Week 85: Some Short Thoughts on Nam Tai, Yellow Media, Radian Group and Atna Resources

Portfolio Performance

Update

I finished a post over the weekend giving some thoughts about the macro-environment and how it pertains to my portfolio. As a consequence of the conclusions drawn, my portfolio has been growing and my cash level decreasing, to the point where I have now been on margin for the last month and a half. Right now I have about 11% margin. While I am typically wary of using margin, when I look at what I own there are no stocks that I feel compelled to reduce. We’ll see if this turns out to be folly. This is, however, about as much risk as I’m comfortable with, so any stocks added hereon will have to be balanced by equivalent removals. And as per the strategy I profess, I will sell without remorse if the market turns abruptly.

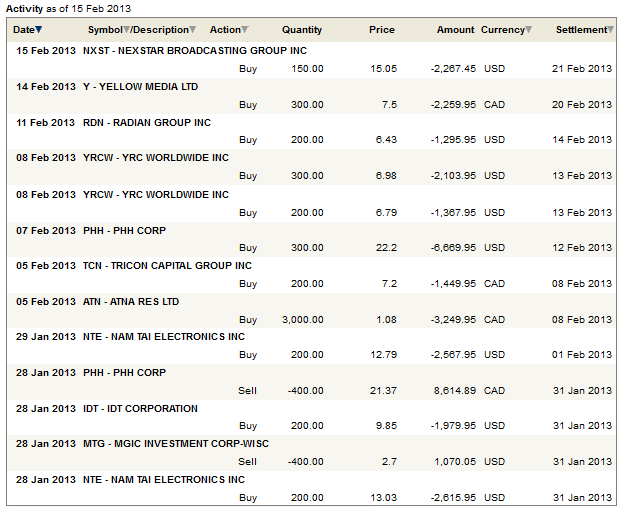

On to some of the moves I made over the past 3 weeks.

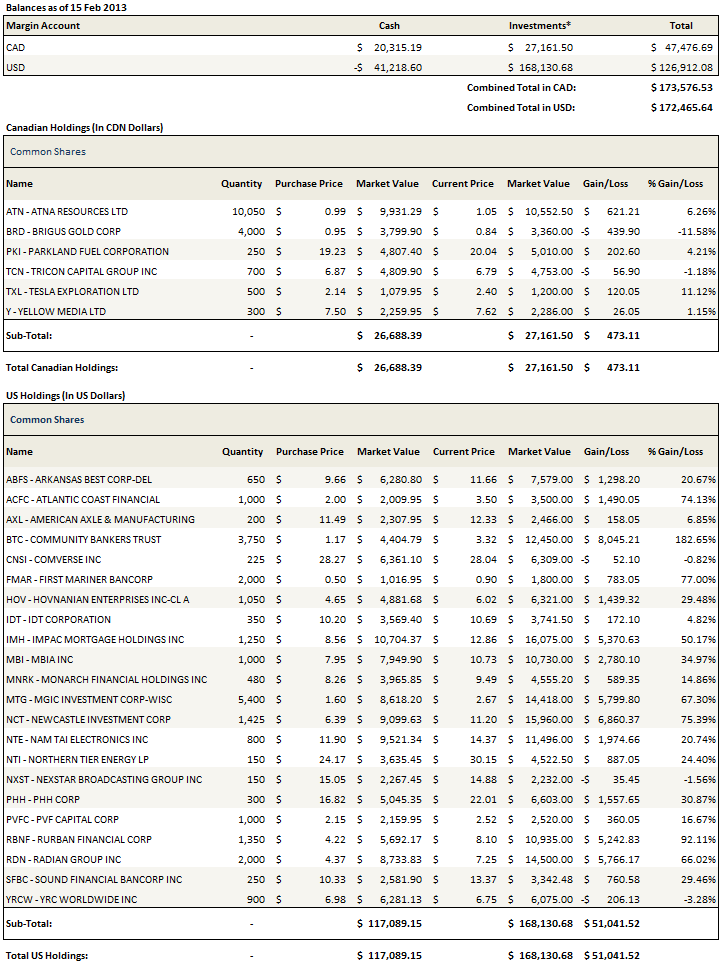

Adding to Nam Tai (NTE)

When Nam Tai released earnings on January 28th the stock was up over $2 in pre-market and I thought we were off to the races. But it turned out to be short-lived; the stock dropped during the conference call, purportedly on concerns about gross margins. While gross margins were 10.5% in the fourth quarter, on the conference call the company guided for gross margins of 7% for the full year.

