Another Nuvectra Update

Nuvectra is not even close to being my largest position. It is however BY FAR my largest loss right now.

Be that as it may. The past is the past. Another less dubious distinction that Nuvectra holds is that right now it is the most interesting position I have. This is why I am devoting more space on this blog to it today.

The situation with Nuvectra is fascinating to me. It is the starkness of the outcomes. I am pretty sure the two most likely end game scenarios are A. lose it all or B. make a lot.

Nuvectra started trading on the over-the-counter market today. The stock has a “Q” on the end and is no longer part of the Nasdaq. It likely won’t be changed on your brokerage account for a day or two.

One of the things I researched in the last week is how bankruptcy stocks trade. What I have learned is that they fluctuate wildly.

Nuvectra could go down to 5c and it means nothing. It could go up to 50c and mean nothing. In fact, today Nuvectra briefly touched 8c first thing in the morning. It closed over 20c.

Bankruptcy stocks trade with insane volatility. You basically have to place your bet, accept the possibility of a 100% loss, and stop looking at it.

With that said, let’s move on to the news and recap what has happened since I last wrote.

A Barrage of Filings

The company has submitted a slew of bankruptcy filings. Most of them are pretty boring and the legalese is painful to read. But there are some details that have been disclosed that give us an idea of where we stand.

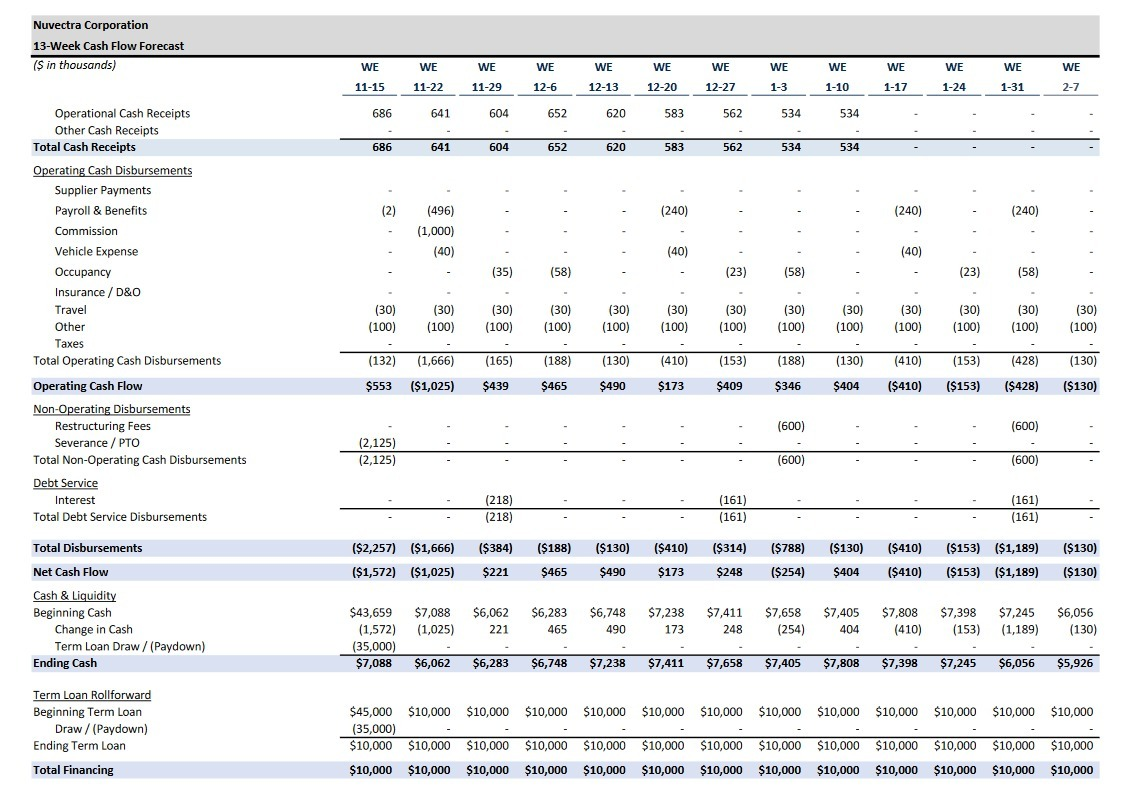

First of all, Nuvectra had to provide a cash forecast as part of the cash collateral requirements. That plan shows the company’s cash and liquidity through the bankruptcy process.

What we see is that Nuvectra has paid off the majority of the term loan that was outstanding. $35 million was paid down. There is $10 million of the term loan left, against about $7 million of cash as of last week. The year-end number for cash (I’ll explain why the year end date appears is important shortly) is about $7.6 million.

