Smith Micro: Stealing a Good Stock Pick

So I can’t take credit for this idea. I also don’t have much to say that hasn’t been said already. But I added the stock to my portfolio a couple weeks ago so I need to talk about why.

Smith-Micro is a Mark Gomes stock pick. In fact if you go to his blog you will find so many posts on Smith-Micro that reading them all would keep you busy for a few days.

I’m not going to repeat all the information he provides. I’m just going to stick to the story as I see it, the reasons that I took a position and what makes me both optimistic and cautious about how it plays out (this is just a typical 2% position for me so I’m not betting the farm).

Yesterdays Smith Micro

Smith-Micro has been a bad stock for a number of years. But it used to be worth a lot. This was a $400 million market cap company stock back in 2010. Revenue in 2010 was $130 million.

At the time revenue relied on a suite of connection management products called Quicklink. This suite of products maintained and managed your wireless connection as you moved around with your USB or embedded wireless modem (remember those!). They also had a visual voicemail product that transferred voicemail to text and provided other voicemail management features (in fact they still do have this product).

From what I can tell it was Quicklink that was driving revenue. They had 6 of the 10 big North American carriers onboard and 10%+ revenue contributions from AT&T, Verizon and Sprint. It was a cash cow.

Now I haven’t figured out all the details of what happened next, but the short story seems to be that the smart phone happened. Smart phones had embedded hot spots or mobile hotspot pucks for accessing mobile broadband services. No more dongles, no more laptops looking to keep their connectivity. And the connection management product was no more.

That was pretty much it for Smith Micro. The company never recovered. 2011 revenue was $57 million. 2012 was $43 million. By 2014 it was down to $37 million.

Today’s Smith Micro

The struggles have continued up until today. Over the past few years the company has had a difficult time creating positive EBITDA and revenue growth has been in reverse. Revenues bottomed out at $22 million last year. It’s gotten bad enough that the company included going concern language in the 10-K.

The company currently has a suite of 4 applications.

CommSuite is their visual voicemail product. It is still used after all these years and generates about 60% of revenue. QuickLink IoT seems to be a grandchild of the original Quicklink products but with the focus on managing IoT devices. Netwise seems like another Quicklink spin-off, managing traffic movement for carriers by transitioning devices from expensive spectrum to cheaper wifi where they can while insuring that an acceptable connection is maintained.

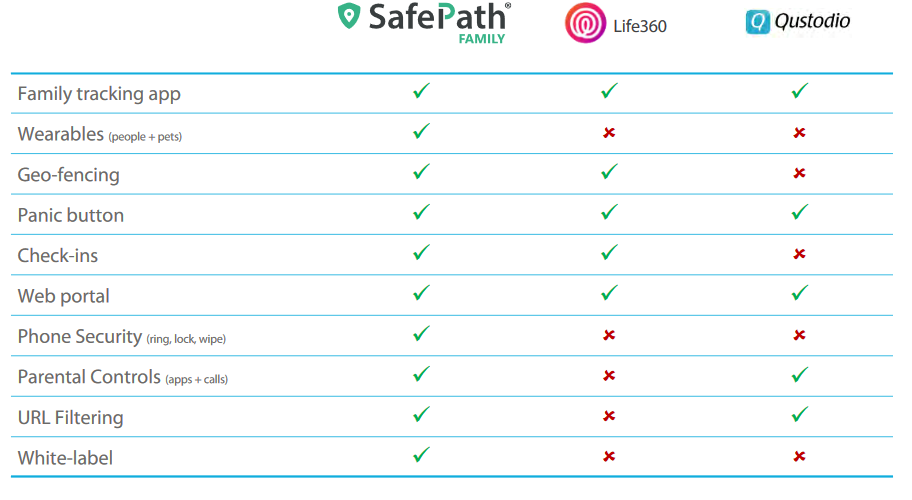

So those are the other products. But there is only one that is really worth talking too much about and that’s SafePath.

SafePath is a device locator and parental control app. With the app installed on all devices in a household a parent can keep track of their kids or the elderly (or spouse for that matter) as well as control and limit what apps and access each device has.

Smith Micro gave a rundown of the SafePath functionality in their latest presentation, comparing it these app store based competitors.

