Week 401: Treading Along

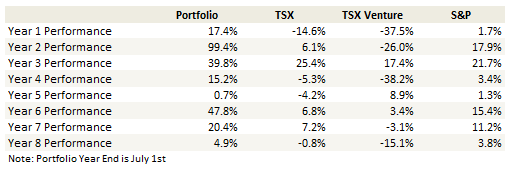

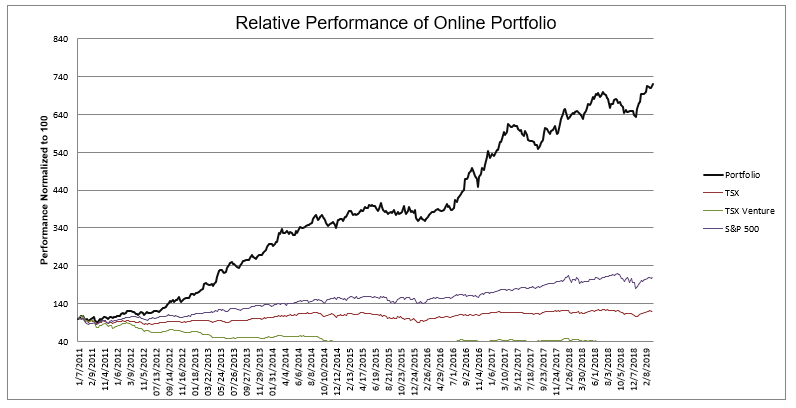

Portfolio Performance

Thoughts and Review

Treading water might be the best way to describe my portfolio performance. I haven’t participated much in the rally we’ve had over the past 7 weeks. My stocks got the initial bump in early January but since then its been only a little bit up.

In fact the tracking portfolio looks better than my actual portfolio because I don’t hedge the Canadian dollar here. That has helped the numbers by about 2-3% since my last update.

But what are you going to do? I said last update that I didn’t feel comfortable buying heavily into the rally and therefore I wouldn’t be chasing it. And I haven’t. The lack of performance is a consequence.

Nevertheless I am happy with the stocks I own. I think there are some that could turn out to be decent winners. Digital Turbine looks good. No one cares about Mynd Analytics but there is every indication that the merger with Emmaus is going to happen. Smith-Micro, Mission Ready and Evolus, all of which I will discuss below, give me plenty to be excited about.

