New Position in Digital Turbine

So far I’ve been pretty cautious about buying any stock that is economically sensitive. I bought some gold stocks, a couple healthcare/biotech names, but nothing that really is at risk of an economic downturn.

Digital Turbine is a departure from that. They are directly dependent on smart phone sales, particularly in the United States.

So with all the headwinds around smartphones and my own skepticism about the economy, why Digital Turbine?

I think it has potential, even in the return of a bad market, and there is more here than just following the smart phone sales trend. The stock performed extremely well while the market fell apart in December.

Digital Turbine provides a mobile device app management solution called Ignite. This isn’t an app-store app. Digital Turbine partners with carriers (they have 30 carrier customers including AT&T and Verizon) and OEMs (recently signed up Samsung, have another 7 smaller OEMs signed and have hinted at others to come) who install the apps on the phones before sale.

When a customer buys a phone from the carrier Ignite installs sponsored and partnered apps. These apps have been curated by the carrier and Digital Turbine based on the users preferences and from a list of app developers who have paid for the right to be included on the install list at the time of activation. A list of other sponsored apps that might interest the customer is also displayed during the set-up process.

In the past virtually all of Digital Turbines revenue came from these installations and recommendations at the time of activation. App developers paid Digital Turbine for those placements and installations.

Recently the company has leveraged their platform by adding a number of products that add value through the device life-cycle: Single Tap, Smart Folders, and Post-Install Notifications.

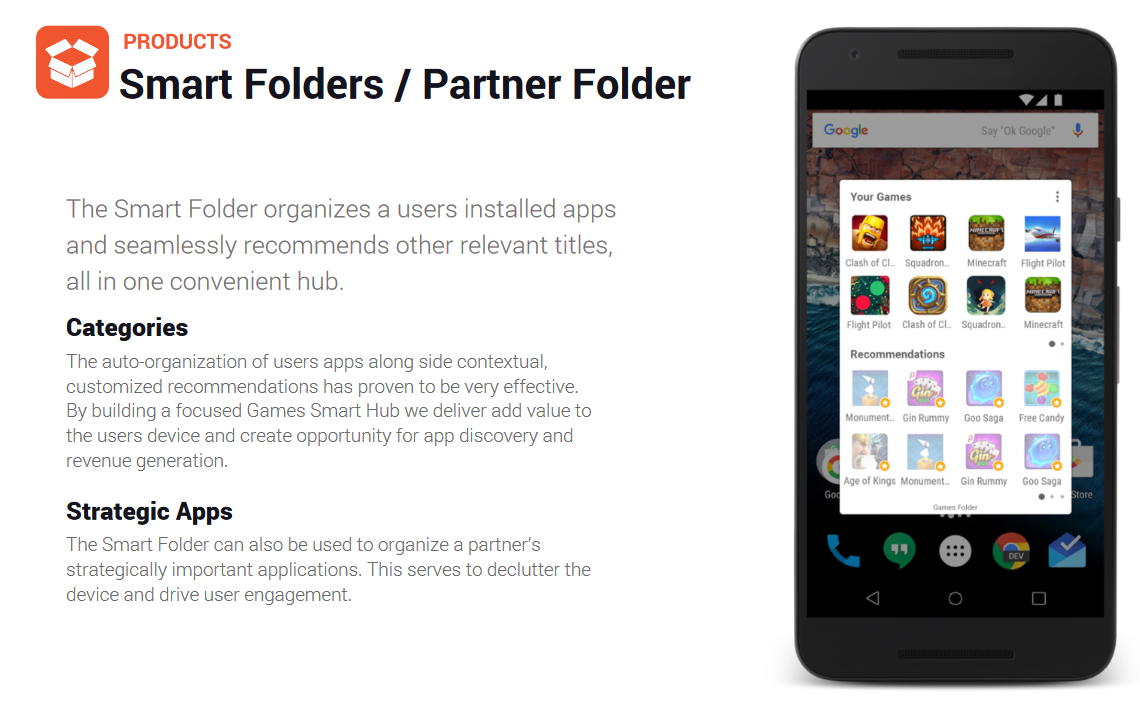

The Smart Folder app organizes apps into folders. Embedded in each folder are recommendations of other apps to download, which based on past preferences the user might find interesting. For example a gaming folder might be created for the users gaming apps. When accessing this folder they would see “similar” apps, which are sponsored content of other games that can be downloaded.