Essentially what these apps let you do is a combination of:

- Keeping tabs where all the other devices in your network are including geofencing alerts if the location is unexpected (ie. children not in school)

- Panic button if a family member is in trouble

- Content constraints on what apps can be downloaded onto each device, what websites can be visited

- Time constraints and time limits on when apps and web content can be accessed

- A history of device usage, location

I think it’s a pretty useful product. I actually didn’t know that so much functionality was available for parents to control what their kids have access to (my kids aren’t at that age yet but I could see a product like this being a purchase for me one day).

SafePath isn’t a unique offering. There are several apps on the market that offer a combination of the features. Each carrier seems to offer some sort of flavor. And there are freeium products available at the app stores, such as Life360 and Qustodio which are the comps used in the table above.

Both the Life360 and Qustudio apps are not associated with any carriers. You get them via the app store and you get some reduced version of the product for free (can only track a couple member of the family, don’t have all the controls, etc). You upgrade to the premium pay version if you want all the features.

For the premium version the pricing on the Qustudio app is between $4.50 to $11 per month depending on the family size. I believe the Life360 app costs $5 per month but I can’t really find recent information on that, and I would need to sign up to get pricing via the app itself which I can’t do here in Canada.

Before I talk about the SafePath pricing, I want to mention that maybe the most important differentiator for SafePath is the white label. Rather than providing a product into the app stores, Smith Micro licenses the app to carriers. They put their own labeling on it and offer it to their clients.

That’s where Sprint comes in.

Why SafePath?

Last fall Smith Micro added Sprint as a SafePath customer. Sprint obviously is a huge win, with 55 million wireless customers.

Sprint has named their version of the app Safe & Found. The product was launched near the end of 2017 but didn’t really accelerate until the last couple of months.

Prior to Safe & Found Sprint offered a product called Family Locator that provided location detection for families. They had a separate app for parental controls called Family Wall. These products didn’t work at all on iOS.

Combining the functionality into a single app that’s available on all operating systems is likely part of a bigger strategy. At the LD Micro conference William Smith, the CEO of Smith Micro said this:

[Safe Path is] an enabling platform for a carrier that is looking for a strategy to grow their consumer IoT devices… [such as] wearables, pet trackers, a module that goes in your car and lets you track your teens driving, a panic button that you give to your parents…

Putting together a single product geared at families is about attracting families to the carrier. Families are low churn and high dollar value customers.

Sprint is selling the Safe & Found app for $6.99 per month, so in-line with the other apps that are available. Smith Micro has a revenue sharing agreement, taking a cut on each customer. Apparently, Smith gets about $3/customer/month from Sprint (though I haven’t been able to verify that number).

The Sprint Bump

Ok so now let’s throw out some numbers.

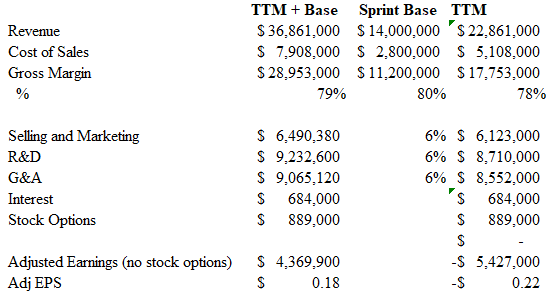

Smith Micro has about 24.5 million shares outstanding. At $2.50 that gives it a market capitalization of $61 million. There is about $10 million of cash on the balance sheet (maybe a bit more but they are still burning cash so call it $10mm) and $1.5 million of debt.

TTM revenues were about $23 million and gross margins are 75-80%.

Now let’s look at what Sprint does to those numbers.

On the fourth quarter conference call Smith said:

While the conversion of Sprint’s existing customer base is still underway, it will equal approximately $3.5 million in additional quarterly revenue for the company once it’s completed.

That’s including breakage. So this is a $6 million revenue per quarter company that is guiding that it can add $3.5 million a quarter on a Sprint ramp? Obviously, that’s the opportunity here.

The company said that margins on SafePath will be around 80% and that almost all that margin should fall to EBITDA.

Not surprisingly, if you model this out the company becomes much more attractive.

The above assumes 6% operating cost inflation (gets you to $6.2 million per quarter).