In my original post on Nam Tai I made some projections about sales and gross margins. For those projections I assumed gross margins in the 6% range. This was based on the expectation that Tablet LCD Module margins would be in the 6-8% range and that Smart Phone LCD Module margins would be in the 5-7% range. So guidance of 7% doesn’t seem unreasonable.

And I think that if anything the guidance is going to turn out to be low. I’ve already noted that margins in Q4 were much higher than 7%. A fair question is why? I think that the most likely answer is that management has been and continues to be lowballing their margin estimate. There was a good article on Seeking Alpha after the earnings release that discussed managements historical tendency to do just that.

The other thing that was mentioned on the call and mostly forgotten was that at full capacity revenues would be double what they were in Q1. It works out to about $900 million in revenues a quarter. The company expects to be at full capacity by year end.

If you start doing the math on that, assume a run rate of $900 million per quarter and 7% gross margins, you get a heck of a lot higher earnings than what is priced into the stock currently.

I added significantly to Nam Tai when it dropped below $13 after the quarter. I don’t really understand what the expectations were or how the quarter disappointed them, but from what I can see it does not look like the stock price is even close to pricing in the upcoming earnings.

Buying Yellow Media (Y.to)

I’m planning on a more lengthy write-up on Yellow Media so I’ll keep things short for now. Yellow Media is in the phone book business. I’ll just let that one sink in for a second…. Ok, so yes, they are in the phone book business and the phone book business is a terrible business. So terrible that the company had to restructure its debts last year even while generating significant free cash flow. You know its a bad business when you are getting pressure to restructure while still generating positive cash.

But here’s the thing. Now that they have restructured there is significantly less debt held by the company, down from $2.1 billion pre-restructuring to $800 million in senior notes and another $87 million in convertible debentures now, offset by about $100 million of cash. The company is still churning out significant free cash flow; I calculated that in 2012, if you remove all the one time restructuring charges, normalize interest charges to the post-restructuring level and assume a 27% tax rate, the company would have generated over $250 million in free cash flow. And you are getting the stock for a market capitalization of a little over $200 million.

And yes, phone book revenues are in terminal decline and that will no doubt continue. The core directory print business declined at 22% in 2012 and the company projected more of the same this year. But Yellow Media hasn’t stood still and watched their business evaporate; on-line revenues now make up about 35% of the business. They should have some competitive advantage with their on-line offerings; they have years of relationships with small and medium sized businesses and a recognized brand in Canada.

Anyways I find it hard to pass up a business trading at less than 1x free cash flow. The company is obligated to work down its debt over the next few years and they could be close to debt free 3 or 4 years out. At that time the phone book business will be generating a fraction of the cash it is now and the on-line business will be bigger. So a lot depends on whether the on-line business can keep growing and eventually develop into a sustainable company and that is something I need to delve into in more depth.

So this is a bit of a departure for me. I like positive catalysts, and in this case the main one is “revenues-decline-less than-expected”, which isn’t much of a catalyst. But 1x fcf? I mean come on… even a little bit of love from the street and this stock is at $10. So we will see.

Adding to Radian Group (RDN)

Radian’s fourth quarter results had a big negative headline number (-$1.34 eps) but the specifics of the results were actually pretty decent. In particular, the company continued to guide to an operating profit in 2013, and it disclosed a truly banner January cure rate of 109%. When the stock fell hard first thing in the morning after the release it seemed likely that the more casual stockholders were focusing (incorrectly) on the headline number and not looking (or perhaps understanding) the important numbers. I added to my position. It was a bit of the roller-coaster ride for the rest of the day, as the stock quickly took off to over $7 before falling back into the $6.50 range, but since that time my thesis has proven out and the stock has been steadily gaining. As I’ve written about before, I don’t really buy the naysaying arguments on the stock; I think that delinquencies are falling and cure rates rising and that betting in-line with the trends of that data seems to be the prudent thing to do.