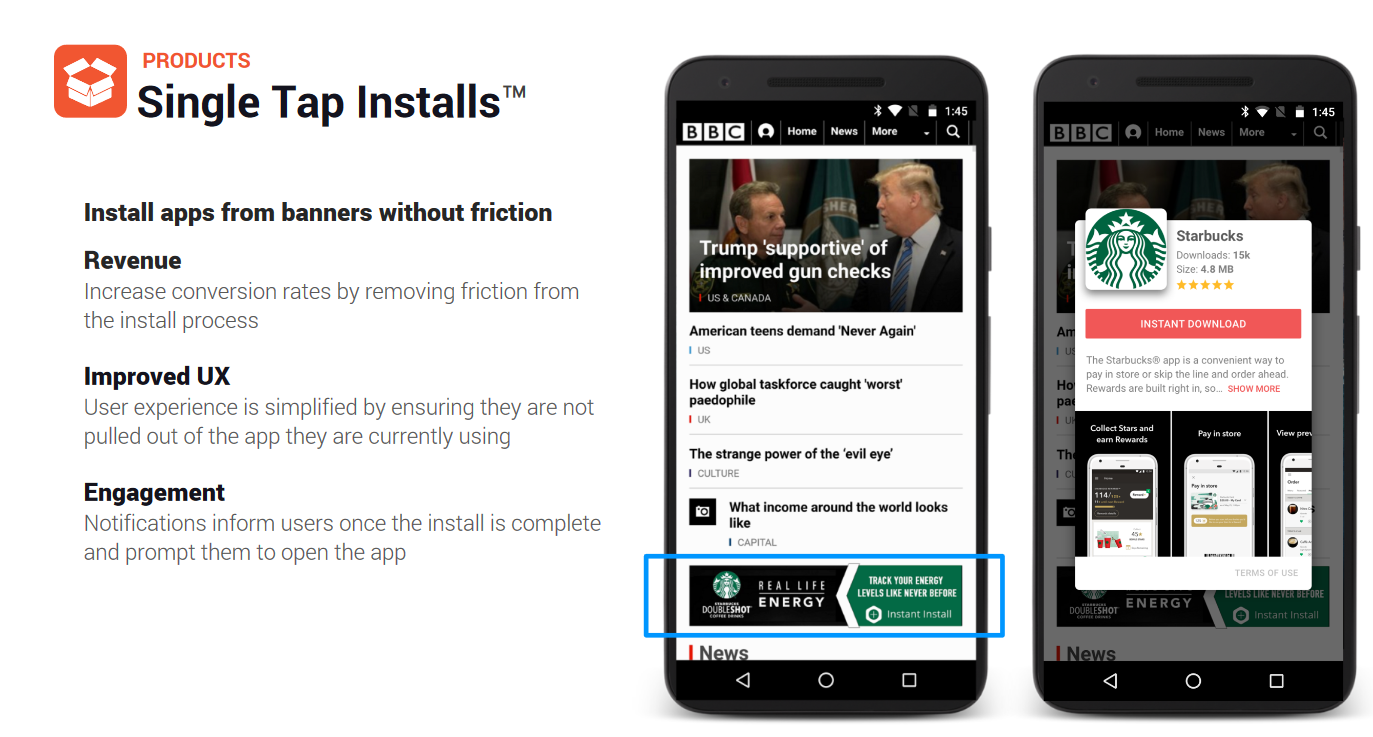

Another product is Single-Tap. This allows the user to download an app directly from a notification, advertisement or Smart Folder list without accessing the app store. Because the app is not installed via an app store, Google or Facebook don’t take their 25-30% cut. The app developer benefits with more revenue per download.

