Silicom Design Wins

I took a starter position in Silicom a couple months ago. I did so because I thought their products were aligned with the software/hardware decoupling that is occurring. But I kept my position small until I saw more results.

Those results came a couple of weeks ago when the company announced a huge design win for a 100G switch fabric network interface card (NIC):

Silicom has received initial purchase orders (POs) in the aggregate amount of $17 million to cover a small-volume Alpha phase, an intensive Beta program and the product’s first commercial deployment. Having completed deliveries for the Alpha phase, Silicom is now in the process of delivering the Beta-program products while completing two additional activities: 1) finalizing the product configuration and validating the solution’s performance within the servers in which the Silicom products will be deployed, in cooperation with a Tier-1 server manufacturer; and 2) ramping up product manufacturing to a full mass-production level. Based on the customer’s guidance, Silicom forecasts that revenues related to the design win will build to more than $30 million per year.

I added to my position after the news release.

I was surprised that the stock didn’t move more on the news. I bought into the stock early in the day on the 21st at around $46-$47 but saw it tail back down to $45 as the day went on. It seems to be just a slow response; on Friday the stock had butted up against the $50 mark (editors note: maybe not! It’s Wednesday now and $50 is no more!).

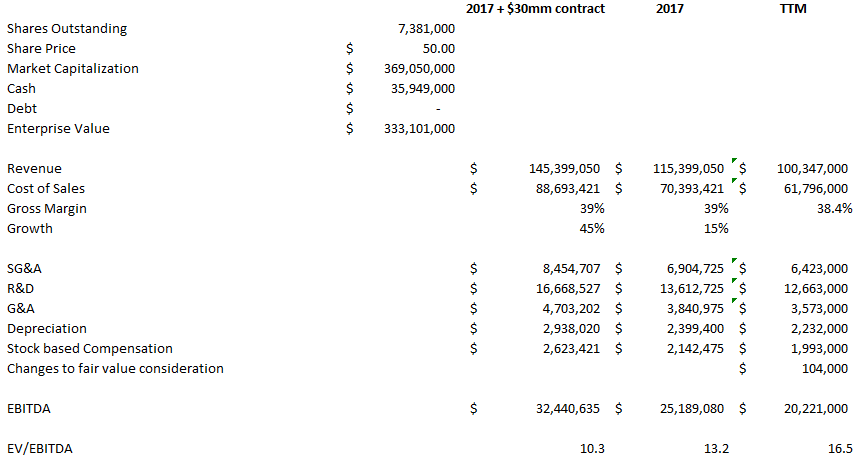

If Silicom achieves the $30 million run rate they expect, I think this contract has a pretty big impact on the valuation, enough that it maybe isn’t even all priced in, even after the $10 move.

Below I’ve added the $30 million onto a 15% growth estimate (my own estimate, Silicom has said double digit growth for 2017) and assumed that expenses (R&D, G&A) grow by half as much as revenue (the company has said that their business model is levered to growth and that the “majority” of new gross margins will fall to the bottom line, so I think this is reasonable).

I might be too optimistic about the growth rate, maybe some of that $30 million should be part of the 15%. Everyone can judge that for themselves. I’ve chosen the assumption because I like the prospects.

If I’m not, at $50 the company is trading at 10x forward EBITDA. Given 30%+ growth in 2017, it’s not an aggressive multiple for that kind of growth.

Let’s look at the products

I am hopeful that this high growth rate is sustainable. Silicom has products aligned to a number of growing segments. To understand my enthusiasm, let’s take a closer look at the product line.

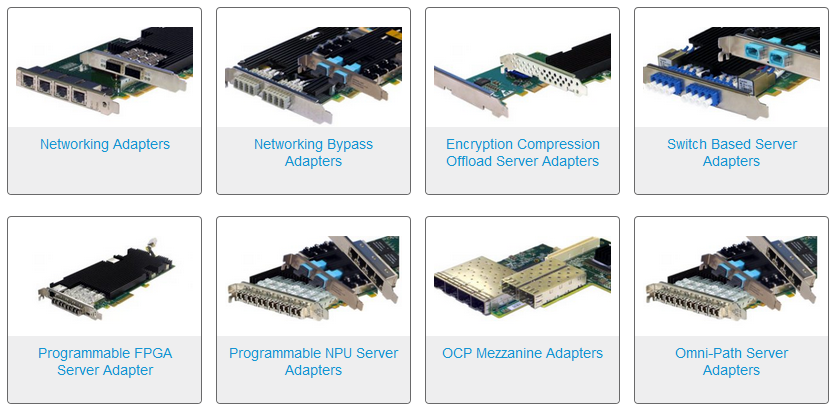

I’m still a little foggy on terminology here so I apologize if I am classifying something wrong. Most of what Silicom sells falls under the broad category called network interface cards (NICs). Under that category are server adaptor cards, which is where the majority of their NICs, switches, and FPGA cards.

