Week 304: More on Edge

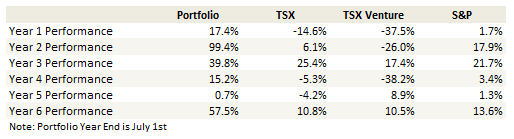

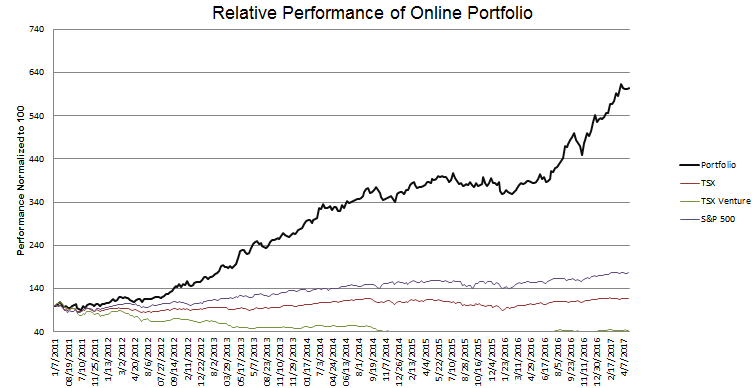

Portfolio Performance

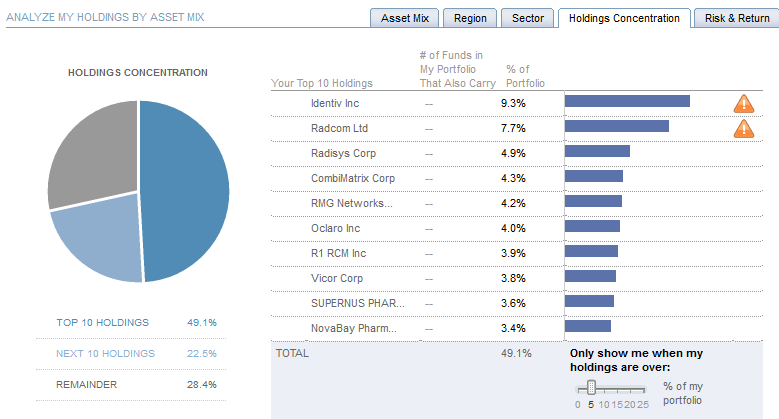

Top 10 Holdings

Thoughts and Review

In my June update I took space to describe some of the attributes of my edge. At that time I didn’t define it specifically, and so I wanted to extend that discussion here. To repeat the definition that I put forth back then:

An edge is essentially the advantage that allows you to beat the market more than it beats you. For many of these traders understanding their edge; a system, a pattern, a money management technique; has been a major step toward consistent success.

I think I have put up enough years of out-performance to tentatively conclude I have some sort of edge. Its still possible that I don’t; maybe I will blow up yet and these past years will prove to be a statistical aberration. But as times goes on those odds become less likely.

So what is it?

First, I do quite a bit of research. Now maybe I’m not the most exhaustive researcher; I know some folks that will, at minimum, read through the last 5 years of 10-K’s before pulling the trigger, but nevertheless I am on the heavy side of the research spectrum. I think its fair to say that I make decisions on a more informed basis than the average investor.

Second, I’ve come up with a methodology that works, both absolutely and for my personality. I take small positions that let me be wrong without losing a lot of money. I rarely add to those positions if they fall and sometimes cut them if they fall too much even if I have no news to suggest anything has changed. And I add to the positions as they rise and price movement reinforces the thesis.

This works for me because in the real world I’m not very good at making decisions. Just to give a couple examples from every day life, I don’t like having to choose the TV show we watch at night, what food we will have for dinner, or where we are going to go on vacation. I would rather have someone else make the decision and just go with the flow. I am fortunate to have an understanding wife.

I invest in a way that is in tune with this nature. I rarely commit to an idea unless I am deep into it. Even with my biggest positions; Identiv or Combimatrix or Radcom, I don’t feel sold on the ideas. I’m more of a renter. I am not sure if they will pan out and I am ready to run if something goes awry. It’s easier for me to pick a stock then what’s for dinner because I know it’s not for good.

The final element of my edge is the type of stocks I look for. I try to find companies that, while they may only have a small probability of going up, have the chance to go up by multiples if things play out in a certain way.

