Week 387: My Recessionary Portfolio

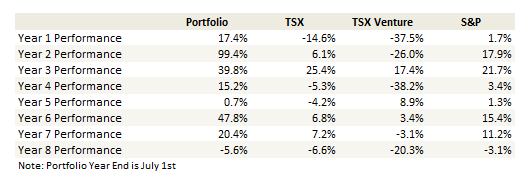

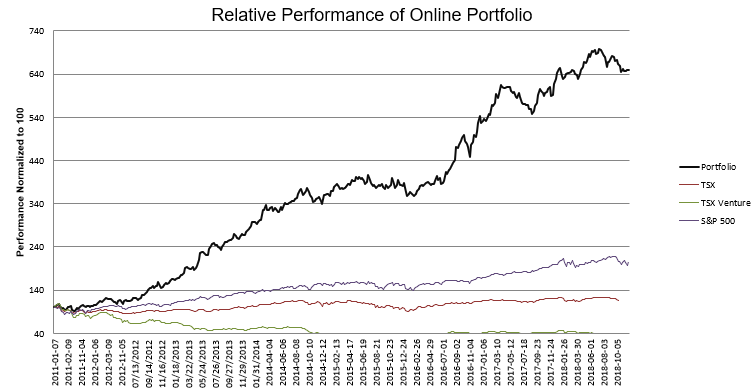

Portfolio Performance

Thoughts and Review

I haven’t written in a while. I don’t have much to say, the markets are brutal and I am in no hurry to start picking new stocks. So its not a lot of fun writing.

I have continued to sell stocks in the last two months. My already high cash position is even higher. I’ve hunkered down.

I see no choice but to continue to sell. The problem is that with the small and speculative stocks in a bear market the only safe place is cash. So even as I went into the fall with a very high cash level, over the last 8 weeks I made it even higher. As of this weekend the online portfolio I track with this blog is at 75% cash. That trails my actual portfolio, which is now up to 85% and my RRSP is basically now a GIC.

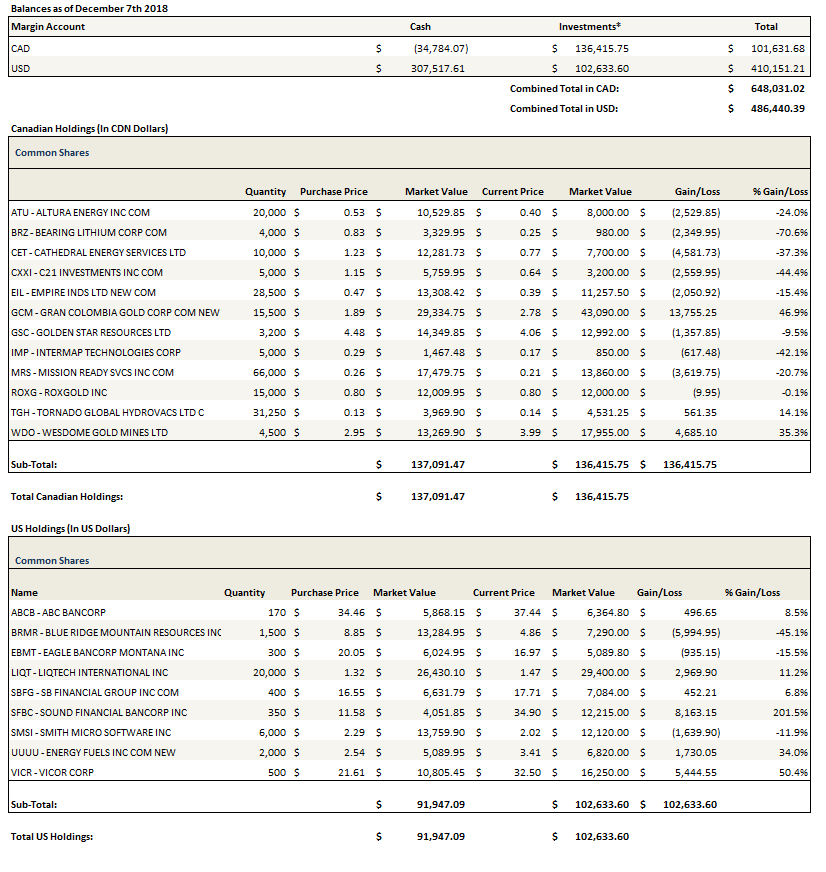

I even sold my long-held bank stocks this week (not reflected in the portfolio below, which I updated for December 7th). It’s a bit of a personal watershed for the portfolio and the blog.