An analyst on the fourth quarter call said Sprint’s installed base was about 300,000 customers, so the above would assume a ramp of those customers (with breakage) to Safe & Found (I would really like to have this number verified though, I can’t find evidence of how many Sprint’s Family Locator subscribers there are anywhere else). Its worth noting that if the 300,000 subs is accurate it is is less than 1% of Sprints installed base. So there’s clearly lots of blue sky if all goes well. On the fourth quarter call Smith said that:

I think it is the goal of not only Smith Micro but also of Sprint to see millions of subs using the SafePath product and that’s a goal that, I think, would be echoing in the executive aisles of the Sprint campus as well.

So we’ll see. The numbers can get quite big when you are dealing with 80% margins and a large installed base.

Can Reality match the Model?

That’s the big question. Are these numbers achievable?

Look, I take small positions in a lot of little companies that give a good story. I tend to take management at face value.

This is a bit unconventional. I get called out for it by more skeptical investors. When these investors are right, which is more often then not, then they get to gloat and I get to look like a naïve fool for trusting management.

But bragging rights aren’t everything. There is a method to my madness and that method is that when I am right, I sometimes get a multi-bagger out of it. The big wins drive the performance of the portfolio and while on a “naïve-fool-basis” I come out looking poorly, I also come out profitably.

Nevertheless, I always try to keep it at the forefront of my mind that there is a pretty good chance that this isn’t going to end well.

With Smith Micro I’m taking management at face value. If they say they can do $3.5 million a quarter from Sprint, then okay, I’m buying the stock on the basis that they do $3.5 million a quarter from Sprint. They say the goal is for millions of subs then I say, okay, lets see that happen.

But I also recognize that might not happen.

My Concerns

Honestly my biggest hang-up with the stock right now is the reviews. The reviews on Google Play could be better.

I recognize you have to take these reviews with a grain of salt. First, they make up a very tiny percentage of the total downloads so far. Gomes put together a very helpful table of his estimated downloads and the reviews that have been added. Reviews are much less than 1% of downloads.

Second, its not clear that the reviews are all legitimate. I haven’t done this, but some others have dug into the reviews and questioned that they are often coming from locations that aren’t even in the United States.

Third, apart from a few legitimate concerns like battery drain (which other reviewers actually contradict), most of the reviews seem to be more about complaining that the Family Locator app they were used to is gone. Fourth, the trajectory of the reviews has been getting better.

Nevertheless the reviews are a datapoint and right now a somewhat negative one.

My second hang-up with the stock is that, at least from what I can tell, Sprint hasn’t completely shelved their legacy Family Locator app. On the first quarter call Smith said this:

The legacy product was originally due to sunset in the first quarter of 2018, but has subsequently been delayed for several months. This change was based solely on Sprint operations and was not a result of the SafePath application or change of our contract status.

Why has Sprint delayed the sunset? I have no idea. It could be (probably is) a completely benign reason. But again, it’s a bump in the road to weigh against the $3.5 million a quarter that I am taking at face value.

My third concern is that management hasn’t been on target with their projections. Originally they said the ramp on the Sprint installed base would be complete by the first quarter of 2018. That turned out to be way off. They were also positive on a Latin America carrier win that doesn’t appear to have panned out.

Finally, concern number 4 is that we are dealing with a service provider. These guys are A. Slow to adopt, and B. not at all loyal. We’ve already seen point A prove itself out as the ramp has lagged. Point B is something I’ve already experienced with Radisys, which was dumped unceremoniously by Verizon. Smith Micro has had this experience multiple times in its history, most recently by Sprint themselves when they dumped their NetWise product after what Smith Micro called a promising launch.

These are all reasons this is a 2% position for me.

On the other hand, Sprint does seem to be moving ahead. There was a big promotion in May including a joint deal for AAA members (talked about here), reps have been visiting stores and getting the sales staff up to speed, and stores are promoting the app to varying degrees.

One other potential positive is that Sprint might not be the only Tier 1 win. The CFO, Tim Huffmyer, presented at the Microcap conference in April. He mentioned a second win with a Tier 1 European carrier.

Huffmyer said that they had already been selected as the family safety application for this carrier but that the contract process was still ongoing. If they get the contract finalized it would be rolled out to Europe, Asia and the Middle East where this carrier operates. He didn’t give any more details on size but presumably it would not be a small rollout.