These downloads and placements also benefit the carrier. An important aspect of Digital Turbine’s business model is that the carrier is not Digital Turbine’s customer. In fact, when Digital Turbine receives revenue from app developers they pass on a chunk of it to the carrier. Rather than being dumb pipes, the carrier participates in revenue from each placement, install or notification that is generated (note: there is an exception to this if the carrier owns media or apps they want placed on the platform in which case they remit revenue to Digital Turbine for the placement).

It seems like an easy win for carriers. They put in none of the R&D, none of the marketing, but they get maybe 50% of the margins (its not broken out so that’s my ballpark guess) for simply putting the Digital Turbine platform on their phones. My understanding is that the carriers are also final decision makers on what and how much content is delivered via Ignite, so they remain in control.

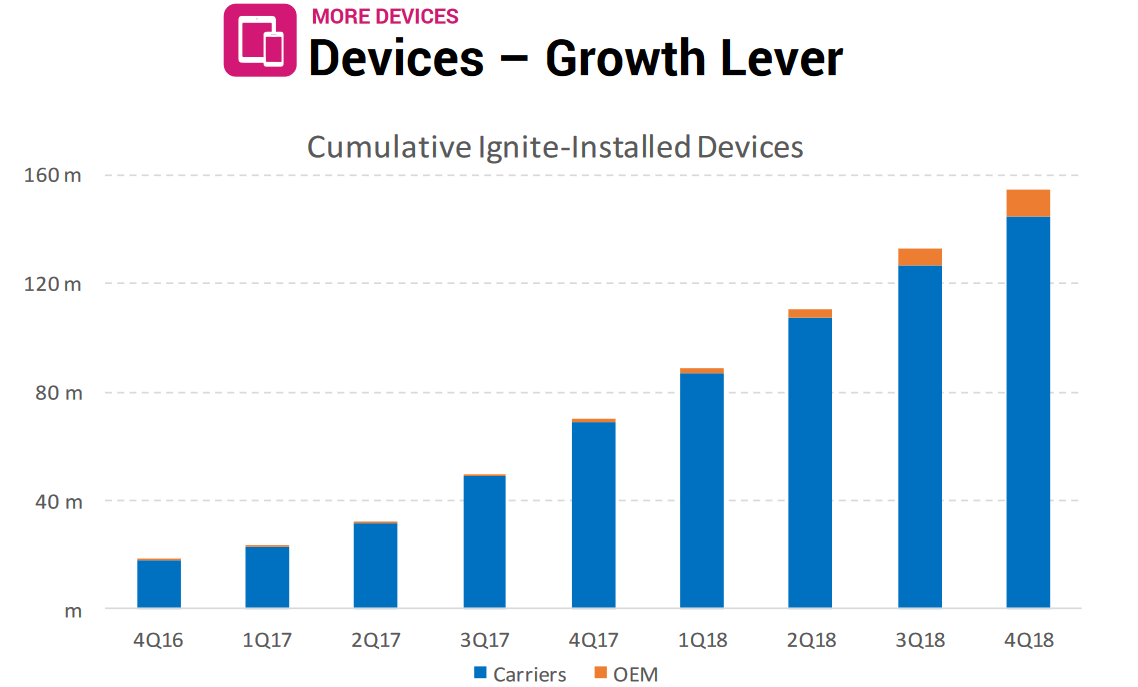

You can see the model is working. Digital Turbine is installed on 230 million phones right now. These are all Android phone (the Apple ecosystem doesn’t allow for this type of product). That is up from 155 million phone in March of 2018. They peg their annualized install rate at 100 million.

They don’t have a recent snapshot of their quarterly device growth but the snip below is from their Inventor Day presentation in June. You can tack on three more quarters (their year end was March) to get them to the 230 devices that are out there now:

Its a strong base (>10% of android phones) to layer on additional products. Carriers seem happy to comply since they are getting a nice cut. To wit, Single Tap was introduced about a year ago and its already on 120 million phones as per the conference call last week. While the post-install products have all been introduced in the last year, they already account for 15% of revenue.

Revenue is generated as app developers pay for adding their app to the pre-install process, adding it to Smart Folder recommendations, and for notifications or advertisements that are displayed. The agreements vary between app developers and between carriers but they either take the form of a cost-per-install (CPI) fee, a cost-per-placement (CPP) fee, or a recurring revenue fraction after the app is placed.