So what do these cards do? They provide network connectivity and offload tasks from the CPU (buffer storage, processing packets, that sort of thing) so that the appliance they are working with can run more efficiently and focus on the dedicated tasks they are intended to do.

The cards come in a variety of flavors. There are different network speeds (1G to 100G) and different tasks they are designed to offload. These are things like data encryption, acceleration (where a chipset on the card performs some CPU tasks at times of peak usage) , data compression, time stamping, and bypass, which recognizes failure of an appliance and reroutes data when it occurs. There are also FPGA cards, which are programmable, and can made to handle a custom task.

You can see the full list of flavours here. Below I’ve taken a screen shot of the highest level breakdown of the product line, just to get a feel for what the options are and what the cards look like:

There are also higher end programmable cards using FPGA chips (field programmable gate arrays). The FPGA cards are an “efficient way for the advanced user to achieve even lower latency and to implement any filters or acceleration that are necessary for a specific application.” These cards are used in “networking, financial and big data solutions” applications. The FPGA based solutions are a product line that was came with the acquisition of Fiberblaze in December 2014.

Recently Silicom has had design wins for time stamping with a Tier 1 monitoring company (which I read somewhere was likely Gigamon), for encryption cards with a former customer that they had lost 3 years ago, the aforementioned very large win for a 100Gb switch fabric NIC, and most recently for by-pass cards to be used with a cyber security appliance.

Silicom also has a number of stand-alone products. There are switching solutions, network appliances and a product that converts off the shelf servers into appliances (SETAC).

Silicom describes their growth opportunities as being in cloud and in cyber-security. The cyber-security opportunity is pretty straightforward; their cards piggyback off of cyber-security appliances providing a network interface and offloading CPU tasks. The cloud is a catch-all for many different opportunities, including integration of their cards into monitoring, packet processing, and switching – pretty much anywhere where workloads can be offloaded from a CPU, thus creating efficiency.

SD-WAN Market

Also part of cloud is Silicom’s entry into the SD-WAN market. I’m going to talk about this one in more detail because I think its potentially a big opportunity, and has the visibility to get the company noticed by analysts. Their product is an off-the-shelf virtual CPE solution.

SD-WAN is one of the first applications to embrace network function virtualization, or NFV, something I ramble on about when talking about Radcom or Radisys. SD-WAN entails the decoupling of software from hardware for routing traffic at edges of the network. As such, traditional proprietary appliances are replaced with “software application running on inexpensive appliances to implement a flexible traffic routing solution between branch offices and the Cloud” (from this article).

SD-WAN is one of the first applications to embrace network function virtualization, or NFV, something I ramble on about when talking about Radcom or Radisys. SD-WAN entails the decoupling of software from hardware for routing traffic at edges of the network. As such, traditional proprietary appliances are replaced with “software application running on inexpensive appliances to implement a flexible traffic routing solution between branch offices and the Cloud” (from this article).

Demand for SD-WAN from service providers is surging. Silicom already has two design wins for SD-WAN appliances. The first is with Versa Networks, where Silicom is one of three companies (along with Advantech and Lanner) providing hardware. They announced the win in September. A second win was for an SD-WAN customized vCPE appliance, which is expected to scale to $5 million annually, and was announced in November. In this case the customer wasn’t announced, but my guess is its Velocloud, which seems like a likely bet to be an existing encryption card customer.

This SeekingAlpha article suggests that SD-WAN deals could be in the $10 million range, which is a lot bigger than the typical win Silicom has.

As part of the second win, Silicom said this in the press release:

“In fact, the customer’s forecast is another clear demonstration of the momentum of the SD-WAN market, as both enterprises and service providers begin adopting the new technology to enable their transition to the Cloud, NFV and the virtualized environment. We believe that our favorable positioning in this market, due both to our basis in the WAN Optimization market and the unique new technologies that we have developed, will enable us to benefit strongly from the momentum of this ‘hot’ new market space, making SD-WAN a significant new revenue driver for Silicom.”

Silicom also announced that the same customer that they had a by-pass card design win from was “considering the potential use of Silicom’s vCPE appliances as part of its Cloud offering”.

So I like the idea and hope to see more wins

Silicom’s gross margins are generally around 40%, which implies that the “moat” for their products is not very high for a technology company. While this may be a bit concerning, what I find interesting is that they seem to be the largest non-integrated competitor in the business. As this SeekingAlpha article points out, Silicom has nearly 200 different SKU’s whereas their nearest competitor (interface masters) has 35. The large integrated players (Intel for example), are way bigger of course, but they also don’t offer the range of solutions that Silicom has (being constrained to their own chipsets).

I really like this idea. I think Silicom has the right product set at the right time, ready to take advantage of the shift towards using commercial off the shelf hardware to accomplish more tasks. I think the recent $30 million design win is not fully being priced into the stock at current levels, and yet it may only be a harbinger of what is to come. I bought the stock in the mid-$30’s and added in the mid $40’s. I would probably add one more time on another big win.