I know from painful experience how slow Tier 1 wins can be. But quite often they get around to it. It’s a good sign that they are moving down that road with others.

A Typical Stock for me

This is a Mark Gomes pick and I am stealing it. But I am stealing it because it fits right in my wheel house.

There is no question the stock could be a dud. The Sprint ramp might stagnate, Sprint might walk away and go back to the incumbent or to some other option, and then there is the merger with T-Mobile that throws yet another wrinkle into the equation. Who knows what’s in store?

The one thing I do know is that if the launch is successful and Smith hits their targets, the numbers are big enough to justify a higher stock price. Viable growing businesses with 80% gross margins and a recurring revenue model don’t trade at 1-2 times revenue. Simple as that.

So this is a classic stock for my investing style. An uncertain opportunity that has some positives, some negatives, no sure thing, but an upside that is more than large enough to make it worth throwing your hat in the ring.

How often do these sorts of opportunities pan out? Definitely somewhere south of half the time. If it doesn’t then I get to look like a naïve fool for trusting management. But if it does I get a big winner. It’s these sorts of moonshots where the 5-baggers come from. And that’s what drives the out-performance. Crossing my fingers that Smith-Micro will be next.

Hi,

Great article (and thanks for the plug). I follow your blog on my WordPress app (GREAT app!) so imagine my surprise this AM. Nice to finally see someone else writing about SMSI — I’ve LITERALLY been the only one.

FYI, the answer to all of your questions / concerns have been previously answered in my blogs. However, as you point out, it could take days to read through it all. As a 24 year Wall Street vet, I was trained to be thorough. Better to know everything about 5 stocks than a little about 50.

Anyways, allow me to assist:

1. The Reviews: A LOT of them are absolutely fake (the bad ones AND the good ones). The competition started by attacking with fake negative reviews and Sprint seems to be striking back. It’s like what Disney did with Ant Man & The Wasp. They boosted the mediocre (67% rating) reviews to make it look like an 81% rated movie.

The similarity doesn’t stop there. To get the real review, you have ask people you trust or SEE IT YOURSELF. That’s how I research things. I give Ant-Man/Wasp a 65 and I give Safe & Found 4.5 stars.

If you don’t trust me, trust this… the reviews have risen EVERY month https://docs.google.com/spreadsheets/d/1e1dSDqV08mlsZ0LE0lOc1f1d677NfLXWb8UxzGfUbns Before April, it was 2.15, in April 2.79, May 2.99, June 3.79. It’s closing in on my personal 4.5 — my complete review in on my site somewhere.

2. There indeed WERE about 300-350K Location Labs customers. Many are now Safe & Found, but your question is “how do we know it’s 300-350K?”. Simple triangulation of management commentary. Many professional investors (me and others) have all come up with numbers in the same ballpark (which is close enough to understand SMSI’s opportunity). Similarly, SMSI’s $$ per sub is a function of that same triangulation.

3. Sprint delayed the sunset because their legal department said they couldn’t replace a $5.99 product with a $6.99 product. Being a big slow corporation, it took months for them to realize that all they needed to do is offer it for $5.99 to existing customers.

Their FAQ now reads as follows:

15 day FREE trial of full functionality is available for all new customers.

• $6.99/mo.: Provides full functionality (location, parental controls); monthly recurring charge per account for up to 5 devices.

• $5.99/mo.: Provides location only (only available for legacy Sprint Family Locator users who opt in during the free trial)

• $4.99/mo.: Provides parental controls only (only available for legacy Sprint Family Locator users who opt in during the free trial)

FYI, they also give 30 day trials. SMSI gets paid-in-full on anything past 15 days. They also get their $3.00-3.50 per month no matter how much (or little) Sprint decides to charge. So, if Sprint thinks it’s so critical for locking in customers, they can give it away if they want, as long as they pay SMSI their $3.00-3.50.

Addressing your next concern, management didn’t meet their target date for the switchover because of the mishap(s) at Sprint. Not their fault, but they should have known better than trust a big corporation to stick to deadlines. Half credit; half blame for sure.

