Update on a Few Stocks

Here are some of the changes I made to my portfolio in the last two weeks.

Liqtech

I sold out of Liqtech after reviewing their fourth quarter results. I did so a couple of reasons.

First, their guidance for the first quarter was okay but not as strong as I would have hoped. The company said they expected $7 million of revenue in the first quarter. Assuming diesel particulate filters rebound back to historic levels, that implies 10-15 filters, depending on the price.

That’s not as many sales as I would have hoped for at this point. We’re less than a year away from IMO 2020. I would have liked to see twice that.

Second, the company decided to stop reporting its backlog. As a rule, companies don’t stop reporting items that have positive implications for the stock price. Which leads me to wonder if and why the backlog is not be increasing as quickly as hoped?

One of my worries with Liqtech has always been that shippers go with “hybrid-ready” scrubbers that are designed to use a filter some day, but not right now. I follow the announcements on Ship & Bunker and other sites and I’ve noticed most of the large scrubber orders are described as hybrid-ready.

Gregory Vousvonis made interesting comments on SeekingAlpha yesterday saying:

Although closed loop and hybrid scrubbers make sense there is a legit counter-case to be made that the overwhelming economic benefit can be collected with a cheaper open-loop model and thus avoiding the more expensive and complicated closed loop / hybrid scrubbers. Which also have the disadvantage of having to dispose the solid residue from the wastewater management system.

Liqtech is still going to get a lot of filter orders, but the pace of these order may be more stretched out than I had hoped. And order may lag until there is a more general ban on open-loop scrubbers everywhere

This is all just guessing. Maybe the company has completely unrelated reasons for not reporting backlog. The stock price has actually held up quite well since the earnings release which makes me wonder if I am wrong. Nevertheless I decided to do my guessing from the sidelines.

Product Tanker Stocks

In his comment on SeekingAlpha Vousvonis says he was researching Scorpio Tankers when he came upon the insights about open-loop scrubbers. It’s a coincidence because I have been researching tankers myself.

I’ve known for a while that product tankers (the one’s carrying gasoline, diesel and other clean fuels) are expecting an uptick in demand from IMO 2020. Gasoil and low-sulfur bunker fuels will need to be transported to the bunkering hubs. As well longer shipping routes will be required as low sulphur fuels now need to travel further (refineries that are most able to produce low sulphur fuel are in North America and Europe whereas the demand will increase in ports across the world in particular in developing nations).

With that in mind I found this panel discussion with four product tanker companies, which was tweeted by @20slots, to be really interesting.

Each participant is very bullish. Of course it could be said that shipping companies are always bullish. But I don’t know – not like this.

The most interesting argument made is that product tankers have been in a bear market for 11 years. The companies cannot respond to the coming demand from IMO 2020 because they are too levered already and their share prices are too depressed. This sets up a scenario of an extended cycle.

I took equal positions in 2 of the panelists: Ardmore Shipping and Scorpio Tankers. I took a smaller position in Pyxis Tankers. Of the 3 I am inclined to think Scorpio might fair the best. Why? Because they have been the most proactive with scrubbers.

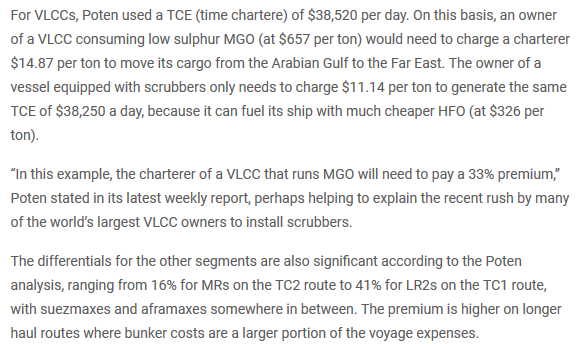

Scrubbers could potentially be quite lucrative to the shippers that install them. An old article from last year:

The estimates in the article are for VLCCs so the absolute margin increases will be lower for MR and LR tankers, but you get the idea.

Speaking of selling scrubbers to Scorpio, @FBuschek found an obscure little company to play scrubber installations with. Pacific Green Technologies has scrubbers orders with Scorpio Tankers, Scorpio Bulkers and a couple of other tanker firms.

Pacific Green is an illiquid little OTC company, so I took a very, very small position in it. Really its more just for curiosity than anything else. They have a partnership with a Chinese company called Power China, which makes me a little wary. They also split gross margins with Power China 50/50, and with no guidance from the company on what margins might be, its difficult to put together any kind of financial model

Nevertheless scrubber orders of nearly $200 million on a stock with a $135 million market cap makes this an interesting one to watch.