I rarely have talked about these stocks since they are boring, but they have been great performers for the last 6 years. I’ve held them through pretty much the entirety that I have been writing this blog. Which is to say some tough times! Yet with the yield curve inverting and leading indicators rolling over I decided to finally exit the trade. I sold Sound Financial, SB Financial, Eagle Bancorp, and ABC Bancorp (they were the firm that took over Atlantic Coast Financial). It was the end of a era!

That I am selling these stocks, which I held through some crummy times in 2015 and 2016, should tell you something. I’m pretty bearish on where the economy is at.

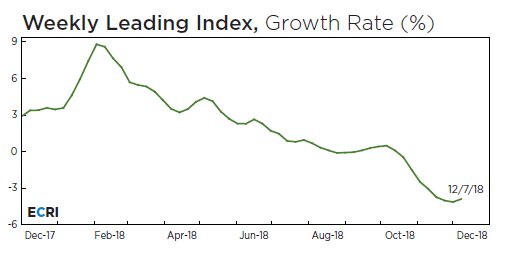

The weekly leading indicators put out by the ECRI were at 144 week lows before a slight uptick this week.

The pH report recently said (also in a Real Vision interview which I’m not sure I can reproduce here so I won’t) that they thought we were on the cusp, if not in, a global recession.

Chemicals are the best leading indicator for the global economy. Data for both Chinese and global chemical production are warning that we may now be headed into recession.

On top of that we have the Fed raising interest rates and quantitative tightening, which are reducing the availability of credit.

And then there’s the trade war.

If this isn’t the tide going out, I don’t know what it.

Look, I’m not the smartest guy in the room. All of the funds and firms and experts undoubtedly know more than I do. So I might be wrong and maybe this is another pause, another correction, before takeoff.

What I do know is to respect my limitations. And trying to guess the bottom in a market that is in a downtrend on top of a bunch of negative economic data just seems like a foolish exercise to me.

No one is paying me to take risk. So when the environment isn’t conducive, why should I?

The last time I did something like this was January 2016. That period turned out to be a false alarm. This one might too.

This is what I wrote in my February 2016 blog post.

The point of existence of a hedge fund is to risk money in order to make more of it. You can argue the particulars of that statement, that risk reduction can occur through various hedges, diversification, concentration, whatever your flavor is, but the bottom line is that the money should be at risk somewhere or why is the fund even there?

But that’s not my job. While part of what I am trying to do is of course maximize my profit line, my first mandate is also very clearly and in capital letters, TO NOT BLOW MYSELF UP.

What I guard against with absolute vigilance, is insuring that my capital doesn’t permanently disappear.

You can look back on these comments and say they were poorly timed. February marked the bottom, the market started to recover, in the fall when Trump was elected it really took off.

But the reality is that I greatly benefited from that rally. My Year 6 performance (the table at the beginning of this post) from June 2016 to June 2017 was one of my best 12 month periods. The market turned and so did I. If that happens again I’ll turn on a dime just like I did then.

But I’m not going to sit around and wait for that turn while the market grinds lower.

You can look through my portfolio and look at what I sold. I’m not going to go through the whole lot. What I’ve held, I’ve done so for two reasons.

First, most of these stocks aren’t terribly economically sensitive. Liqtech isn’t go to sell less scrubber filters because the economy is slowing (in fact a lower oil price probably means they sell more).

Second, the TSX Venture has already gotten creamed. The few Canadian stocks I hold there have not done great, but they’ve done okay. This seems like a bad time to throw in the towel there, especially since the positions are small.

And then of course there is Mission Ready which apparently isn’t going to trade again until the next decade. Not that I’m complaining. If I had the option to put all my stocks on a trading halt for the next 12 months I think I’d have to consider that.

