Adding Gold Names

I decided to add more gold names yesterday as it looks to me like gold is breaking out. I finally got a move out of some of my existing positions. Americas Silver has jumped from $3.80 to $5.80, Gran Colombia Gold has moved from $1.40 to $1.60 and Klondex Gold has broken out of its $4 choke hold and is trading at $4.35.

First, I decided to add to both my existing positions in Gran Colombia and Klondex. Gran Colombia had very good news on Monday, announcing that their mine strike had ended. The stock, at $1.60, has hardly participated in the gold move, and is one of the cheapest gold stocks out there and less than 4x free cash flow. The hair remains but the settled mining dispute removes some of it, and I have to think it goes higher.

Klondex is my largest gold position and I added to it yesterday. My add here was simply that it appears to have broken out from the $4 level (Canadian). I’ve written about Klondex in the past. Its been under pressure for months from an unusual GDXJ rebalancing that caused a lot of forced selling from the fund and follow-ons. I note that there was a 25,000 share purchase by one of their directors on Thursday.

I added two new positions. First, I added Wesdome. Wesdome operates two mines at its Wawa complex in Canada and also has two advanced stage projects in Canada. They have a $320 million market capitalization and $22 million of cash and no debt. Guidance for the year is 55,000 oz. I ran a quick comparison of gold companies looking at their enterprise value per ounce produced. This is super simplistic of course, it doesn’t account for costs, reserves or development projects that are generally big determiners of value. Nevertheless, when I look at Wesdome it compares favorably (at $5,500/oz) to other miners. There are cheaper one’s out there (for example Gran Colombia and Jaguar Mining, which I will talk about in a minute), but these generally have a lot of hair. I don’t see much hair on Wesdome.

Jaguar, which I also added, comes out even cheaper, with an enterprise value of less than $1,000 per ounce. But it has lots of hair. I actually owned Jaguar years ago. It has a new management team, a lot more shares, but essentially the same mining complexes.

Jaguar has a market capitalization of $90 million, $20 million of debt and $20 million of cash.

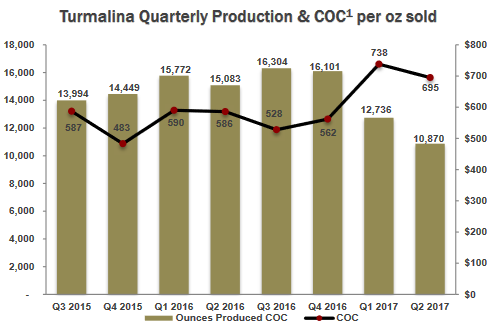

Apart from being really beat down, and very cheap (at least on a superficial basis), Jaguar actually seems like they had gotten their shit together up until the last quarter. They had consistent production from both their Turmalina, Pilar, and Roca Grande mines. But production slumped at Turmalina in the first quarter, causing the shares to slide.

The share drop was potentially accelerated by Resolute Funds, which sold 30 million shares over the quarter. I found this article, which speculates on the impact of the Resolute Funds liquidation.

My bet with Jaguar is that in a rising gold price environment, many past transgressions will be forgotten. It is also that maybe the second quarter does not portend the future. Jaguar kept guidance in the second quarter, and they had been producing consistently at Turmalina for the past 6 quarters.