Oil stocks – Athabasca Oil and Gas and Crescent Point

I made a couple bets on oil stocks. The price of oil has risen and the stocks so far have not followed. This happened last year. At the time it was frustrating to watch until it wasn’t. In April of last year oil stocks decided to join the rally and some of them rose 75-100% in the matter of a month.

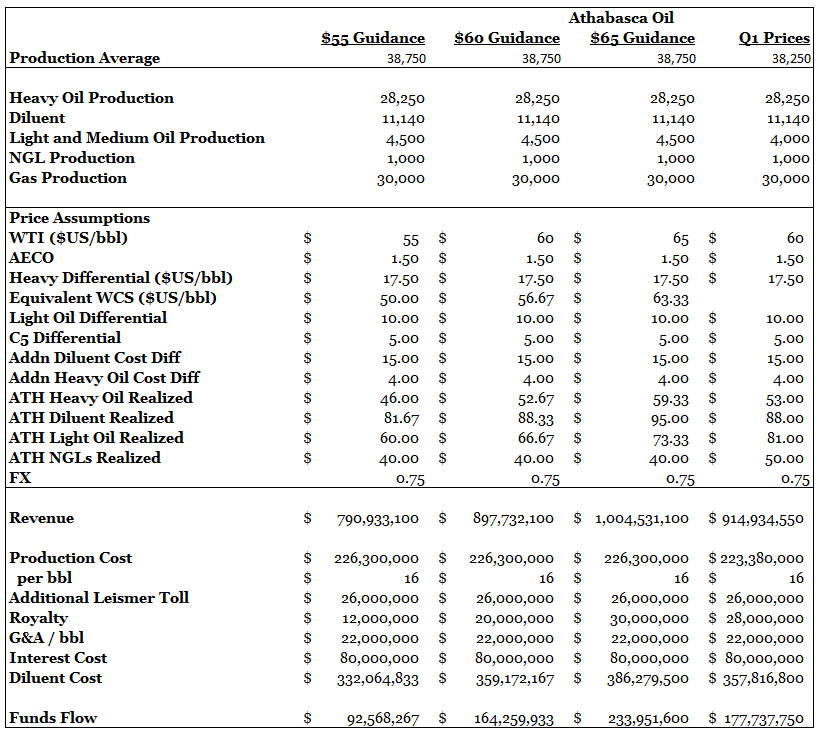

Will that happen again? Who knows. But its worth a small gamble I think. I added Athabasca Oil and Gas and Crescent Point. I did a rough model on Athabasca, essentially replicating the company’s own guidance, and it’s quite stark how levered the company is to each $1 increase in the price of WCS at these price levels.

Athabasca is guiding to CAPEX of between $95 million and $110 million for 2019. So you can see how the free cash flow begins to add up. WCS prices were USD$56/bbl yesterday. Athabasca has a market capitalization a little under $500 million.

HyreCar

I owned HyreCar earlier this year and briefly mentioned it in one of my portfolio updates. I didn’t talk about it extensively because I didn’t know how long I would hold onto the stock. I was worried about their ability to add dealer inventory to their rental car platform. As it turns out I sold it after a month but missed much of the run-up to $7.

Well the company reported their fourth quarter earnings and the stock responded poorly. To be fair I think the stock moved more on the Lyft IPO than anything to do with its own results. The same could be said for the prior move to almost $8 per share.

I thought HyreCar’s results were actually pretty decent. As it turns out Hycar was pretty successful adding dealers to the network.

In our third quarter call, we noted that we had 25 dealerships representing an estimated 250 cars on our platform. A number we expected to double in the fourth quarter of 2018. Today I am proud to report, we listed our 100th auto dealership today, of which, 1200 cars have been listed to the platform.

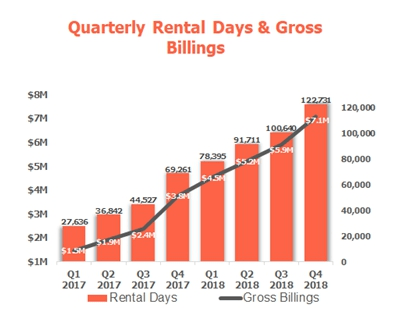

HyreCar had 10% growth sequentially in the quarter which is pretty good. But I think the headline number may underestimate the underlying growth.

If you look at the 10-K there is a table showing gross billings and rental days. Both increased around 20% sequentially in the fourth quarter.