Adding to Tricon Capital (TCN.to), IDT Corp (IDT) and YRC Worldwide (YRCW)

I have already written about Tricon, IDT and YRC Worldwide in some depth so I won’t go into the details too much here.

In the cases of both Tricon Capital and YRC Worldwide my additions came after recent events confirmed my opinion. I like to initiate a starter position in a company and then add to that position if the company performance confirms my expectation. In the case of YRC Worldwide it was a solid fourth quarter while with Tricon Capital it was the purchase of residential real estate in Charlotte.

As for IDT, the only particular event that drove me to increase my position was my own research. As I looked at the company in more depth I became more convinced that it was undervalued and that catalysts were on the horizon that could change that. I felt it prudent to increase my position, even though I did so well off the lows of year end.

Adding to Atna Resources (ATN.to)

Atna is another positive news buy, as I added after the company reported it had received its large mine permit for Pinson. This is a big step for Atna that should allow them to begin producing gold at much higher rates. Yet I am concerned I have made a mistake. While I have no company specific concerns, I am worried about what the price of gold will do over the near term. Its been falling precipitously of late and if the US economy really is improving you have to wonder how much further it has to go. Atna is a higher cost producer and so their margins are going to be at risk as the price falls. I have been contemplating the logic behind holding both of my two remaining gold stocks (Atna and Brigus Gold (BRD)) and while I haven’t come to a conclusion yet, I may decide to cut the lot of them in the near future.

Portfolio Composition

A bit of house keeping. I finished the Visual Basic program I had been working on. The program imports, sorts and prints my closed and open positions. I have updated my Portfolio Page to show both the closed and open positions output, as well my portfolio composition below. My previous method of posting out each week’s performance sequentially on the Portfolio Page was getting a little unruly and the Portfolio Page was getting very, very long. It has a much cleaner presentation to it now.

The program basically allows me to export the trades from the Practice Account, import them into the spreadsheet and from which it automatically sorts the open and closed positions and queries Yahoo Finance for the current prices. Its slick and I’m kinda proud of the geek-out result. From now on I won’t have to deal with the bugs in the Practice Account outputs, in particular the incorrect gain/loss calculations that it was making in some cases. The trades page, linked to below, is still directly from the Practice Account.

To see the last three weeks of trades, click here.

{kind=link}

>and queries Yahoo Finance for the current prices.

Any chance you could share that piece of code, I’d love to have it!!!!

Also, do you happen to do (paid) telephone consultations…..I’m heavily in gold/silver and getting absolutely destroyed, I’m starting to get the deer in the headlights feeling like I had in 2008 and don’t know what to do.

Thanks, Trevor

Yeah the gold stocks have been getting killed. Its tough in that sector right now but having been in and out of gold for a number of years I’ve seen this sort of despondency before and it usually marks a point near the bottom.

I have exactly the same concern regarding Atna, but a much larger position.

I bought a bunch of gold stocks today (ATN, EPZ, OGC, BRD) for a trade. I think its gone too far and while I am a bit wary of gold over the medium term it seems ripe for some sort of bounce. We’ll see if I’m being too cute.

I completely agree with your take on YRCW. I currently own about 1% of the shares outstanding of the company so I’m clearly biased. However, the company has gone through a major metamorphosis. I honestly didn’t expect great things out of Q4 (or Q1 for that matter) because it is a seasonally weaker quarter and Hurricane Sandy really put a dent in business. However, the fact that they were able to generate better operating income than Q3 and are within a stone’s throw of generating a net profit, I believe come Q3 2013 they will be able to post a $1+ EPS quarter. And I don’t think the market is even remotely prepared for this. In fact, I wouldn’t be surprised to see them post a $2 EPS quarter, benefited by continued operating ratio improvements and a rollout of their handheld technology to their drivers which should result in continued improvements in on time deliveries and overall operating efficiency. This is the most leveraged company I have ever seen in my entire life: if they are able to grow revenues 2% in 2013 they could see a $5 EPS improvement.

Ultimately, I do see the company returning to positive net profit in 2013 and I believe the company can ultimately generate $200 Million in free cash flow, which will enable them to pay down their debt and within 2 to 4 years I think the company will trade at a $1.5 Billion market cap (roughly $65 to $70 per diluted share).

Best of luck on your trade.