Smith Micro

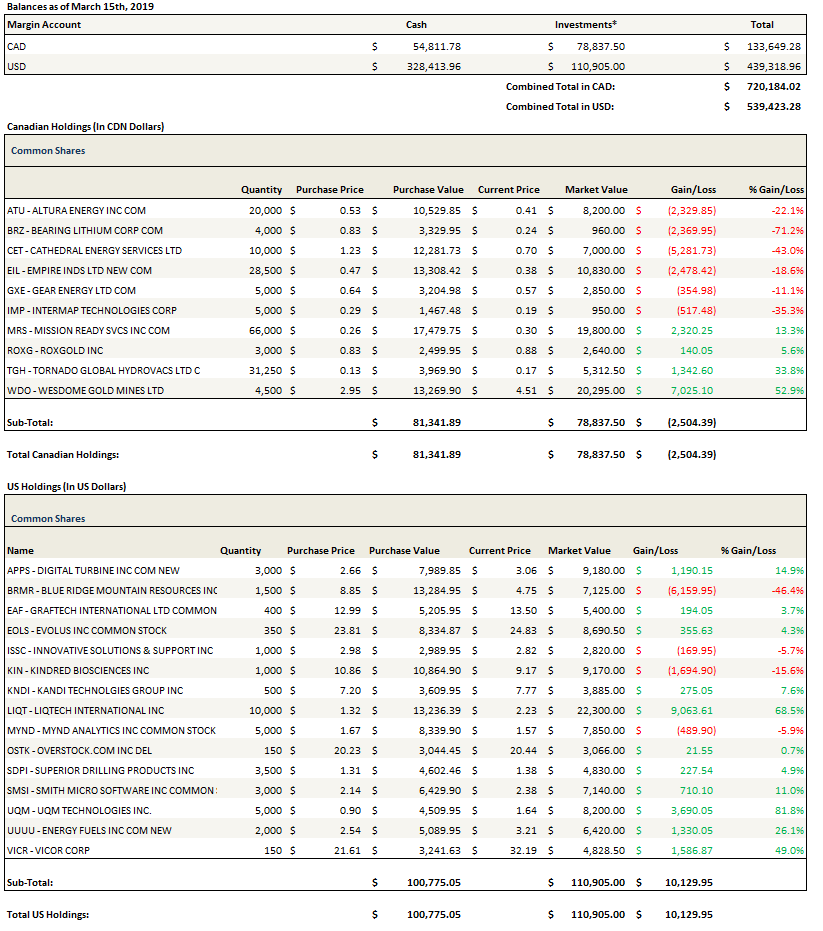

Smith-Micro had a great quarter. I added to the stock at $2.30 last week and added again Monday (which won’t show up in the portfolio totals below) as I think it could really turn out well if things continue in this direction. BTW, a thanks to Mark Gomes for his video on Smith-Micro, which helped give me some insight on the quarter.

I am told that the subscriber count, which is expected to see a doubling of between the third quarter and the end of the first quarter, was not a surprise, but to me it was, and I saw this as very positive news. Those subs should ramp to over $2 million in quarterly revenue over the next few quarters. That’s a pretty big jump from the $1.2 million of SafePath revenue that we had in the fourth quarter (which itself was up from $1 million sequentially).

Speaking in maximum double negatives, there seemed like there was not much not to like here. The fourth quarter revenue was really good ($7.4 million which was up from $6.5 million the previous quarter). They had positive earnings (3c EPS) and positive cash flow. Smith-Micro forecast another tier-1 win for SafePath in the first half and suggested they could have more than one new tier-1 by year end.

And the valuation is still not expensive at all.

The average estimate here pegs growth in 2019 at 30%. While that number could be higher or lower depending on how the Sprint ramp continues and the other Tier-1’s materialize, let’s take it at face value for now. I believe there is about 34 million shares outstanding including the warrants that are in the money again. So the market capitalization is $85 million. I realize there is cash with the warrants and on the balance sheet but I’m going to ignore that. At an $85 million market capitalization Smith-Micro trades at 2.5x forward revenue. If I didn’t tell you this was Smith-Micro and I just said I had a 30% grower with 80%+ gross margins and recurring revenue at 2.5x sales… I think you’d have to say that sounds like a deal.

Now I realize its never quite that simple and you can go down the road of why Sprint still hasn’t sunset the legacy software, why they didn’t Smith get a Tier-1 by year end like they had suggested they might, why are reviews still mixed on GooglePlay. There are always questions. But after these results and with the color they gave on the call I felt comfortable adding.

Mission Ready Solutions

One of the more interesting positions in my portfolio right now is Mission Ready Solutions. It is a stock I’ve held for a year and a half. For most of that time I have been flat to underwater on it. The original thesis I invested on is busted – there was an LOI with a distributor for purchases of their BCS armor vest (called Flex9Armor) from a foreign military. It never amounted to anything and the LOI was eventually dissolved at year end.

When orders from the LOI didn’t materialize many investors lost interest and were rightfully ticked off.

I stuck with the stock because… well, I don’t know exactly why. Probably some hope mixed in there. Also their lead product, the Flex9Armor vest, always appeared to be a legitimate product to me, maybe the best ballistic combat shirt out there. Same for the team at their subsidiary, Protect the Force, which on all indications is a premier R&D firm for tactical gear and body armor. I kinda took the opinion (and this is purely my opinion) that Mission Ready was likely given the run around by the distributor on the foreign military LOI. Also, the price of the shares remained surprisingly resilient through the first half of last year, a period of basically zero news and few positives to speak of, which made me wonder why that might be the case.

It turned out that Mission Ready was about to sign a merger deal with Unifire.

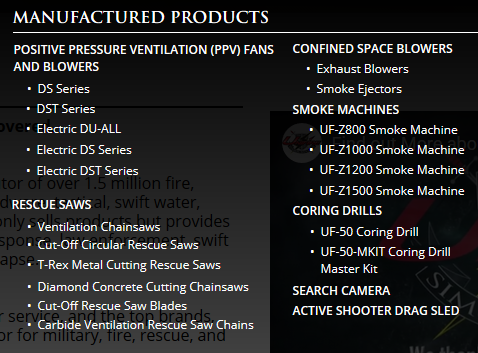

Unifire is a manufacturer and distributor of fire, military, emergency, and law enforcement equipment. The following are their own manufactured products, but in addition they distribute over 1.5 million products from a whole pile of different vendors.

