Third Quarter Updates: Versapay

It’s getting a bit late in the game to be writing up third quarter results so this will likely be the last one I do. But I did want to say a few words about Versapay, because they announced additional divestiture news at quarter end and have an interesting white-label deal for ARC in the works that could be meaningful to the share price.

Versapay announced their third quarter results on November 29th. At the same time they announced that they had sold their Merchant Services business for $10 million up front and another $1.5 million contingent on performance.

$10 million represents about 5.5x EBITDA for the business. While Merchant Services grew pretty strongly in the third quarter (15% year over year) historically the business grows at only around 5%. With the sale Versapay is basically pulling forward their cash flow for the next 4-5 years. This isn’t a bad idea since they need that cash flow now to fund their burgeoning online business.

What the sale leaves is Versapay Solutions, which consists of their cloud based accounts receivable platform ARC. Versapay accelerated customer acquisition onto the ARC platform in the second quarter, as customer count increased from 43 to 70. In the third quarter the increase moderated to 76 customers, which was a disappointment.

The company gave the usual explanation of temporary delays, but unlike so often when the excuse is offered, in this case it may actually be true. Since the end of the third quarter through mid-November the client count increased another 10 to 86, and active customers increased to 29,000. So it appears that growth is re-accelerating.

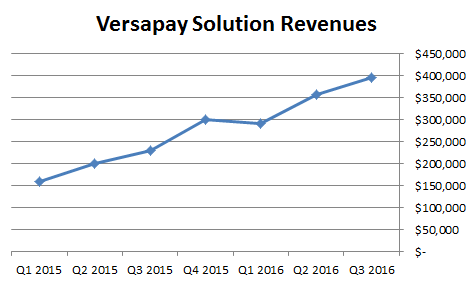

Revenue at Solutions grew to $400,000. All revenue at Solutions is recurring so the business is up to $1.6 million in annually recurring revenue.

What the sale of Merchant Services makes clear is the valuation the market is assigning to ARC. At $1.20, Versapay has a market capitalization of around $36 million. With the cash from the sale, total cash will be around $13 million. So after generously deducting the existing cash, the enterprise value of the company and valuation of ARC is around $23 million. For that price you get $1.6 million of recurring revenue growing at a 75% year-over-year rate. The conclusion I would draw is that the stock price is probably fully reflecting the current trajectory.

What could buoy the valuation is the channel partners that Versapay is cultivating. On the conference call they went into some detail about the type of channel partners they are trying to secure:

- Referral partners such as ERP vendors. The relationship with NewsCycle is an example of this.

- Business process outsourcing companies looking to embed ARC into to their product offerings. Subsequent to the end of the quarter Versapay signed one of these deals with Ricoh

- Financial institutions looking to white label the product

It’s the third group that has the biggest near term opportunity. For the last number of months Versapay has been working with a Tier 1 Canadian bank (who they haven’t named yet) on a white-label launch of ARC for the bank’s customers. On the conference call Versapay said they had now developed a “single sign-in integration with the banks online site” and that they expected to launch “a bank branded version of ARC at the beginning of December”. The banks sales reps were already out in the field selling to customers. The banks goal is to secure 10 customers as a pilot program.

If this takes off the opportunity is very large. The bank has said to Versapay that they estimate they have 100,000 business customers are a good fit for ARC. Compared to the current customer count, which is less than 100, securing a fraction of the addressable market could launch Versapay to another level. I haven’t seen anything about the economics of their agreement to white-label ARC to the bank.

I’m holding my stock, and I have added a little over the last few months. When they announce the bank relationship in more detail we probably will see a pop. Its not a cheap stock but if the customer count can move exponentially from the banking white-label (assuming the company is getting reasonable terms) I don’t think the market will care.