The Hidden Values of Ambac (AMBC)

I started a position in Ambac this week. While I still have more work to do on the company, I’ve done enough to think its worth a starter position. As usual, it will grow as the stock trends up and if events arise that validate the thesis behind my purchase. I first got the idea for the stock after having read Christian Herzeca’s blog post that points to the benefit Ambac has accrued from MBIA’s legal trailblazing.

Much like every other company with a ticker the stock ran away from me on Friday and is already a couple of bucks above where I bought it. Yet despite the move, I don’t think this is a scenario you have to rush into. The catalysts to stock appreciation are all going to take time to play out:

- A business plan that realizes the benefits of past net operating losses

- Reversals of their RMBS loss reserves

- Trial wins and/or settlements that add to shareholder value

About the only possible short-term catalyst I can imagine is if the company finds a merger partner that can take advantage of its NOLs. And given that the company is fresh out of bankruptcy, I doubt that is going to happen overnight.

I’m still trying to wrap my head around the company. The financial statements are complicated and the amount of disclosure available is sparse (with a company just recently out of bankruptcy it’s typical to have little information available). I tried, for example, to pull off an adjusted book value estimate for the company (equivalent to the one MBIA provides) but ran into a enough roadblocks along with way that I had to conclude that I failed miserably in the attempt and that the required data either just isn’t there or I still have more to learn before I find it.

Ambac runs business that is quite similar to MBIA. They have a public insurance business that, in the past, has underwritten bond issues from municipalities, counties, and long-life public projects. And they have a structured finance business that in the past offered financial guarantees on residential mortgage backed securities (RMBS), collateralized debt and loan obligations (CDOs and CLOs) and collateralized student loans.

Much like MBIA, they ran into a lot of trouble in 2008 as they began to experience significant losses on their financial guarantees. However unlike MBIA they were unable to avoid bankruptcy. They emerged from bankruptcy at the start of May.

Exposure to RMBS

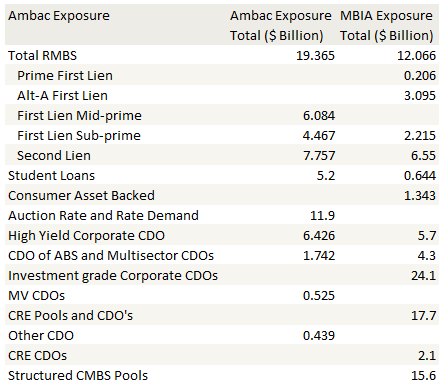

Much of the work I’ve done on Ambac has been as a comparison to MBIA. And one of the first things that made Ambac stand out to me was that unlike MBIA, they have virtually no exposure to CMBS and commercial real estate (CRE). I put together the following table of exposures of each company (note that MBIA exposure does not add up to the total gross par of MBIA Corp as I limited the table to items where there was overlap with Ambac).

The primary source of new loss reserves at MBIA has been its structured CMBS Pools and other CRE CDO’s. A big part of the settlement with Bank of America was the commutation of all of the CRE exposure between the two companies.

Ambac, on the other hand, is primarily exposed to RMBS (mid-prime, sub-prime and second lien). And while low grade RMBS securities have been crushed, most of that crushing took place over the last 5 years and is now complete. Barring another downturn in housing (something that looks much less likely at this point), there should be little more crushing on the horizon.

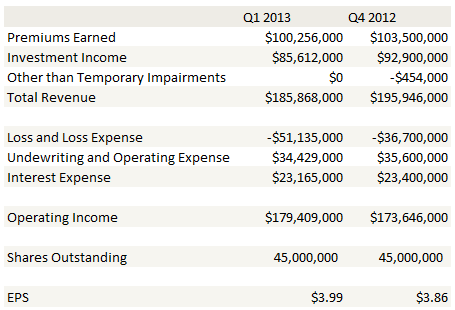

Indeed the losses on RMBS and elsewhere in Ambac’s portfolio appear to be subsiding and to some extent reversing. In the first quarter Ambac recorded only $4.1 million in new loss reserves, down from $464 million in Q1 2012. They also reversed $129 million in previously recorded losses related to RMBS. In the fourth quarter, while the company did not break out new losses from reverses, the change in the overall loss reserve was a net benefit of $36.7 million, suggesting again that in that quarter revisions outweighed new loss estimates.