Regarding carrier loyalty, TRUE. That’s the double edged sword of dealing with carriers. On one hand, SMSI is one of only a few companies capable of selling apps into carriers (relative to the total number of app vendors). This is a HUGE advantage which will allow them to grow their business via acquisition now that there are so many apps in the world and so few vendors who can sell those apps to carriers.

On the other hand, the nature of carriers makes a SMSI very hit-driven, even more so than a video game maker. Of course, that can be good or bad for an investor. If you look at a 20 year chart for a SMSI, you can see that the stock has gone over $60 on multiple occasions and come down into the low double digits or lower on just as many occasions. The trick? Ride the highs and avoid the lows.

Over the last two years CEO Bill Smith has purchased tons of shares, becoming the company’s largest shareholder.

So, we all know where he thinks they are in the cycle…

Hope that helps. Again, kudos and well written and well balanced assessment. Your final paragraph was particularly on point and exactly how I think when deciding how much money to invest.

Cheers!

Thanks Mark, really helpful comments. Appreciate all the work you’ve shared on the name.

I bought a small position this stock at 1.77 after reading and subscribing to Mark Gomez blog. It has been up over 50% since then, but is volatile.

True. It’s almost as volatile as the last letter of my name, which appears to have transformed from an S to a Z again 😂😂😂

Mark – any concern about their app becoming obsolete with the upcoming iPhone updates in iOS12:

https://www.google.com/amp/s/amp.usatoday.com/amp/672232002

Thanks

No. Please see my past posts. This was discussed in depth last month.

Stock sold off a little when this was first announced, but has since broken out.

Also read my latest posts. One features a data point where a tech savvy store associate shows how Safe & Found can be used IN CONJUNCTION WITH Apple’s capabilities to create a full experience for customers.

That’s exactly how I view it… and why bought more on the selloff (which earned me a quick 10% when it rebounded).

Hope that helps,

Cheers!

Mark thanks for the link on your comments about Apple / google. I do remember there being a big push for them to address the teen phone addiction and seeing this launch in iOS 12 makes me wonder about the obsolescence of S&F. It sounds like Apple will be putting all features into one app which should be a bigger deal than in the past where it was a pain in the ass to access all features. I need to dig in some more I think to understand their features vs S&F.

I think your comment about cross platform isn’t really that big of a deal but I could be wrong. I’d have to imagine most families looking to pay for S&F would be using the same platform (ie all Apple or all android)

Aren’t they going after an install base that is currently using Sprint Family Locator that doesn’t have any parental controls? Also I thought that install base was all android?

Not necessarily. The Family Locator users are aimed to converted to S&F, but they are not the only ones. Sprint’s other customer base is not only on Android and especially not all family members are on Android. Maybe the father has Android and the kids Apple. Or the other way round. So cross platform is a big thing and widens the TAM especially with a look at other carriers.

Yeah I’d imagine there’s plenty of incumbent users that will just roll over. Also, I always forget just how big the country is. Shit, there’s still people on AOL dial up. All it takes is a few hundred thousand users to be convinced out of a population of hundreds of millions and its a game changer for a company like SMSI

To bring some balance to this comment section with some negative remarks 🙂

-number of families with small children is probably a lot smaller. Total number of families is 80 million. Then there are slightly less than 50 million children between 6-17. Then not everyone will use this app, and some families have two children. Still a potential TAM of 10-20 million users though. But that would be a blue sky scenario.

-legacy business seems to be in decline and bleeding money. What % is steady state earnings and what % is investment in new product? They don’t seem to break that out. Because $4m in earnings on a $50m+ market cap does not seem all that cheap? And that is a pretty bullish scenario, assuming legacy revenues stay stable (that have been declining fast). Why can’t they earn more money on their legacy business? As more than $20m in revenue with high gross margins is pretty sizable. Often run off operating margins of software businesses are in the teens.

-For 2x revenue or less you can buy better software stocks with better ramp up prospects of new products that have synergies with their current projects, that have a growing core business to boot like Getbusy, Dillistone, Yangaroo or Intouch insight

-Large reliance on a big client

-Glassdoor reviews are probably quite important for software companies. None of them sound positive really. If key talent cannot be retained you can be stuck with a codebase that is hard to learn for someone new. And some of them are pretty bad:

” The management team, including the CEO, is completely incompetent and should be terminated immediately. The CEO is as narcissistic and crazy as Donald Trump and is the ONLY employee that has ever worked for the company that has attained any real wealth.