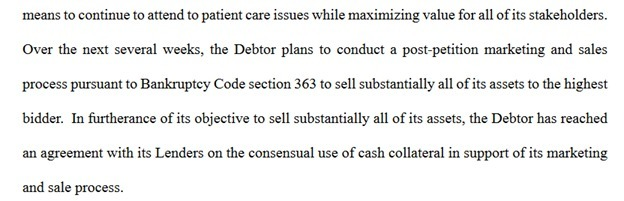

Next, Nuvectra clarified their intent. In a Chapter 11 bankruptcy you can either have your debts cleaned up and continue operating as a business or you can try to sell everything and dissolve the company. Nuvectra is doing the latter:

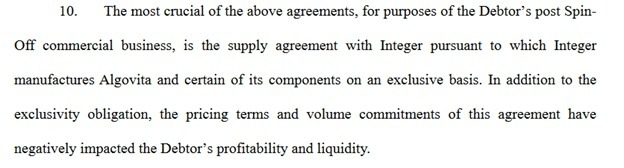

I mentioned in my last post that my suspicion was that this bankruptcy was precipitated by the existing manufacturing contract that they have with their former parent, Integer.

To re-cap the history, when Nuvectra was spun-off they were saddled with a 5-year deal whereby Integer would be the sole manufacturer of Nuvectra’s Algovita systems.

This contract was less than ideal for Nuvectra. Gross margins for Algovita have been around 50%. Yet I don’t see any reason they should be less than 70%. There is a case to be made that they should be even higher.

My guess has been that any buyer of Algovita balked at the manufacturing contract. The only way out of the manufacturing contract was via bankruptcy. So that is the direction Nuvectra went.

Nuvectra alluded to this in one of their bankruptcy filings.

One of the big questions marks for me has been whether Nuvectra is on the hook for the manufacturing contract now that they are in bankruptcy.

As part of the Integer contract there were minimum volumes specified that totaled a little over $20 million for the rest of 2019 and for 2020.

Some sleuthing from @fbuschek has been really helpful in this regard (big h/t for all the help). It appears that when you go through Chapter 11 such contracts, and minimum requirements, can be rejected by the debtor.

And from this source:

What is so significant about executory contracts in a bankruptcy proceeding is that the Bankruptcy Code authorizes a bankruptcy trustee, and in the case of a Chapter 11 proceeding the debtor-in-possession, to reject any executory contract or lease where it is in the best business judgment of the trustee or debtor-in-possession to do so. Provisions in executory contracts and leases that prohibit or restrict such rejections are unenforceable

If we are correct and the minimum volume contract is no longer applicable, the debts of Nuvectra consist only of the secured and unsecured creditors.

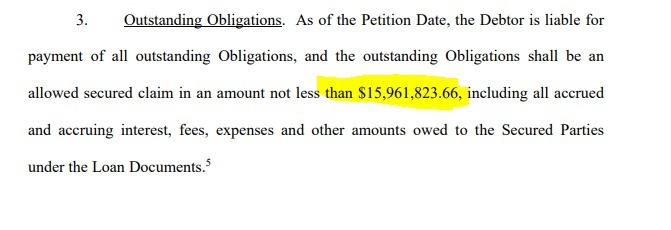

Let’s look at those creditors. We received information about both. First, the secured creditors. In a filing late this week we learned that secured claims were around $16 million.

The largest of these secured claims is the $10 million they still owe on the term loan.

The largest of these secured claims is the $10 million they still owe on the term loan.

The other $6 million? An earlier filing listed a number of claims that Nuvectra was petitioning to fulfill. This was stuff like salaries, commissions, insurance, warranties, etc. I’m a little uncertain about how I should be including the insurance and warranty amounts, so those might be off, but I am heartened that the numbers provided in the filing totalled around the amount of remaining secured debt that Nuvectra had outstanding after you remove the term loan.

After secured debt we come to unsecured debt, which was totaled for us in an earlier filing.

This filing actually shows the 20 largest unsecured creditors. After #20 the amounts are small enough that they can be ignored. In total it appears that there is a little over $5 million due to unsecured creditors.

Its worth pointing out that the two largest unsecured creditors are their suppliers: Greatbatch (now Integer) and Minnetronix.

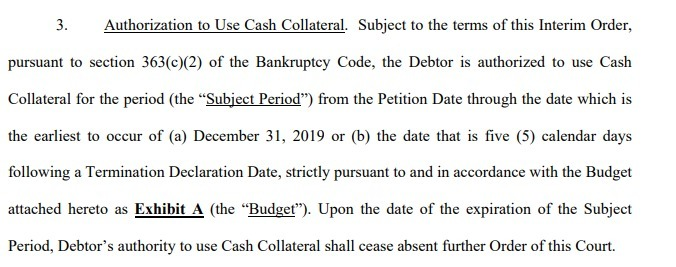

I mentioned earlier that I would explain the significance of year end. Here is an excerpt from another filing, released earlier this week, that stipulated details about the cash collateral agreement.

The key clause is that the cash collateral date goes until the earliest of a unspecified termination date or December 31 2019.

Here’s a question: why limit your cash collateral agreement to December 31st? Why not come up with some terms that take you out into next year, so you have a nice long runway and don’t have to go back and extend if need be?

It sounds to me like they expect to have this thing wrapped up quickly.