But HyreCar didn’t fully participate in the growth of gross billings and rental days because owners took a higher percentage of profits in the quarter (the tables are in weekly and daily respectively so you have to convert one of the two to see the apples to apples comparison).

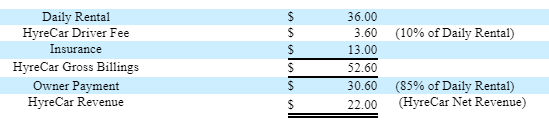

Third quarter margins per vehicle:

Fourth Quarter margins per vehicle:

I’m not surprised that owner margins went up because HyreCar had to entice dealers to deliver cars to the network. The success of that initiative is more important to the long-term viability of the business than the lost margin in the short term.

My hope would be that margins stabilize and HyreCar more-fully participates in margin growth going forward.

Also in the 10-K is a note that HyreCar should be realizing better margins on insurance in the second quarter:

American Business Insurance Services (“ABI”) is our insurance broker and Y Risk is our mobility-focused managing general underwriter. Y Risk was sold by our incumbent insurance company American International Group (NYSE: AIG) to The Hartford (NYSE: HIG) in December 2018, and we are in the process of moving our annual car insurance policy with The Hartford for the plan year from April 2019 to March 2020 under superior pricing and term

Together these positive data points made it worthwhile for me to add back the stock.

Aehr Test Systems

I’ve been watching Aehr flounder the last few quarters after selling it last year. But it looks like they may be turning the business around here. It was a pretty positive conference call, and I haven’t known the management team to be all that bullish unless there is reason to be.

On the call management made the following points:

- Evidence of a ramp in orders – $6.9 million backlog at the end of fiscal third quarter plus recently announced orders means they have a $10 million plus backlog

- Currently actively engaged with 12 customers

- Expect to see a significant increase in bookings in the fiscal fourth quarter

- Expect a return to profitability in the fiscal fourth quarter

If I understood what they were saying on the call, it sounds like the low-end products they’ve introduced have been successful in bringing on new engagements and initial orders. As well maybe, just maybe, the technology of smaller dies is finally beginning to require a solution like the FOX family of systems as CEO Gayn Erickson said “our solutions stand alone as the only way to cost effectively scale to meet the demands of these devices that are used in 5G infrastructure build out, 2D and 3D sensors, and enterprise and datacenter server and storage applications.”

So we’ll see. I took a starter. I mean my biggest worry here is that the semi-conductor industry is strong enough to support the growth, but I guess I’ve been totally wrong about my assessment of the economy in general (or at least that is what the market has told me!) so I’ll try to keep that concern locked away in the back of my head for the time being.

You and OGIB both had Liqtech. He bailed 2 weeks ago. Squeaked out a profit.

How is Atlantic Power coming along.

Yeah I know a few people that have bailed since earnings. It just seems so much more up in the air now.

I don’t think I’ve ever owned Atlantic Power? You mean Atlantic Gold maybe? If so I sold that one but I keep waffling on these gold stocks, thinking this has to be the right environment for them doesn’t it? What with Herman Cain now, have to wonder what the Fed policy is going to be like in a few years if Trump gets elected again.

FYI, Frontline (FRO) bought a scrubber company in anticipation of IMO2020.

I bought back into HYRE as well, tiny position. Nice catch on the share being paid back to the car dealers / owners.

How come you turned around again on GCM if I may ask? Why do you reckon the stock is lagging again?

Also long ATU and GXE personally. Very few micro and small caps that are managed well. My picks are unlikely to be picked up by funds as long as the don’t double a few times but there might be value in that. I definitely see the possibility of buybacks for Gear once their debt is lowered to $50-$60 M range if their stock price remains depressed. Returns on buybacks would be insane, especially given lack of many growth opportunities due to apportionements.

Cheers

Well my thought was that with Trump bringing on guys like Moore and Cain to the Fed and with the Fed already leaning dovishly, that the gold rally would continue. But that hasn’t turned out to be the case!

Hi Lane, I also have Crescent CPG and after painful end of 2018 now am up on it quite a bit as avg down. The reason like it is It was $40 in 2014 with only twice the EBITDA it has now and the share count has only gone up a small amount. Thus indicates it could go back to $20. And with WCS going up maybe it can match 2014 EBITDA and go to $40.

My 2 cents on bearish oil stocks: OPEC meeting in June, prices are high enough and Saudi previous target was $70+ to balance their books, thus they may have incentives now to release more barrels and compete with the US for market share. 2nd factor can be the high S&P/ global stock indics now.