New Positions in Supercom and PNI Digital Media

I took starter positions in a couple stocks in the last month. The descriptions I wrote below took up a bit more space than I expected so I’ve relegated them to their own posts rather than include them in the monthly update. In both of cases the stocks are micro-caps and not without their flaws, so I expect to be following my usual wait and see approach; take a small position, watch the story play out, and add to that position if it does.

Supercom (SPCB)

The idea for Supercom came by way of this SeekingAlpha article, which does a pretty good job of describing the idea. I say pretty good because I think the article exaggerates the thesis somewhat. And given the market’s own tendency to exaggerate when it comes to SeekingAlpha thesis with small cap stocks, that might be a reason not to chase this one. I bought the stock at $4.68 and only 3 days later I’m up over 10%.

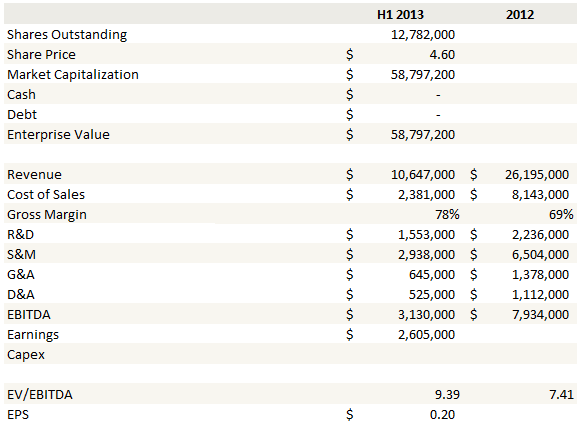

Supercom produces RFID’s for and electronic ID’s for public safety, healthcare and homecare, animal and livestock management. They also produce electronic ID’s, used by countries to manage citizen identities. The company recently acquired a close competitor, the Smart ID division of On Track Innovations. The stock shot up in the summer after news of the transaction because of the expectation of synergies which should result in improved financials. Below is a table that I stole from another SeekingAlpha report. It demonstrates the degree to which the combined company will benefit.

While the combined entity does appear to have gained operating leverage, my own work found that on current metrics it isn’t quite as cheap as the Seeking Alpha writer makes out. The company had a large gain due to the conversion of convertible to equity in 2012 and a large tax gain in the first 6 months of 2013.

While the combined entity does appear to have gained operating leverage, my own work found that on current metrics it isn’t quite as cheap as the Seeking Alpha writer makes out. The company had a large gain due to the conversion of convertible to equity in 2012 and a large tax gain in the first 6 months of 2013.

Without these one-time events, based on the 6 month results of the combined entity and given the extra shares recently offered at $4, the stock is trading at 9x the last 6m EBITDA and 7x last years EBITDA. There is very little in the way of taxes, D&A, interest costs so annualized earnings based on this year’s results come out pretty close to the EBITDA number, or about 40c per share. Below are the combined entity estimates of EBITDA and earnings that I snatched from the prospectus:

Even though these numbers don’t strike me as a screaming bargain, I still bought the stock. I think that the story here is the pipeline and the opportunity to see a sudden jump in revenues from a new contract

The CEO of Supercom was interviewed as part of the Seeaking Alpha article and he pointed out the following:

we are inheriting a huge pipeline of bids around the world and, as some of you might know, the bidding process in the EID space is very long term. It can take two to three years to win a contract. But, once you win these contracts, you have a very long term base of revenues. So we’re inheriting a pipeline with bids in over 20 countries around the world and many of them are close to maturity and we expect to see a number of these awards be given out in 2014, which has potential to increase our revenues significantly going forward.

The bids that he is discussing are for government contracts, and the size of the government contracts can range from $5mm to $150mm. So they are significant compared to current revenues ($30mm). One contract win would be a big win for the stock. And while I haven’t done a lot of work on the valuation of the competition, again deferring to the comments of the CEO, it appears to be reasonable:

Looking at our peers, our share price may be viewed by some as undervalued. Look at Zetes Industries, ZTS on the Brussels Euronet Exchange; it trades at a P/E of 25. Or consider the L -1 Identity Solutions acquisition at an EV to EBITDA multiple of 20.

Conclusion

One worry I have is that this whole thing feels very promotional. Not my post (I hope – haha), but the SeekingAlpha article, the comments by the CEO, they are throwing around a lot of big numbers and cheap valuation metrics and we will have to see what comes to fruition.

I’m keeping my position appropriately small (its around 2%), which my usual watch and see approach. As I said, if I didn’t have a position already I wouldn’t chase one here. The stock isn’t as cheap as its made out in the article and the catalysts for appreciation are going to occur throughout the year 2014, so there is probably no rush to jump in.

