Third Quarter Earnings Updates: INVE and SIEN

Identiv

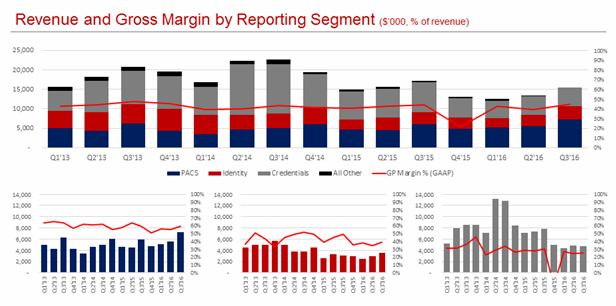

I was pleased with Identiv’s quarter. Revenue was down year over year but that is mostly due to discontinued transponder sales to Disney. Excluding this customer revenues were up 13% year over year. The company appears to be on track.

Sequentially revenue was up 31% for the Physical Access Control Systems (PACS) segment, 21% for Identity (smart card readers) and was down a little in RFID. The third quarter is seasonally strong for PACS because of government customers that have a September year end. But that alone doesn’t explain all of the strength in the results.

The story here remains that a turnaround is occurring on the expense line. Operating costs are down to a $6 million quarterly run rate. Last year they were double that.

The stabilization of the top line and improved expense management has led to positive EBITDA for the first time in a while. They have $1.7 million of adjusted EBITDA (no stock option expense) in the quarter.

Guidance was kept the same at $56-$60 million, which puts the fourth quarter revenue in the $14-$18 million range.

I think there is a good chance they can hit that range. The fourth quarter is seasonally slower than the third quarter

I tweeted a couple of times this morning that I don’t think the stock makes sense at a $20 million market cap. Its moved up since then but even at $2.50 the market capitalization is still less than $30 milion. The company has a $55 million trailing twelve month revenue run rate, they are showing growth, they are EBITDA positive now and its not an insignificant amount of EBITDA. That feels like it should warrant at least 1x sales. We’ll see if it gets there.

Sientra

I wasn’t expecting too much from Sientra in the third quarter. So I was pleasantly surprised to see a couple of positive data points: sales growth of their bioCorneum product and a tuck-in acquisition in the area of tissue expanders.

Sientra continues to progress with their new facility for the breast implant product. Their manufacturing partner, Vesta, has completed the build out of the facility and is producing test product. Sientra will submit a PMA supplement (pre-market approval for a manufacturing site change) in the first quarter and expects to be shipping product by the fourth quarter of 2017, if not earlier.

They also announced on the conference call that they received notice (just that day) that Silimed, who was their prior manufacturer and from whom all of the manufacturing issues arose, had sued the company for contract breach. I have a hard time believing there is much to worry about here since Silimed is under suspension, had their factory burn down under a still undetermined cause and obviously cannot supply product.

All of this was anticipated good news. What makes Sientra more interesting to me are the moves around supporting products.

BioCorneum is a silicon based gel that is used to prevent scarring and also to hide the appearance of scars. Sales of bioCorneum continue to improve. Revenue was $1.32 million in the third quarter. That is 20% of total revenue and up 18% sequentially.

Through the acquisition of bioCorneum Sientra has proven that they can take an under-marketed product in an adjacent vertical and apply their salesforce to increase sales. They made a second foray into this “adjacency model” in the third quarter with the acquisition of Specialty Surgical Products (SSP). SSP has a portfolio of premium tissue expanders, which Sientra said on the call is a $235 million market. They didn’t disclose sales from SSP but I suspect they are small. They did say they made the acquisition for a price in the range of 1.5x to 2x revenue. They also retain “a handful” of sales staff from SSP that will help build-out their own salesforce further. SSP products are manufactured by Vesta so there is overlap there.

Similar to bioCorneum, management said that the SSE portfolio is an “underdeveloped, under-promoted portfolio can expand with their sales staff”. Additionally, because tissue expanders are typically used in a hospital sending, the SSP sales staff is geared towards the “hospital-based reimbursement market” for reconstruction. Sientra has not sold their implants through this vertical, so there are market share gains to be made by leveraging that team.

I added a little to my Sientra position on the news.