A look at Pro-forma Income

The lower levels of reserving are leading to a much improved income statement. I did some work to come up with a pro-forma income statement, ignoring the effect of the mark to market on derivative instruments, one time gains on investments, gains on foreign currency, etc. The company has generated a tidy operating profit in each of the last two quarters. Note that even without the net benefits from Loss and Loss Expense the company would have been quite profitable.

Keep in mind these are run-off earnings and, absent the company writing new business, they will decline over time.

Net Operating Losses

A second catalyst for the stock is the company’s massive net operating losses. As I mentioned earlier, Ambac went through a tough time in 2007-2012 with the result being that they lost a whole lot of money. The emerged from bankruptcy with most of the tax benefit associated with those losses intact.

The following are all excerpts from the first quarter 10-Q:

As of March 31, 2013 Ambac has an ordinary U. S. federal net operating tax carryforward of approximately $7,107,171, which if not utilized, will begin expiring in 2029 and will fully expire in 2034

…Ambac has relinquished its claim to all net operating loss carry-forwards resulting from losses on credit default swap contracts arising on or before December 31, 2010 to the extent such net operating loss carry-forwards exceed $3,400,000. The exact amount of the loss carry-forward relinquishment is $1,059,988.

…Upon emergence from bankcruptcy, approximately $816,380 of the NOL will be reduced for cancellation of indebtedness income and reduction of interest expense pursuant to IRC Section 382 (l)(5).

…As a result of the development of additional losses and the related impact on the Company’s cash flows, management believes it is more likely than not that the Company will not generate sufficient taxable income to recover the deferred tax operating asset. As of March 31, 2013, the company had a valuation allowance of $3,134,054.

When put together these statements suggest to me that Ambac is carrying around $3 billion of NOL’s, and in addition that they have another $3.1 billion of NOL’s that are not being recognized simply because the company can’t envision a scenario whereby they would earn enough money to offset them before they expire.

Now NOL’s are a precarious catalyst, because if Ambac cannot find a way of becoming profitable then they are essentially worthless. And while I am not super familiar with the accounting of NOL’s during I takeover, I have heard it can be difficult to carry them over in such a case, so they may or may not represent a significant asset to an interested party. Nevertheless, they pose an interesting chip that could be played by a creative management. Ambac is after all involved in an industry that currently has a dearth of players; with a proper capital infusion they could perhaps venture back into public insurance or expand back into structured insurance now that we are seeing a resurgence of structured vehicles. And how about a plain vanilla mono-line business, where they would compete for the 20% ROE’s that MGIC and Radian have been bragging about.

Putback Recoverables

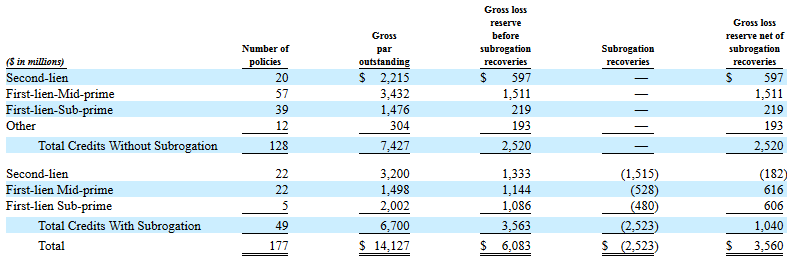

The final catalyst for Ambac is to take advantage of the inroads made by MBIA on putback litigation and maximize the recoveries of their putbacks. Of the company’s $14 billion in RMBS gross par and $6 billion in gross loss reserve, they have booked $2. billion in what is called subrogation recoveries. From the 10-K:

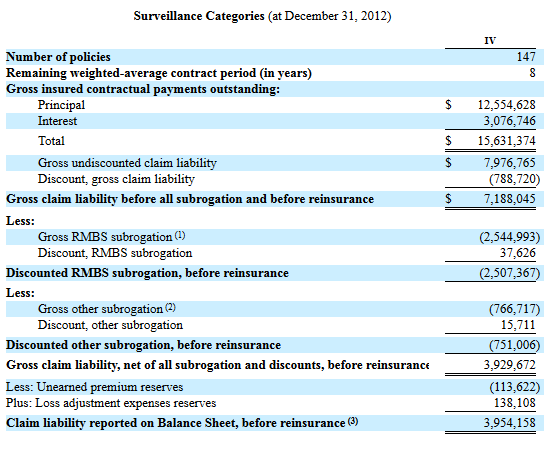

Subrogation recoveries are really just a fancy way of saying that this is money they expect to get back in one way or another for breaches of representations and warranties. The subrogation recoverable listed in the table above refers to only those loans to which Ambac contracted a third party to investigate and quantify the breaches. On the other $2.5 billion of loans, Ambac has booked a further, relatively smaller estimate of what they expect to get back. While I’ve had a bit of trouble trying to understand what that number is, I’m pretty sure the number is somewher between $500 million (provided in Note 3 of the Surveillance Categories table on Page 127 of the 10-K) and $750 million (which comes directly from the table itself). Below I’ve reproduced an abridged version of the table showing only the RMBS data, as well as the Note 3 subrogation recoverable.

Subrogation recoveries are really just a fancy way of saying that this is money they expect to get back in one way or another for breaches of representations and warranties. The subrogation recoverable listed in the table above refers to only those loans to which Ambac contracted a third party to investigate and quantify the breaches. On the other $2.5 billion of loans, Ambac has booked a further, relatively smaller estimate of what they expect to get back. While I’ve had a bit of trouble trying to understand what that number is, I’m pretty sure the number is somewher between $500 million (provided in Note 3 of the Surveillance Categories table on Page 127 of the 10-K) and $750 million (which comes directly from the table itself). Below I’ve reproduced an abridged version of the table showing only the RMBS data, as well as the Note 3 subrogation recoverable.

Note 3:

Note 3:

The point here is that Ambac is likely being conservative on its recovery assumption for the other $2.5 billion. For the RMBS that the company has investigated thoroughly they are expecting a recovery of about 70%, yet for all other RMBS they are only booking about 20% recovery. If all RMBS see equal recoveries of 70%, Ambac stands to gain another $1.25 billion in recoverables. This is a not insubstantial $28 per share of additional book value.

Now of course there are a lot of if’s in this analysis and, as we know from MBIA, these things can take a very long time to be realized. But it remains another potential catalyst that, when added to the others, makes the shares attractive to me.

Conclusion

The way that I’m looking at Ambac is that they have been dealt a few interesting cards, they are out of bankruptcy and ready to play another hand, so let’s see what kind of interesting things they can do to make the most of what they are dealt. If nine months from now they are in the same position they are now I probably am going to begin to lose interest. What I am hoping is that between now and then management comes up with some creative means for realizing the locked up value that I have described. We’ll just have to see how it plays out.

Nice post. Good to see someone looking at this other than myself. I’ve been trying to figure this out & it’s been mind numbing. I brought the 10q home with me to get through this weekend but its truly awful to read. Based on the 10k, I came to the same conclusion that there’s a lot here. Here are my thoughts:

I think it is likely that $2b in subrogation recoveries aren’t appearing on the BS, but do show up in the notes. I also agree that there’s more potential recovery on the policies they haven’t looked at.

I also wonder if the book isn’t potentially marked aggressively (as both severity and frequency have probably improved over the last 2 years), as this is the incentive through a bankruptcy proceeding.

I would be curious to hear your take, if you have one, on the terms they pay out on the segregated account. 25% cash and 75% in a surplus notes.

There also seems to be a lot of opportunity to commute these policies, ie. the student loans they commuted. Any thoughts on that?