Another point that came out literally minutes before I wrote this. Nuvectra put out an 8-K announcing 89 employees are being let go. Nuvectra had about 200 employees in mid-June. They already had 25% layoffs in August. So this move takes the headcount down to ~50-60 people.

Adding it up: Where are we?

It looks like there are $21 million to $22 million in creditors to pay off. There is $7 million of cash. The company had inventory of $8 million at the end of the second quarter accounts receivable were $9.4 million.

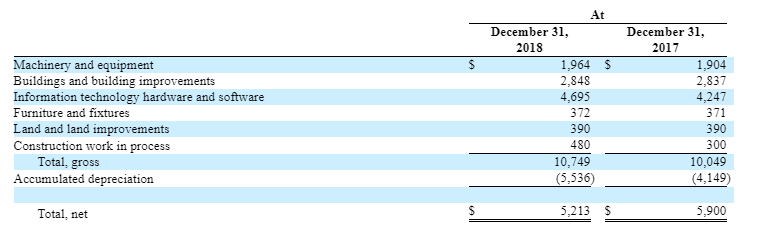

Property, plant and equipment, net of depreciation, was $5.2 million at year end 2018. Nuvectra owns their research and development facility in Blaine Minnesota. They lease their other facilities (interestingly, from Integer).

You can discount these amounts as much as you want. I am not going to try to figure out what the cash value is because I haven’t gone through near enough bankruptcies to know what these kind of assets can fetch and the information we have is largely circumstantial or analogies.

The bigger question, also fraught with uncertainty, is going to be this: what are Algovita and Virtis worth to a bidder in bankruptcy court?

Algovita has ramped to be a $50 million revenue product. Obviously, it is not a profitable product, but that is largely due to the dead-weight manufacturing agreement that lets Integer take way too much margin.

What is Algovita worth now that it is unencumbered by that manufacturing contract?

While Nuvectra is letting a lot of their people go (so you would essentially be buying the IP and maybe (???) retaining a few key lead personnel) it still strikes me that this IP should be worth quite a bit.

Once you buy Algovita, in particular if you are big company like Stryker, you can set up a cheap outsourced manufacturing agreement (maybe even negotiate a better one with Integer) and use your existing sales team to sell it. I would expect profitability to follow shortly.

There was a time, not long ago in fact (like 6 months prior), when brokerages were valuing Algovita as a $300 to $400 million product.

As for Virtis, I don’t have a lot of data to work with, and the product is still awaiting approval from the FDA (expected mid-next year). JMP described the opportunity with Virtis earlier this year:

We also continue to expect a decision from the FDA regarding the approval of Nuvectra’s VIRTIS SNS (sacral nerve stimulation) product, an indication with only one competitor today on the market and an ~$750 mln TAM.

Virtis has had their approval delayed by the FDA multiple times with requests for more information. It’s been 3-years since Nuvectra filed with the FDA. Earlier this year Virtis was expected to be approved in the second half of this year but that now has been pushed out.

Meanwhile a competitor in the space has gotten approval. Axonics has a device targeting the sacral neuromodulation (SNM), the same as Virtis. The Axonics device was approved for fecal incontinence in September and urinary symptoms in November.

The Axonics device is the second to market. The incumbent is a Medtronics device called InterStim.

The big disadvantage of InterStim is that it has to be pulled out every 5 years or so, meaning you need to have multiple surgeries. Both the Virtis and Axonics devices use rechargeable batteries and so their life is 15 year plus.

Nuvectra gave this direct comparison of the devices earlier this year.

The following is a note from Wells Fargo. It describes the Axonics submission, clarifies the the “paper” pathway and identifies some of the device differences between it and Virtis. It seems the Axonics device has some advantages.

Average analyst estimates for Axonics next year are $80 million of revenue and negative $45 million of EBITDA.

The market is giving Axionics a “Nuvectra-like” market capitalization for top line growth and bottom line losses at $600 million.

The delays to FDA approval have obviously hurt Nuvectra a lot. The FDA could just be being cautious on approval given that Nuvectra chose to go the “paper” route – they did not do trials and instead relied on literature for their submission.

I get the sense that the Axonics device may have a few advantages, while Virtis has others (it has current steering which is basically like a dimmer switch, 2 leads with more channels and the leads are stretchable) but overall the devices seem quite similar. If Virtis is approved you would think it would have value.

It would not surprise me if, assuming this plays out positively, Nuvectra kept Virtis until there is FDA approval. I don’t know if that would happen in bankruptcy or outside of it. But it would seem to me that Virtis would have a lot of value once approved

What will shareholders get paid?

I am not going to try to do math on the above figures. Any set of numbers that I try to use could be easily shot down. What is PP&E worth? What is the end cash position? Most importantly, what will Algovita and Virtis sell for?

All I will say is this. I think there is a reasonable chance that the combination of value from these sources greatly exceeds debt and leaves shareholders with significant value.

Keep in mind, at 20 cents Nuvectra is worth $3.4 million net.

What are the chances that assets exceed liabilities by substantially more than that?

I would say it is non-zero. In fact, I think it is significantly higher than zero. So I have continued to add to my position.