PNI Digital Media (PN.CA)

PNI Digital Media is a puzzle with a lot of pieces that fit together, but a few still missing. They provide a software platform for uploading pictures to retailers for printing and value-added products like cards, calendars and invitations.

There are a lot of positives here. The company boasts an extremely impressive list of customers, and indeed it was the customer list that got me interested in the stock in the first place. Retailers who deliver their digital photo products through the PNI platform include: Costco Wholesale Ltd., Costco Canada Wholesale, Costco Australia, CVS/pharmacy, Walgreen Co., Sam’s Club USA, Wal-Mart Canada, Wal-Mart US (mobile photo API only), Blacks, Rite Aid, Tesco, and Fujifilm.

The company has had trouble growing revenue in the past. This year they made some efforts to improve revenue by getting their customer base to agree to what they call the “preferred transaction model”. With the previous revenue model the company look a small slice of each photo that was uploaded, whereas with the new model they are paid on the value added products that the customer buys. So its geared towards things like custom invitations, Holiday cards, calendars, and albums.

Finally the company recently came to a two year deal with Samsung that installs their mobile device on every new Samsung device. This will make it the default for customers who take a picture on their phone or tablet and want to send it off for printing. Most of the above mentioned retailers have recently been intregrated into the PNI mobile app, which should mean a seamless transfer from phone to end party.

The idea’s missing piece is trying to quantify the upside once the full effects of revenue model changes, mobile, integration of new customers, Samsung agreement to revenues have been realized. It makes sense to me that it will be significant, but I can’t seem to come up with a thread that will allow me to nail down how much. The idea depends on the success of the recent moves; last years growth didn’t blow me away – 5% and the company currently has negative EBITDA and trades at 2x revenue, so its not cheap by my usual standards.

I took a small position at $1.11. It’s a $38 million market capitalization company and I find it compelling that a company this size can have a customer base this hefty. I also like the momentum the stock has, and the integration of customers to mobile and into Samsung devices makes strategic sense. So I’ll wait and see what the fourth quarter results bring. They will be seasonally strong because of Christmas and New Years, so the real proof will be the year of year comparables. Until then…

Blast from the Past:

Good luck with PN. I won’t be following you in. I bought this stock ca 2008 when it was called PhotoChannel. The company always seemed to have promise. They just needed to get the CVS account, or the Costco account, or the Wal-Mart account. Then the cash would come flowing in. Well they eventually got all of those accounts and several more, but there was no discernible improvement in the economics of the business. I finally came to the realization that their business model was flawed. They have no pricing power with those retail heavyweights and consequently, they can’t make any money. I took a 50 percent haircut and moved on, never to look back — until today.

I see that that the PN share price has gone up by a factor of five in the last few months. Wow! But I can’t find any news that would account for such a big move. Do you have a theory? Anyway, I noticed that the company recently (20 Dec) took advantage of this inexplicable (to me at least) move and sold another 7 million shares to the public at $1.05 per share. Consider yourself diluted.

I think the price has gone up because of what I explained in the post, which was also addressing your concern about the model. But we will see, you could easily be right. I’m not really being diluted much given that I bought the stock after the offering closed and a few cents above it so I’m not sure what you mean there.

I just found the Supercom article yesterday. I also found it extremely promotional, but the business does look high quality. I think I’ll wait a few quarters and see what happens. I have no idea how they’ll do vs. competitors.

I think the RFID technology is still relatively new in terms of public opinion. Once it becomes more mainstream and well accepted and new uses are found for the technology stocks like Supercom will take off. I think it’s good for a long term investment.

I agree that the supercom article seemed very promotional, but doing my own valuation made it seem pretty attractive.

The big question/assumption I built into my model is that Supercom management can turn around the OTI division’s margins like it did when it took over Supercom. If it can get operating margins up to 25%, even if it takes a few years, I get a value/share of $5.85 currently. I think that’s the very large question right now, but given the past 3 year turnaround I think it’s fair to give management the benefit of the doubt when it comes to increasing margins for the OTI division.

Now, the kicker is, that value assumes 0 growth. We’ve seen that they have the ability to cut the fat off of operating expenses, but as of yet, we haven’t seen management grow revenues yet. While I’m skeptical about management’s lofty expectations, a 20% CAGR over the next 5 years, with revenues at $63m at the end of 2018, gives a value of $11.07/share.

Overall, it does not seem like a highly risky investment, with protected downside risk, and good potential upside.

Keep in mind, this is completely ignoring the RFID sector and only focusing on EID, since we have no idea where RFID is really going and how successful the company will be with growth in that area.

I’m about to enter into a position myself with Supercom and write a post about it soon, with my valuation file included.

LOL – check out PNI corporate twitter account pumping an article about PN long pitch. Yikes! Here is the article they linked to http://www.canadianbusiness.com/investing/pni-digital-media-pn/

why yikes?