Vicor Fourth Quarter Results: Modeling the Ramp

I’ve owned Vicor for over a year. During that time I’ve been twiddling my thumbs waiting for the promised revenue ramp. It looks like it’s almost upon us.

The company had a bad fourth quarter: revenues down sequentially from $53 million to $48 million, gross margins down sequentially 17%, negative EBITDA. But as the stock price attests, none of this matters because guidance and color around the VR13 ramp was excellent.

I first wrote about Vicor back in March of 2016. The thesis remains the same:

The story going forward is simple. The company says that with recent design wins and product launches, in particular wins for new data centers that will utilize the VR13 standard (more on that in a second), as well as high performance computing, automotive and defense, they can grow revenue 3-5x in the next couple of years.

Here’s what’s happened between now and then:

- 3 quarters of delays in the Skylake Intel chip necessary for the VR13 standard to take off and with that for Vicor to capitalize on its design wins (I’d recommend going back to read my previous post to get the details on the VR13 chip and Vicor’s integration with it), and

- the Skylake chip is finally available (at least in pre-production) and fourth quarter suggests a turn is upon us as Vicor has started to ship power converters for VR13 design wins.

The company said on the fourth quarter call that they had “began to ship the VR13 version of [their] 48V point-of-load solution” and that shipments of the VR13 solutions would “ramp more steeply” in the second quarter. Shipments for the 48V point of load solution increased 15% sequentially in the fourth quarter and the 1 year backlog would had risen 14.8% sequentially. They expected at least 10% sequential revenue improvement in the first quarter.

With the story on the verge of happening, the questions become A. what’s the end game and B. is there enough upside in the stock left. Keep in mind that even though we are only starting to see the story blossom, the stock is 50+% higher than when I first bought it.

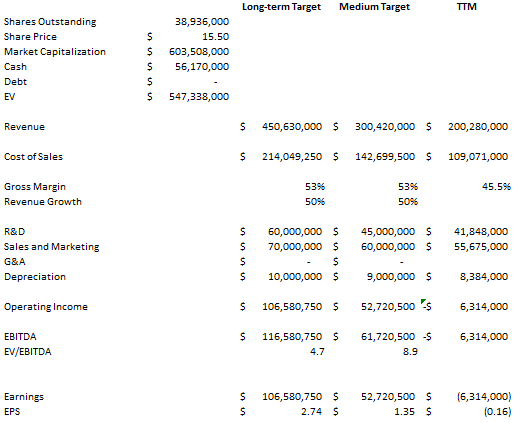

I’m not much into detailed modelling. I do some models, but they are pretty half-ass compared to what you will see from professional research. I don’t have a lot of time, and I find that I am better hedging my uncertainty with position sizes and stops then pretending that I can put together an accurate model that I can rely on.

I make a model to get one or two basic answers. At what growth rate does this company get profitable or at what growth rate does the current stock price start to look cheap?

It was the second question that I needed to answer with Vicor.

I would call Vicor a modeling play. It seems reasonably clear that revenue is going to ramp. Its just a question of how quickly and by how much. The end game is that they reach their objective of 3x revenue in the next 3 years.

Here’s the model. It’s the same model I put out a year ago, tweaked for current run rate expenses and guidance. I’m not trying to model 2017. I’m looking ahead at what the company is saying they can do with revenues as the VR13 data center opportunity ramps to its full capacity.

I’m accepting management’s comments that operating expenses are dominated by headcount, that they don’t expect this to scale with the top line increases, and that most of top line growth will drop to the bottom line. I’m also assuming that management’s assertion that gross margins can transition to the low 50%’s by the end of 2017 is correct. And my long-term target is a little over 2x revenue, not 3x revenue.

The stock price doesn’t look too bad after considering that there is this kind of upside. I almost never buy options, but I decided to buy a few October calls on Vicor. It seems like a reasonable situation for it. The ramp is going to happen in the next 6 months. The potential numbers that are materializing should be pretty clear by the fall. If this is going to play out like Vicor says it will, its going to be clear shortly. I hope they’re right.

I would just add that their main competitor in power is MXIM. MXIM is much larger and has great economies of scale with operating margins of 20%. MXIM also trades at 5x revenues.

Lots can go wrong here… BUT, If somehow VICR can scale 3x their current revenue run rate in 5 years (as the CEO promised), and if they can attain 20% OP margins like MXIM… then VICR could trade into the $70’s ($200mln rev x 3 = $600mln | $600mln x 5x multiple = $3B) | $3B / 39mln = $77

Again lots can go wrong… but if they get 48v right and competitors fail to scale competing solutions in time then we could see the stock substantially higher.

Do you know if VICR has any sort of relationship with NVDA or AMD? Just curious how tightly their fortunes will be tied with Intel in the future. Thanks!

No I don’t think so, but I don’t think they really have any any special relationship with Intel either (I might be wrong?) I think its just that Intel has a new processor generation that has a new voltage regulation standard (vr13) for which Vicor is one of the only vendors that has products that can meet it. But Vicor has been providing 48V regulators for graphics chips and DSPs for quite a while so I imagine there are applications where they are used with NVDA.

Thanks as always!