In the 35+ year history of the company, one thing has remained constant — the CEO Bill Smith. He has fired/ran off many great people and has managed this company so incredibly poorly that it is worth a mere fraction of what it could be had a qualified CEO been given the opportunity to run it. The culture in the company, set by the CEO, is one of fear, distrust, and disillusionment. He constantly pits people and teams against each other and he has no loyalty to anybody in the company except 2 maybe 3 people. The rest are simply disposable workers that are there to try and help him regain some of his lost wealth. This CEO is undoubtedly one of the worst CEOs of a tech company ever.”

Given all that I don’t see how the valuation looks all that compelling at current prices?

Thanks to everyone for the comments. I kind of think of this idea differently then everyone else. To me the only thing that matters at this point in the story is if the app gets adopted and they take the Sprint base. I don’t see how there could be a successful deployment of the app, where they acquire the 350k Sprint customers and add some more new ones from Sprint, and the stock isn’t much higher (even 2x revs on that scenario is a 40% bump). So isn’t the story all about whether that ramp can be successful or not? I don’t really see the rest as being all that relevant. I pointed out a number of reasons in the post to believe the ramp won’t be successful and I’ll stick by those as valid worries. But the other questions, like what the real TAM is, what the CEO is like, what Apple is doing, that all their revs come from Sprint, I don’t know… I’ll worry about those things once the ramp question is answered one way or another. And if the ramp a bust then I won’t worry about them at all!

Good points, especially the Glassdoor reviews are hefty. Are they 100% reliable?

But I think Sprint is pushing this really hard. For them S&F is one of the few ways to differentiate themselves from other carriers. Sprint needs to lower their own churn rate. The wouldn’t roll it out in such a way as Mark has documented only to drop it weeks later.

Also, if the Sprint thing is a success, SMSI has big credibility against other carriers. That would open the way for new clients in Europe, South America, to which Bill Smith seems to have already some contact.

I’m taking a look at YOO. Can you explain it to me a little? I see some rev growth yoy, and the margins are high but what exactly do they do? And why is the stock chart so bad – its down more than 40% since the beginning of the year? Thanks

YOO? Never heard of…

I was replying to Arfs comment

Sorry, wrong comment.

Description of their product from two analyst reports (cannot find them on google now for some reason):

from:

Euro Pacific:

“The Edge in DMDSTM – Low Cost and High Reliability

Traditional distribution technologies rely heavily on dedicated serves at the broadcaster site. Moreover, manual operations are routinely required to conduct quality checking (QC) and taking corrective action on video files. Considering the North American distribution footprint of 8,500 destinations, an acceptable distribution solution would deliver a video file within a two-hour window limit. Through DMDSTM, agencies and broadcasters have an option to distribute files via the cloud thereby reducing costs by eliminating dedicated ad servers and satellite links. In addition to being cost effective, YANGAROO’s delivery implementation over the cloud is fast, meeting the two-hour window threshold with the ability to distribute ads in one hour for premium service. DMDSTM also comes with workflow management tools that decrease workload on media network staff and deliver the lowest failure rate versus the competition. To sum up, we argue the combination of cloud technology, robust QC checking, and intuitive workflow management tools address the industry’s technological challenges of the status quo. This is achieved with improving efficiency, reducing workload, and bringing about faster service at relatively lower infrastructure costs.

The Competitive Landscape In Video Distribution

We estimate the market size for the TV video advertising business at US$300-350M, which is dominated by Extreme Reach, a private company, with a market share of 85%. Extreme Reach also has a cloud based solution with 32,000 platform users and distributes videos for 9,000 brands and agencies. Unlike YANGAROO, Extreme Reach goes beyond ad agencies and considers brands and advertisers as potential clients to acquire. The platform also provides capabilities to manage workflow associated with creating and producing a TV or video spot, including talent acquisition. By leveraging its capabilities, Extreme Reach has been successful at extending its influence upstream in the value chain and connects directly with brands and advertisers to secure market distribution flow. Other players either use antiquated technologies, or have underperforming solutions. These competitors hold a small footprint and operate the advertising business as a non-core add-on.”