The recurring revenue is new, within the last year. They’ve already signed up Amazon, Netflix, the Weather Channel, Yahoo among others. If a user installs a Netflix, an Amazon or whatever app via the Ignite platform (be it a pre-install from a Smart Folder recommendation or an ad) then Digital Turbine gets a piece of monthly revenue from that app.

A year ago recurring revenue was nada. Now it amounts to 5% of revenue. It was 3% the previous quarter. Annualized that amounts to maybe $5 million but clearly growing quickly.

The latest big win for the company was Samsung. They made a deal with Samsung in the fall that added Ignite to Samsung’s factory install. Once it’s fully rolled out this could mean that Ignite is on every Samsung phone.

The OEM partners are important for international carriers where bring-your-own-device (BYOD) is much more common than in the United States. Until now an international carrier couldn’t do much to customize the experience of a BYOD customer. With Ignite pre-installed on the phone, they can turn it on and run through their own customized set-up.

While Samsung accounts for some 500 million devices on their own, Digital Turbine has hinted at more OEM relationships in the works (maybe LG, Sony or Huawei, which were all mentioned in passing on the last call?).

Right now revenue primarily comes from the United States carriers (AT&T, Verizon, T-mobile make up 85% of total revenue). International is growing. It was up 100% year over year last quarter with revenue from their large Latin American partner (which must be American Movil) tripling.

This is a business where both revenue and margins are a bit deceiving. Revenue is more recurring then you think. The company has an annualized install rate of 100 million devices, so the turnover from that base recurs every few years on a replacement cycle. The ads, notifications and placements are on an on-going basis.

Margins look weak at a glance, coming in at 35% last quarter. But those margins take into account the carrier revenue share. While I don’t know what the revenue share is, it wouldn’t surprise me if its around 50%. That would make true margins for the business closer to 80%.

Revenue would be less of course. But if you looked at Digital Turbine and saw an 80% gross margin business with what is essentially recurring revenue, relationships with 30 major carriers, most of the major app developers, and that is on over 200 million smart phones growing at 30% per year, what would you pay?

The company might be a play on 5G as well. They’ve targeted their platform at phones, but there is nothing stopping them from expanding to other connected devices. TV’s for instance. In fact the business model here has some similarities to Roku.

I found the stock on a screen after it popped on its earnings beat earlier this week. It’s moved some since then and has a market capitalization of $200 million. Revenues last quarter were $30 million. With analysts expecting 20% growth next year that’s a P/S multiple of under 1.5x. They generated $4 million of EBITDA and $2 million of free cash last quarter. It doesn’t seem that expensive for what you get.

Some of the risks would be:

A. Could Google do the same thing? Maybe, but they haven’t. They would be cannibalizing their own app store and sharing revenue with carriers when they don’t now, so I don’t know if it would make sense for them. It’s a pretty small business in the overall scheme of things. Nevertheless its a risk.

B. Could Google block the platform on Android? It’s hard to believe that this wouldn’t violate competition laws but maybe it’s a risk?

C. Would carriers develop their own product? Again, maybe, and in fact based on the filings I’ve read I believe this has been the primary competition for Ignite (though there may be others I haven’t found any other than those mentioned in the 10-K: IronSource, Wild Tangent, and Sweet Labs). But carriers are getting a pretty good deal here. They basically do nothing, share in ad revenues, install revenues, app developer relationships that Digital Turbine cultivated. No R&D, marketing spend on their part.

D. Smart phone replacement cycle slows. This is why international expansion is important and the OEM deals are key. Digital Turbine can’t rely on growth in the North American phone market.

E. International expansion doesn’t work. Right now 85% of revenue is the the United States. They have been working on a ramp with American Movil for over a year now and its still fits and starts.

F. Carriers squeeze margins more. They just signed deals with Verizon and AT&T so this shouldn’t be an issue in the short-term. It will probably be important to show they can drive revenue growth for the carriers, which of course is good for Digital Turbine as well.