In the first half of 2018 Unifire had $18 million USD of revenue (that number comes from Mission Ready’s original press release on the acquisition). We don’t have a lot of information yet on revenues prior to that. Government data shows that Unifire had $31 million of revenue via Federal Government contracts in 2017.

The interesting part, and I wrote about this before in this blog post back in September but will give an update here, is that Unifire is one of six participating vendors in Defense Logistics Agency contracts (DLA).

The most recent awards for two DLA contracts came out in February. Unifire is still one of six vendors for the “$4,000,000,000 bridge contract under solicitation SPM8EJ-13-R-0001 for special operations equipment” and one of six vendors for “$90,000,000 bridge contract under solicitation SPM8EH-12-R-0009 for fire and emergency services equipment”.

These are big numbers but before we get carried away there are lots of unknowns here. The biggest one is what piece of the pie Unifire will get. Historically it’s been small. Like I said, in 2017 Unifire received $31 million of government revenue. In 2018 that appears to be down to more like $6 million (which may or may not be because they have been tied up with this merger with Mission Ready over that period).

The story behind the merger is that Unifire has been capital constrained and that has prevented them from bidding on higher volumes. A $20 million available credit line was announced by Mission Ready a few weeks ago and with it in hand Unifire/Mission Ready should be able to bid on (and presumably win) more product. It makes sense, but we’ll just have to see how it plays out.

At any rate I don’t think it is any coincidence that Mission Ready announced a private placement after these DLA awards were announced. Literally the next day a $2 million private placement was announced. Likely a lot of investors had been hesitant to participate in anything until they knew for sure that Unifire was still on the DLA go-to list.

Today they announced that the PP was over-subscribed and would be increased to $3 million. A good sign as it means they at least have the original $2 million. It’s certainly better than the alternative.

A successful private placement is good news because it will mean we can finally get closure on the merger. After being halted for 7 months (maybe it was more? I lost track…), in February Mission Ready announced they had an escrowed close on the merger that still required approval by the TSX Venture to close (this is the first time I’ve ever heard of an exchange escrowed merger close?). So the merger has so far been a kind-of-mostly-done-deal. Once the money from the private placement is in hand I suspect it will become a fully done deal.

I added to my position in Mission Ready. While there is still a lot I don’t know, I do like the direction the story is going. Finally.

Overstock

Overstock announced fourth quarter results on Monday morning.

While the results missed estimates, disappointed many, and so on, I have to say I actually thought the retail business was in better shape than I had expected. I mean the fourth quarter wasn’t ideal but that wasn’t really a surprise.

Apart from the fact that I firmly believe that I cannot take anything Patrick Byrne says at face value, the thing that has most kept me from getting behind Overstock again over the last 9 months or so has been this retail traffic problem.

Overstock has had a problem for about two years. Their search engine optimization (SEO) traffic had been collapsing. I’m no online retail guru but even I can figure out that if your free traffic is declining precipitously you are probably in big trouble.

I’m pretty sure Byrne knew they were in big trouble too. In fact I would hazard to guess that the crazy marketing spending spree that Overstock did in Q1/Q2 of last year was a smoke screen to cover for the disaster that was SEO.

Byrne saw that the numbers were going to continue to get worse so he ramped marketing spend to cover for it. This created a false bump in revenue and allowed him to play the market with his growth schtick. You can even get hints of what they were really up to on the third quarter conference call, where they admit that they spent a lot of that money on testing and R&D. I have my doubts that the spend had much to do with competing against Wayfair. I think it was about ploughing money into a collapsing retail business in a last ditch attempt to right the ship.

Like many of the things Byrne does, while you can’t take it at face value you can have some confidence there is some legitimate plan behind it. Just probably not the one stated. And this time it appears to have worked.

The fact they are off that train and on the conference call said they would bring ad spend back down implies to me that they have some confidence that they will right the ship. I would be willing to bet that if Byrne didn’t think they could do it he’d come up with some new sleight of hand to get the market to look elsewhere.

There are two pieces of good news here.

The first good news is they did turn around their contribution dollars. And they are saying they can keep that going. The first quarter number they gave is quite good. The fourth quarter number wasn’t terrible either.

