of the restructuring. While the regional trucking businesses have been performing well, Freight has struggled with costs and mix. Yet if you look at the Q4 year over year, the improvement at Freight is impressive. Operating income improved from a loss of 26.7 million in Q4 2011, t0 a profit of 21.1 million this year. The operating ratio (measured as expenses divided by revenues) improved from 103.3% to 97.7%.

The following table illustrates the improvement at Freight over the past couple of quarters:

In my original post on YRC Worldwide, “A Very Leveraged Bet on Trucking“, I pointed out that the investment thesis for the company lay in the possibility (not necessarily probability) of a turnaround and the tremendous leverage that the common stock had to that event. I wrote at the time:

YRC Worldwide has a little more than 7 million shares outstanding right now. The lowest conversion price of any of the convertible debt is $14, so it can be ignored for the time being (if I got $14 out of the stock it would be time to re-evaluate). As far as earnings go, a 10 basis point move in the operating ratio of the company as a whole creates about $4.5 million in income. That is $0.64 per share. It doesn’t take much of a change in the operating results to create big swings in earnings.

Excluding one time items, the company reported consolidated operating income (so from both the Regional and YRC Freight segments) in Q4 of $21 million. That is about $3 per share for the quarter. Now this operating income was more than eaten up by interest costs of $39 million. But the company is getting closer to that magical break-even point, and when they do it does not take much above break-even to begin generating significant earnings on a per share basis.

While the first quarter is also a traditionally slow period, and will likely show only a small profit at best and more likely a small loss, if the company can continue to improve on its performance over the first half of this year, the second and third quarter numbers could be quite eye-popping. If the company can report $1 eps in Q2 or Q3, do you think the market will be able to hold the stock down? I have my doubts of that.

Keep in mind that the risk with this stock remains extremely high. In the long-term the company faces significant challenges. The debt, the pension obligations, the union; I have no misconceptions about the tremendous work the company has ahead of it. I talked about each of these challenges in some detail in my previous post.

Yet the street likes a good turnaround story, and one that can deliver large EPS numbers is bound to garner attention. I wouldn’t underestimate the power of momentum, both in a stock and in a business. And while I am not going to sit here and try to forecast what I think will happen, I do think the odds are improving that what does happen is going to be positive. I don’t think that the 5% move in the stock on Friday has begun to reflect that. The stock, after all, still trades below what I bought it for a little over a month ago,even though the story has grown much longer legs. So I bought more.

Now I am sure the naysayers will think me crazy (I don’t know if I have gotten as much negative feedback about any name I have written about as I did after my original write-up of YRC Worldwide), and so be that. I try to act based on changes to the evidence and the change in the fourth quarter was undeniably positive. YRC Worldwide is no longer a curiosity sized position for me; it is fully sized. It is now as large of a position for me as Arkansas Best. I remain cognizant of the risks and wary of the long-term, but for the moment am compelled by the upside of a turnaround that is not reflected in the current stock price.

I completely agree with your take on YRCW. I currently own about a good deal of shares so I’m clearly biased. However, the company has gone through a major metamorphosis. I honestly didn’t expect great things out of Q4 (or Q1 for that matter) because it is a seasonally weaker quarter and Hurricane Sandy really put a dent in business. However, the fact that they were able to generate better operating income than Q3 and are within a stone’s throw of generating a net profit, I believe come Q3 2013 they will be able to post a $1+ EPS quarter. And I don’t think the market is even remotely prepared for this. In fact, I wouldn’t be surprised to see them post a $2 EPS quarter, benefited by continued operating ratio improvements and a rollout of their handheld technology to their drivers which should result in continued improvements in on time deliveries and overall operating efficiency. This is the most leveraged company I have ever seen in my entire life: if they are able to grow revenues 2% in 2013 they could see a $5 EPS improvement.

Ultimately, I do see the company returning to positive net profit in 2013 and I believe the company can ultimately generate $200 Million in free cash flow, which will enable them to pay down their debt and within 2 to 4 years I think the company will trade at a $1.5 Billion market cap (roughly $65 to $70 per diluted share).

Best of luck on your trade.

Thanks – lets hope it plays out this way. I certainly think there is a chance it will.

Just based on how the stock is trading, I think it’s wise to expect a test of the $5 lows first to get enough people off board before it can make its move. Perhaps that would coincide with a weak Q1 earnings report.

excellent call!