I own it @ about $20, but I can’t even begin to figure out what it is ultimately worth, to me it seems like its probably a lot more than the $1.25b in market value. Could really be a multiple of that, with the NOL and the recoveries, and the marking/commuting of the policies.

I just started looking at it and want to first get a handle of what is in included on the balance sheet when it comes to loss reserves. The prior post thinks that $2 bn in subrogation is not appearing on the bs, but from the K, doesn’t this below state that it is?

“As of December 31, 2012, we have estimated subrogation recoveries of $2,523.2 million (net of reinsurance), which is included in our loss reserves. These recoveries are based principally on contractual claims arising from RMBS transactions that we have insured, and represent our estimate of the amounts we will ultimately recover. However, our ability to recover these amounts is subject to significant uncertainty, including risks inherent in litigation, collectability of such amounts from counterparties and/or their respective parents and affiliates, timing of receipt of any such recoveries, regulatory intervention which could impede our ability to take the actions required to realize such recoveries and uncertainty inherent in the assumptions used in estimating such recoveries. The amount of these subrogation recoveries is significant and if we were unable to recover any amounts our stockholders’ deficit as of December 31, 2012 would increase from $3,247.0 million to $5,771.6 million.”

http://www.sec.gov/Archives/edgar/data/874501/000119312513122346/d449863d10k.htm#tx449863_22

Also, Gary’s reply implies that the balance sheet is marked conservatively, but the recovery rate of the subrogation of the RMBS is about 70%. I have a hard time assuming that that is to be considered conservative.

I agree that in the BK process management should have had the incentive to be conservative, still I do not see it. Assuming $2.5 billion or 70% of all gross pre subrogation loss reserves does not seem to be conservative to me.

It does seem that there might be a benefit from the improving housing market on loss severities and loss reserves that might not have been recognized yet. And given how the housing market is doing well one would assume actual losses could be markedly less.

I think your right about this with regard to the 2b.

Definitely could be right about this. Time will tell what recoveries are I guess.

Yeah I think I was pretty clear that the $2.5 billion you are referring to is on the balance sheet. I mean snipped the table from the 10-K where it points to the $2.5 billion in recoverables that are on the balance sheet and put it right in the post and then used that number to indicate what recoverables might be for the other Par outstanding that does not have subrogation recoveries. Only thing I can think of is that you are confusing the two $2.5 billion values that are in that table.

I wound up losing it in the note, my fault for not being more careful.

I think its safe to say that no one really knows what this thing is worth. The recoveries and estimates are kind of a shot in the dark.

The 10-Q says 302M shares not 45M shares as is listed in the article. Am I missing something?

You are looking at the share count pre-emerging from bankruptcy

8 MBI insiders picked up shares last week in fair size. 53,000 shares between them

http://www.nasdaq.com/symbol/mbi/insider-trades

Thanks for the info. Its good to hear – share price isn’t acting so well last couple of days though.

If I read it correctly, they are assuming 2.5bn on the balance sheet for reps & warranties recoveries, the $500mm (or 700) number you are referring to is just a plug for recoveries they expect to get on claims already paid (from 10Q):

“The amount of recorded subrogation recoveries related to each securitization is limited to ever-to-date paid losses plus projected future

paid losses for each policy. To the extent significant losses have been paid but not yet recovered, the recorded amount of RMBS

subrogation recoveries may exceed the expected future claims for a given policy. The net cash inflow for these policies is recorded as a

“Subrogation recoverable” asset. For those transactions where the subrogation recovery is less than expected future claims, the net cash

outflow for these policies is recorded as a “Loss and loss expense reserve” liability.”

So in reference to the chart you pasted of “total credits without subgrogation”, I am pretty sure that they have made no assumption for Reps recoveries…which may or may not be too conervative, I would imagine the reason they have not made an assumption is probably just because they have not initiated a lawsuit yet.