G. The fourth quarter (year end March) guidance did not indicate acceleration – 27% year over year growth at the mid-point and a sequential, seasonal decline greater than last year. With all the levers: ramping Single Tap, Smart Folders growth, Samsung relationship, I might have thought this would be higher. I’m not sure if I should read into it much though.

H. I feel like their R&D spend is low, which makes me wonder about how robust their business is against competition

I. Oath, which is Verizon’s media group (ie. advertising), represents almost 25% of sales so it is a very large piece of the revenue and represents concentration risk. Overall AT&T and Verizon represent around 80% of revenue.

As always, I’m starting my position small, will add if it appears to be working and will sell quickly if I look like I am wrong.

Lane – what do you think the upside is on this? Why would this trade at such a discount to roku?

It reminds one a bit of DoubleClick. I believe Google bought them out for 11x revenues

I’m hoping the upside is quite high but wondering if I’ve missed something that causes it to remain cheap. It seems to me that a platform like this, on this many devices, should be worth quite a bit. Maybe the mitigating factor is that at the end of the day the carrier has final decision on content, so these guys dont have free reign to put ads or placements or installs with whoever. And there is limited space on a phone so you can’t put too much onto it. Also, maybe investors are just worried that google could usurp the business if they decided to, which i can kinda see but also it wouldn’t be in google’s interests to cannibalize their own app store. Its also possible that its still a pretty new story – I think AT&T only started ramping a little over a year ago, the Samsung deal was only a few months ago, the post-install products only appeared in last year as well.

My guess is it underperformed for a while so people are still skeptical. Otherwise it should be a good deal higher.

Thanks for the write-up. Very interesting.

I have looked at this stock before, thought that GOOGL could easy compete with them if they wanted to and neglected it. But they seem to have penetrated quite a lot of devices last quarters. Their penetration percentage right now makes it particularly interesting.

One big problem I see with the stock is the unprofitability. Although operating expenses seems to make sense, cost of revenue is eating up all their profits. In 2016 the cost of revenue portion was 93% of the revenue. Since then, their revenue have more than tripled, and their portion of cost of revenue for FY18 is 66%. So I went on reading their fillings.

First, in their last annual report at page 9 they comment their profitability:

“We expect to continue to increase expenses as we implement initiatives designed to continue to grow our business, including, among other things, the development and marketing of new products and services, further international and domestic expansion, expansion of our infrastructure, development of systems and processes, acquisition of content, and general and administrative expenses associated with being a public company. If our revenues do not increase to offset these expected increases in operating expenses, we will continue to incur losses and we will not become profitable. Our revenue growth in past periods should not be considered indicative of our future performance. In fact, in future periods, our revenues could decline as they have in past years. Accordingly, we may not be able to achieve profitability in the future.”

I also looked after their cost of revenue. The big part lies in “license fees and revenue share”. On page 27 you can read:

“The business model that the Company is pursuing, mobile advertising and application installations, is in the early stages and not completely proven. There are many different types of models including, but not limited to, set-up fees, CPI, CPP, CPA, up-front fees (including licensing), revenue shares, per device license fees, as well as hybrids of each. Initial feedback from customers shows preference for different types of models. This could lead to risk in predicting future revenues and profits by individual customers. In particular, the ‘free’ download market is reliant upon mobile advertising, and the mobile advertising market is still in a nascent phase of monetization.”

So the licenses are not a fixed cost, but looks to be variable cost on their revenue they have to pay to the carriers. In this case, these costs are going to continue to cut off a big percentage of their revenue.

I found one last weak point on page 34:

“Third parties may sue us for intellectual property infringement or initiate proceedings to invalidate our intellectual property, either of which, if successful, could disrupt the conduct of our business, cause us to pay significant damage awards or require us to pay licensing fees. In the event of a successful claim against us, we might be enjoined from using our licensed intellectual property, we might incur significant licensing fees and we might be forced to develop alternative technologies. Our failure or inability to develop noninfringing technology or software or to license the infringed or similar technology or software on a timely basis could force us to withdraw products and services from the market or prevent us from introducing new products and services. In addition, even if we are able to license the infringed or similar technology or software, license fees could be substantial and the terms of these licenses could be burdensome, which might adversely affect our operating results. We might also incur substantial expenses in defending against third-party infringement claims, regardless of their merit. Successful infringement or licensing claims against us might result in substantial monetary liabilities and might materially disrupt the conduct of our business.”