To put it another way, if I am right 30% of the time and on average my gains are 20% and my losers are 20%, I am going to lose money. But if my gains can be 100% and my losers 20% then I am going to do quite well even if I’m wrong most of the time. So I am wrong a lot, I change my mind a lot, but when I’m right its often for a double, a triple or even more.

What I did last month – Aehr Test Systems

Its actually been 5 weeks because we were on vacation for the last week and so I didn’t get this update out on time. Even with the extra week, I didn’t do too much. In fact I only made three trades. One, Catalyst Biosciences, was a fluke that I discussed in my last update. The stock is back down to where it was and I didn’t actually buy it anywhere but the practice account so who really cares.

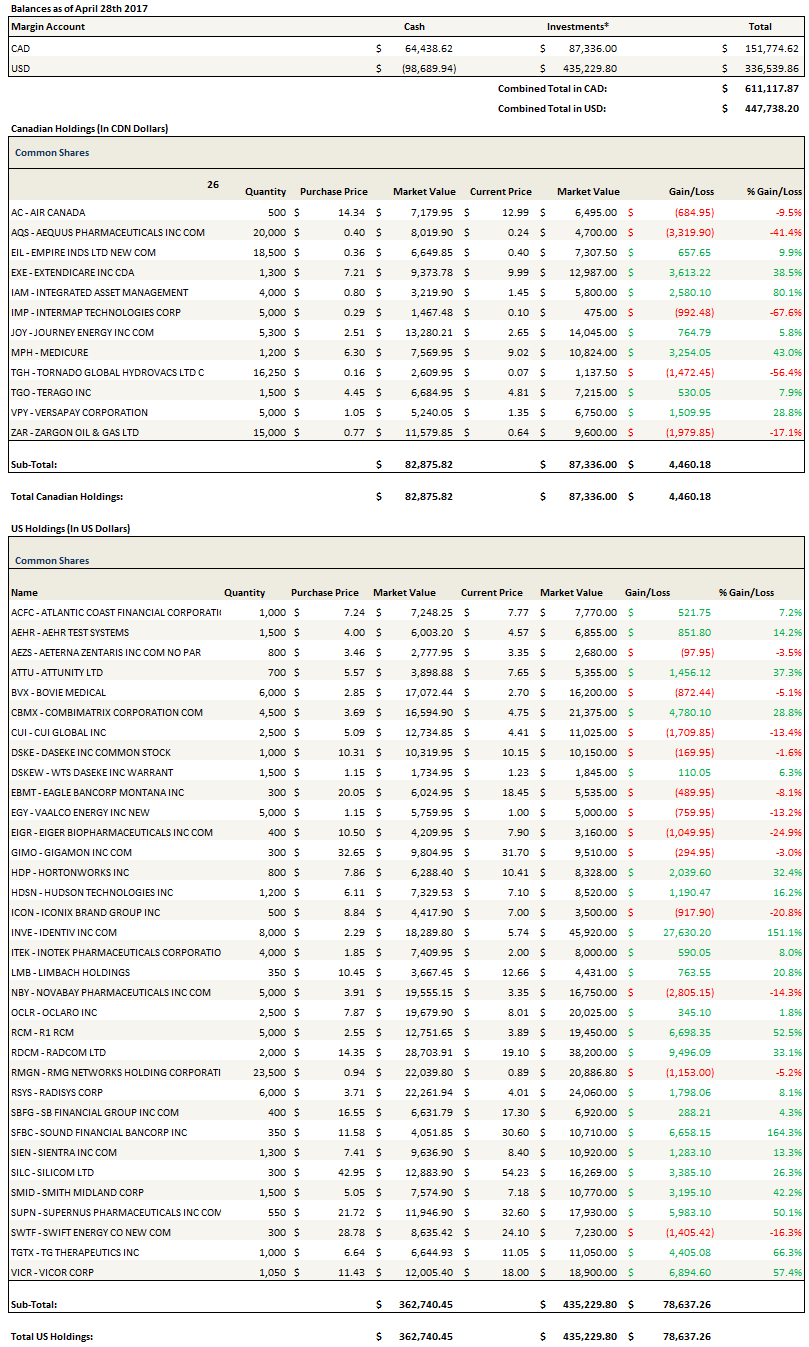

The other two were new positions. The one I’m going to mention in this update is Aehr Test Systems. They are a fairly tiny company ($90 million market capitalization) that makes testing equipment. They have a unique design (I don’t believe there is a lot of direct competition) that can test at the wafer level rather than the module level, which eliminates much of the potential for mechanical failure and improves quality controls. They started selling a multi-wafer testing machine called the Fox-XP system back in July and they have started to see orders come in. Their test equipment is sold to some large companies, like Apple and Texas Instruments (Apple and TI accounted for 47% and 32% of revenue in 2016) and they have made references to being in talks to sell product to a Korean firm that seems likely to be Samsung.