The better news is that there is a definitive turn in SEO. It’s not exactly a hockey stick but at least the collapse appears to be in the past.

I have struggled to see why an acquirer would be willing to buy retail for anything other than a very low-ball offer while SEO was in free fall. Any acquirer would see the pre-Q4 numbers as part of their due diligence and realize the business is likely doomed. Even if they were interested in Overstock’s logistics and back-end platform, I doubt they’d be willing to pay much given the negotiating position Overstock would be in. But the numbers above suggest this is changing.

The final bit of news is that while the first quarter revenue comp looks ugly it is bogus IMO because the marketing spend deluge that was done Q1/Q2 of last year.

Putting this all together, my wild guess would be that they might actually be able to sell retail once they show a couple quarters of solid contribution number and get above that break-even EBITDA number.

Meanwhile on the blockchain front in August tZero opens up to retail investors. This seems like a big deal to me and I like the idea of holding the stock heading into that. Its a tiny position but will be interesting to watch.

Evolus

Not much to say here as the stock treads water in the mid-$20’s, I hold my position and wait. Evolus released their fourth quarter results Monday night. Everything is going fine with the upcoming launch.

The most positive news was that they alluded that they already have the head-to-head data with botox and that the results are thumbs up. That should be a big positive as they will release those results in conjunction with the launch.

The second most positive news was that they received $100 million of debt financing. This reduces the worry of dilution.

Nevertheless I’m not increasing the size of my position.

Its still going to be a few quarters before we really understand the uptake. They said that the second and third quarters will be full of trials and free samples as they try to gain traction and take share.

I also need to understand the competition better. There was a discussion on the call last night about a longer acting toxin that will hit the market in a few years:

Irina Rivkind Koffler, Mizuho Securities: how do you contemplate the market entry of a long-acting toxin sometime maybe towards the end of next year or middle of next year? Does that change the #2 positioning? And can you stay at #2 beyond 24 months?

This toxin, called RT002, is owned by Revance Therapeutics. They had a Phase 3 study completed and plan to submit a Biologics License Application in the first half of 2019. A longer acting toxin, if the results are comparable, will likely be tough competition. Just how tough? I don’t know.

So I’m not sure yet how I should expect this all to play out. I’ll keep my position small.

A few comments on stocks I sold

Gran Colombia – it remains cheap and after I sold they changed the offering from shares and warrants to debentures. Had it been debentures in the first place I’m not sure I would have sold. I might have though. The small, worrisome piece of the story that always had me a little on edge is that if you read through the technical report on Segovia the grades are expected to start to decline after 2019. Now the veins they are chasing have been around forever and have always been high grade so there is every possibility that they find more high grade gold and this is not a problem. Still, it was the other contributing factor to me selling.

Golden Star – I’d like to see some sign that Prestea is straightening out. It feels like its been a year and the results at Prestea are getting worse if anything. The stock price has held up really well since I sold and so I am left to wonder if maybe this is the quarter where that happens and I will be kicking myself in a couple of months.

HyreCar – I mentioned in my last post that I had bought and sold HyreCar. The buying was a great idea, the selling not so much. I don’t see any news to account for the rise. I’m guessing that this $2 move since I sold (ugh) is because of the Lyft IPO? You know I always underestimate things like that. I mentioned the Lyft and Uber IPO’s as potential catalysts in my notes on HyreCar, but I didn’t really give that much weight to them. Turns out its the overriding factor.

Superior Drilling – I sold a bit of this. Nothing is really wrong with the stock but nothing is particularly exciting either. If I had to give a single reason for reducing my position it would be that their OPEX spend in 2019 is going to be higher than I had thought, so the company will grow, but they won’t be delivering as much free cash as I had hope for.

Liqtech – I have continued to reduce my position in Liqtech, which may turn out to be a mistake. Why sell the stock? Well it was a pretty big position and it is also a binary one. There still are a lot of assumptions in any of the calcs I run. So its really just a matter of risk management.

Portfolio Composition

Click here for the last seven weeks of trades. Note that I found a problem with my spreadsheet in the last update. From December 12th 2018 until my January 2019 update I had double counted my Smith-Micro shares (6,000 instead of 3,000). Therefore the totals for my portfolio during that time were roughly $7,000 (~1%) too high. I corrected all my tables and charts in this update.

{kind=link}

Out of OSTK, out of EOLS, I don’t have much room for volatility these days.