From a revenue standpoint, this stock looks cheap. But how much do they need to raise their revenue in order to have a stable and significant profit? Will they even become profitable? This is something even the company itself questions. With their own concern, I am even more concerned….

Thanks for the write-up. Very interesting.

I have looked at this stock before, thought that GOOGL could easy compete with them if they wanted to and neglected it. But they seem to have penetrated quite a lot of devices last quarters. Their penetration percentage right now makes it particularly interesting.

One big problem I see with the stock is the unprofitability. Although operating expenses seems to make sense, cost of revenue is eating up all their profits. In 2016 the cost of revenue portion was 93% of the revenue. Since then, their revenue have more than tripled, and their portion of cost of revenue for FY18 is 66%. So I went on reading their fillings.

First, in their last annual report at page 9 they comment their profitability:

“We expect to continue to increase expenses as we implement initiatives designed to continue to grow our business, including, among other things, the development and marketing of new products and services, further international and domestic expansion, expansion of our infrastructure, development of systems and processes, acquisition of content, and general and administrative expenses associated with being a public company. If our revenues do not increase to offset these expected increases in operating expenses, we will continue to incur losses and we will not become profitable. Our revenue growth in past periods should not be considered indicative of our future performance. In fact, in future periods, our revenues could decline as they have in past years. Accordingly, we may not be able to achieve profitability in the future.”

I also looked after their cost of revenue. The big part lies in “license fees and revenue share”. On page 27 you can read:

“The business model that the Company is pursuing, mobile advertising and application installations, is in the early stages and not completely proven. There are many different types of models including, but not limited to, set-up fees, CPI, CPP, CPA, up-front fees (including licensing), revenue shares, per device license fees, as well as hybrids of each. Initial feedback from customers shows preference for different types of models. This could lead to risk in predicting future revenues and profits by individual customers. In particular, the ‘free’ download market is reliant upon mobile advertising, and the mobile advertising market is still in a nascent phase of monetization.”

So the licenses are not a fixed cost, but looks to be variable cost on their revenue they have to pay to the carriers. In this case, these costs are going to continue to cut off a big percentage of their revenue.

I found one last weak point on page 34:

“Third parties may sue us for intellectual property infringement or initiate proceedings to invalidate our intellectual property, either of which, if successful, could disrupt the conduct of our business, cause us to pay significant damage awards or require us to pay licensing fees. In the event of a successful claim against us, we might be enjoined from using our licensed intellectual property, we might incur significant licensing fees and we might be forced to develop alternative technologies. Our failure or inability to develop noninfringing technology or software or to license the infringed or similar technology or software on a timely basis could force us to withdraw products and services from the market or prevent us from introducing new products and services. In addition, even if we are able to license the infringed or similar technology or software, license fees could be substantial and the terms of these licenses could be burdensome, which might adversely affect our operating results. We might also incur substantial expenses in defending against third-party infringement claims, regardless of their merit. Successful infringement or licensing claims against us might result in substantial monetary liabilities and might materially disrupt the conduct of our business.”

From a revenue standpoint, this stock looks cheap. But how much do they need to raise their revenue in order to have a stable and significant profit? Will they even become profitable? This is something even the company itself questions. With their own concern, I am even more concerned….

Thanks for the comment. Sorry it was slow to be posted, it was marked as spam by wordpress for some reason. I tried to address the COGS in my post. They revenue share with carriers so yeah its true, they aren’t going to be an 80% gross margin company ever. They will also be revenue sharing with OEMs like Samsung so that’s the same deal. I don’t really see this as a negative though. Its just the business model.

On your second point, isn’t that pretty standard IP risk factor language?

On profitability, have you seen their EBITDA ramp? Its a hockey stick. If that continues profitability should be forthcoming.