The stock doesn’t appear cheap at a glance. Revenues in the last 9 months were only about $12 million so on a trailing sales basis the stock looks wildly overpriced.

What makes it interesting is that we are only starting to see orders for the Fox-XP system. So far these orders have been for prototypes to verify the concept. The units sell for $4 to $5 million, so even a trickle of prototypes are incrementally material to the company. But the orders could scale substantially if the proof of concept testing goes well. The company doesn’t give a lot of guidance, and there isn’t much of an analyst following to prod information out of them, but on the third quarter conference call management said that if successful with their lead customer (probably TI?) they could ship 10 systems a program and that they are currently working on 2 programs. So the lead customer alone could amount to a $40 million to $60 million opportunity per program.

If the Fox-XP takes off, the stock is going to move significantly. Will it? I don’t know. It has a chance though, and that is worth a small position.

The dangers of short-term funding

In October of last year I wrote that I was short Canadian alternative lenders and mortgage insurers in the wake of the Federal government mortgage rule changes. For 5 months these positions did poorly. I began to think my puts would expire worthless and my shorts would be tax loss candidates. But last week the bet was vindicated as I took profits after the alleged fraud at Home Capital.

My thesis was not premised on the discovery of fraud. I thought there was a reasonable chance something would be uncovered as the market unwound but that wasn’t my primary reason for going short. Instead I thought the measures the government put in place in October would finally cool down the housing market and that, given that many of the measures were targeted at alternative lenders and insurers, these companies would suffer the most.

That hasn’t happened, so in that way I was lucky. But what I did get right was how things would unravel once the ball got rolling.

It cannot be overstated how precarious a company is if they lend long, borrow short and have a funding source that is easily called away. If any uncertainty develops about their lending book, the run on funding can be swift and fierce.

The collapse of Home Capital was precipitated by their dependence on high interest deposits to fund part of their loan book. Those deposits were available on demand, so at the first allegation of wrongdoing, many were pulled. Why not? Who wants to take a chance with their money for an extra percent. Adding to this outflow, there is and will continue to be a slow motion run on their GIC funding, many of which will mature over the next year and almost assuredly not be renewed.

This capriciousness is why I don’t have the stomach to hold non-bank financials through any bouts of turmoil (think back to New Residential or Northstar). You just never know when the funding side is going to tighten, and when it does an extremely profitable business model can be flipped to insolvency in a heartbeat. Again, and I know I’m repeating myself, but I don’t think you can over-state how precarious it is to lend-long, borrow short and have funding callable on demand. Everything is great until it isn’t, and then it’s all over.

As for the Canadian housing market, it continues to tick on. It will be interesting to see how the events of the last week interact with the price rise of homes in Southern Ontario and coastal BC. We are all familiar with how the US played out. There the topping out of prices was the catalyst that collapsed the loans and tightened of credit. I wonder if it has to play out that way, or whether causality could be reversed in Canada, as lenders for marginal buyers lose their funding sources in the wake of Home Capital?

We’ll see. We sold our rental property a few weeks ago so I don’t even have that chip in the game anymore. However that wasn’t driven by macro worry; instead we realized that renting is very time consuming and not very profitable (unless you live in the GTA or the coast and your house can appreciate in value by 30% in a year). Our last tenant also turned out to be a convicted criminal which didn’t help my stress level last year.

It will be another interesting week.

Portfolio Composition

Click here for the last five weeks of trades. I had to make two adjustments to the portfolio that show up as trades because of name changes that weren’t automatically updated in the practice portfolio. Accretive Health recently changed their named to R1 RCM and a while ago Limbach changed their symbol to LMB. The Limbach situation was brought to me by a reader. Its been wrong in my update for a while (displaying the old symbol and last traded price of it). This has been corrected now.

{kind=link}

Trackbacks & Pingbacks