Happy to be wrong, let me know thoughts…

The way I read it was that for the $2.52 billion without subrogation recoveries, they have made what I might call a nominal estimate of $500 million recoverable, but this amount isn’t based on the kind of exhaustive analysis that the $2.523 billion in recoveries is based on. I get that from the Surveillance Categories and the Note 3 table that I copied. In the Surveillance Categories, they subtract out the gross subrogation recoverable, which I think is the equivalent of the Subrgogation recoveries in the first table, and then on top of that they subtract “Other Subrogations” – and this amount is I think analogous to the $500mm that was in Note 3.

But its complicated and not clear so I might be wrong too. I certainly have written the word subrogation more than I would have ever expected possible.

That $500mm number you are referring to in note 3 is on the balance sheet and is referring to claims for which they have paid out but not recovered losses yet. Since the cash has gone out the door but they expect to get it back, they have to create an asset for it (since it is referring to claims already paid, it has nothing to do with reserves or “expected losses”)

what I do not understand is, of the $2.5bn for which they have not assumed any subgrogation, what is the reason, is it simply that they have not got around to filing the claim? and for the 2.5bn of claims that they have on the B/S already, is that simply the gross amount of what they asked for in the claim, or is it their best guess as to what they will actually recover (i.e. maybe they have filed lawsuits for ~$5bn and they expect 2.5bn?)

I’m not sure where you are getting the comment “it has nothing to do with reserves or “expected losses”” – I don’t believe I ever said it did. Where are you getting this from?

The upside really comes from AMBC settling above 2.5 bn. Note that if you go through all the complaints MBIA, AGO, Syncora, and Ambac filed, the ones that have settled mostly (Countrywide inparticular) come in at 120%+ amount paid. AMBC has already paid out $2.5 bn. While we know that JPM is a hard ass, the precedence in MBIA and AGO can really help AMBC’s case here against countrywide.

would be interesting to see where it shows they paid $2.5bn already

Thanks for the 120%+ amount paid info. That was something I was meaning to investigate but haven’t had the time yet.

Maybe just miscommunicating, I read your comment as if you thought that ($500mm) number referred to their expected recovery on the $2.5bn of expected losses for which no subrogation estimate has been assumed in the chart you posted “total credits without subgrogation”.

All I am saying is that I do not think they have made any subrogation assumption for the remaining $2.5bn (as the name of the chart would suggest), and instead, the $500mm number is simply referring to claims they have actually paid but expect to get back some of the money.

Have you gotten any color on what the “gross other subrogation” ($766mm) is? (beyond the footnote)

I assumed* it was related to the gross other subrogation number and the reason I thought that is that the two numbers are very close for the 10-Q (but less so for the 10-K. My thought was maybe the difference in the 10-K is just allocating between the Gross RMBS Subrogation bucket and Gross Other Subrogation bucket. If you add the two together they come pretty close to the recoveries listed in Note 3. But its a lot of guess work on my part.

You might be right that there are no recoveries against the $2.5bn. I admit I was making a number of assumptions to get there. All the better I guess if you are.

You had mentioned this in your article but is there not additional upside just from the runoff business continuing to build equity? Based on the number I have seen, $100M per quarter net income seems reasonable for at least the next several years. That could build some substantial equity on a $1.2B stock.

But remember, the reserve reversals will flow through the income statement so be sure not to double count. Fwiw, BTIG expects net income of just $53M and $11M in ’13-14, respectively. Has anyone tried to reconcile/extrapolate his estimates vs. recent results?

just wondering how an inevitable change in trends (the catalyst being?) might affect this asset’s prospects: http://www.bloomberg.com/news/2013-05-19/leverage-loved-in-equities-spurs-broadest-u-s-rally-since-1995.html

Maybe i’m wrong here as far as the nature of the sale but appears that MBI’s CEO sold a large portion of his stake last week.

http://www.secform4.com/insider-trading/1205159.htm

also wondering about possible impacts resulting from the outcome of this:

http://www.bloomberg.com/news/2013-05-24/fannie-mae-winning-at-the-alamo-prompts-lender-angst.html

http://investorshub.advfn.com/Fannie-Mae-Preferred-S-FNMAS-20248/