(As an aside there was a piece of bullish news out of Mission Ready just released on Friday. One of the company insiders exercised their 15c warrants that expire in a week. One would think that an insider would not exercise warrants if they thought the Unifire deal was going to fall through).

So I don’t know. Maybe I will find another compelling recession proof stock that will compel me. That might be a hard proposition. If not, and if this is more than your run of the mill correction, then this blog might be a bit boring for a while.

I’ll tell you though that when I see the turn, I’ll be in the middle of it.

So I did take a small Canadian oil position this week. I don’t know how long I will hold it so take this for what its worth.

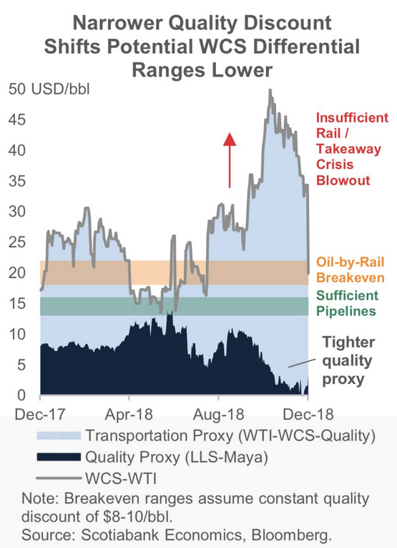

Gear Energy. I owned it before and sold it after Western Canada Select spreads blew out. The stock fell apart like I thought it would. But in the last week and a bit the mandatory production cuts implemented by the Alberta government have worked wonders on Western Canadian Select differentials.

Part of the mandatory cut is that companies producing under 10,000 bbl/d are exempt. In fact companies under 10,000 bbl/d can actually produce up to that level before being affected by the cut. I was surprised to find this to be the case.

Before being forced to shut-in production in November Gear was guiding to 7,500 boe/d. They have an acquisition that will bring that up to nearly 10,000 boe/d but those assets are in Saskatchewan and so they shouldn’t count toward the ceiling.

Small companies like Gear (and Altura Energy, which I continue to own) are in the unique position of benefiting from the spreads and having the ability to grow. I don’t know if the market will see it that way. I have heard the argument that capital just won’t come back to small-caps period. Maybe so.

I haven’t run the numbers for Gear but I did a detailed type curve model of corporate production for Altura and found that at C$40/bbl realized prices they can drill 5 wells next year, stay within cash flow and grow production slightly. Right now WCS prices have risen to over $50 (the latest PSAC quote has them at $54). At those prices Altura can grow production significantly (10-20% I think) while staying within cash flow. I’ll maybe do a post of my model there shortly.

These companies aren’t in a terrible position any more.

No guarantees I keep any of my positions. All comments in this market have the life expectancy of a hand grenade.

Portfolio Composition

Click here for the last eight weeks of trades. Note that this update is of December 8th, so it is a week old and doesn’t have my small purchase of Gear, my bank sales or my sale of Smith-Micro.

{kind=link}

Great stuff as always although I was surprised to see you jettison R1 when it’s just hitting its stride. Between the last few quarters of demonstrated margin expansion, Ascension ramping to normalized profitability in 18 months instead of 3 years (quite a tell looking ahead), torrid, contractually guaranteed revenue growth over the few years and the fact it operates in a recession resistant industry undergoing structural change that should benefit the company at the margin – to say nothing of its nonsensical absolute and relative valuation relative to healthcare digital IT peers, to name just a few of its attractive qualitative and quantitative characteristics, gotta ask – what’s not to love?

Plus you’ve got the Chardan and Citi initiations from September and December 10th respectively, making the days that this orphaned, underfollowed (increasingly dominant) secular compounder remains so, increasingly numbered.

In any case, what was the thought process here if you don’t mind me asking? Seems that wether viewed on an EV/Sales or normalized earnings basis, hard to imagine the common not trading at 2-3x the current quote looking out 12-24 months. If you’ve got any pushback I’d love to hear it.

I’ll echo the above sentiment on R1. Seems less economically sensitive and more secular growth. Most peers trade at 2-3X higher valuation. I’m wondering if there’s something I’m missing…