And another report by Global Maxfin Capital:

“Fundamental to the YANGAROO story is its Digital Media Distribution System (DMDS) technology, which it uses to serve its three industry segments: (1) Advertising; (2) Music; and (3) Awards Shows.

The DMDS enables advertising agencies and broadcasters to digitally transport data from their media and traffic management systems into DMDS. The DMDS eliminates the need to re-key data, reduces the potential for error in the distribution process, and makes it easier for customers to integrate with YANGAROO while maintaining their existing systems and workflows.

Users upload content (i.e., audio, video, images, and documents) to a cloud-based platform, in which files go through automated preliminary quality checks. Once uploaded, the file is secured through a biopassword authentication, digital watermarking, secure file encryption, and access rights management. Upon delivery, the file goes through a secondary automated quality check and sent as directed, to radio, television, publications, or blogs. The platform has the ability to send to 8,000+ distribution points in over 200+file formats.”

I think reason for drop in share price is low liquidity. And probably investors who got in early 2017 taking a profit, since Q1 did not see a large jump in revenue as hoped? There were a few large trades that jumped up the share price, then liquidity dried up when Q1 did not show significant growth. And historical chart looks ugly. I think it just takes time for these type of things as once a customer uses their service, it is really sticky. So it also takes a while to win customers. I think it takes about a month to get customers on their platform.

But last Q’s outlook was pretty positive, they seem to have a pipeline of large deals that might show up in H2 2018. Just a few million in additional revenue would massively increase earnings, as 75% of costs are fixed.

What makes me optimistic about their prospects of taking market share is that Chairman seems pretty well connected in the ad industry they are trying to break in. And he bought a lot of shares late last year.

They got a failure rate of 2% vs 15% of next competitor (see page 16 of presentation), plus they seem to be the cheaper option (possibly due to newer tech as they built their ad platform later?).

Extreme Reach has been slipping with a lot of outages in 2016 and is close to a monopoly, so customers are looking to diversify to a strong number 2 player (which would be Yangaroo with only about 1% market share now and only other player with comparable/better platform).

They seem to have all the broadcasters, consumer companies and ad companies signed up already, they just need to increase usage (amount of files sent through). They aim to take 10% market share in advertising, which would mean more than 50% profit margins (Extreme Reach has 50% EBITDA margins). or about $20m in ebitda.

They got close to 100% market share in radio and award shows in the US already. It looks to me like a long term call option with little downside risk at this valuation.

Hope that helps 🙂 Curious what you think about this.

I also am building a posn in SMSI and also got the idea from Mark, my primary concern is the stock price. Shares are still very cheap based on cost ~$2.50, (not looking at anything else). I don’t yet see why more deep pocketed investors haven’t taken posns. before the actual numbers are achieved and reported. If that comes to fruition you’re looking at a $10-$12 stock pretty quickly. Even a 500k – 1m share posn isn’t that costly with potential returns and for very many speculative investors and funds. I’d like to see that for my concern to be allayed

Hi Lane, how do you feel about SMSI now?

I sold some because of the run up and because as I dug into the last quarter more it didn’t really seem like S&S was the driver. But since then its gone up more so I was wrong about selling.

There has been huge insider buying, that attracts me, but wish they were cashflow positive.

Check out this post by Mark Gomes with upbeat SMSI forecasts. He’s been detailed, intelligent, accurate, and his analysis looks promising: https://markgomesstocks.wordpress.com/2018/10/17/more-on-how-to-profit-in-the-selloff-includes-smsi-hear-pott-stocks-etc/#comments

Thanks I listened to Gomes last video and have read this. Gomes of course knows much more about SMSI than I do. His estimate of 100k subs for S&F in Q2 would be quite bullish.

My concerns is that the Q2 numbers were so good, that there is a reasonable chance they come in below them this quarter. Revenue has always been lumpy, and Q2 revenue gains were only partially driven by S&F (I think about $400k). So if they come in at $6.5mm or even $6.7mm what does the market do? I realize that the analyst estimate is $6.1mm so maybe that is still considered a beat. I’m just not totally sure the market looks positively on sequentially down numbers especially if we are still in correction mode.

I might be totally wrong. They quite possibly could blow away the numbers and the overall market correction could be over. I’m just being cautious.