Sticking with One’s Knitting – Portfolio Update

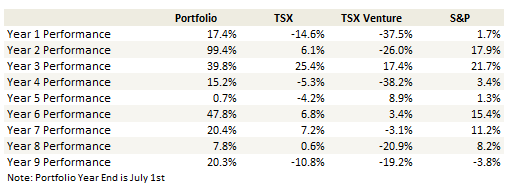

Portfolio Performance

Thoughts and Review

I have been intending to do this update for a while but with kids at home all day and us parents now taking on the role of full-time teachers in addition to everything else, well, its not an easy juggling act. This update takes me up to the end of last week.

My portfolio has continued to perform well since I last updated at the beginning of March. I am not lighting the world on fire with 20%+ gains off the lows (like the market itself is), but I also did not have a low that was less than the previous high (my last lows came as the market set its previous highs). So I am content with my modest performance and the lack of volatility that has come with it.

I did follow the market up last month to some degree, purchasing long positions in a few sectors that I felt presented opportunity. It truly is a bifurcated economy, and it has become clear to me that while the overall impact may be negative, there are a bunch of big winners here. While I am of the mind that some businesses are still best to be stayed-away from, others have the potential to do well because of what has changed or because the Fed has their back.

SaaS

On the first account (trying to find winners because of what has changed – ie. the stay-at-home and work-from-home economy) I missed out on the early work-from-home/stay-at-home ideas like Atlassian, Citrix or Zoom. But I try not to be stubborn. Last week I bought Overstock, which looks to be a likely beneficiary of stay-at-home trends (the April sales numbers were ridiculous!), and this week (so not included in the update below) I bought into the SaaS trend with Workday, Pagerduty and today (Thursday) Alteryx, all of which should be beneficiaries of work-from-home.

I have been hesitant to buy SaaS names in the past but I have changed my mind. I have been presented with two ideas (revelations?) that have made me willing to wade in a little.

First, there was a piece from Morgan Stanley last week that finally explained to me why these stocks can’t be valued on traditional metrics. And it made sense. A few arguments were made, but the most insightful to me was when they went through the math of just how much the operating margins are depressed by the growth. It was a bit of an ‘aha’ moment to see this.

Second, I just look at the likely outcome of this pandemic: if a company looks at their expenses at the end of this whole ordeal and says “you know what, this stay at home thing worked not too bad”, they are going to quickly realize that they can reduce their office space by some factor and scale up their licenses to SaaS by some other factor (to make sure those stay-at-home workers have the absolute best in connectivity) and in the aggregate I am sure the company will save many dollars.

That should make this shift durable over time. It means there are going to be winners and losers here and SaaS really does look like a winner.

The third point is something I’ve said before – these SaaS companies are mini-bets on rates. Their earnings are way out and therefore present value discounts matter. But rates are so low, and I find it hard to believe they will do anything but go lower, which is yet another tailwind for the sector.

But I’m still pretty chicken. My favorite name of those I’ve researched so far is Atlassian. I used to work as a product manager, so I know their software and I totally get how its going to be sticky and scalable and all that jazz. But man, I just can’t pay 20x sales (I think it might actually be 25x sales now) for a stock. I was looking at it last week and then it sold off briefly after earnings but I couldn’t bring myself to buy in. The 3 I’ve bought are not cheap (Workday and Pagerduty are 7x sales while Alteryx is 12x) but I think I’ll need some more time before I can comfortably go much further.

Mortgage Stocks

I have also done reasonably well in identifying a few winners of the Feds largesse.

Thinking of how one picks stocks in such a tumultuous time, I listened to one podcast early on in the crisis, I believe it was back in March, where the hedge fund manager being interviewed made a very salient point – that it was too late to do the work – you already knew what you knew and you should stick to that knitting because that is what you will have conviction in.

There is definitely some truth to that. When the world is collapsing, trying to buy a new name that you only just learned of is tough.

It is no surprise, therefore, that the names I bought early on in the crisis were largely the one’s that I have owned in the past – or at least which come from sectors I have owned in the past and have comfort in. My mortgage bets are a good example of this.

As a group the mortgage players have been my biggest bet. I started with the agency mREITs, which I wrote briefly about a few weeks ago. These guys were an obvious bet – I mean the Fed was basically buying their primary asset (MBS), the Fed was backstopping their funding (repo), and they had already taken it on the chin from the write down of everything on their book but the kitchen sink in March. I bought Annaly and Orchid.

As is usually the case, investors got very negative on these businesses after they had gone through the wringer. After Annaly, AGNC, Orchid and the like had taken massive hits to their book value, investors (on SeekingAlpha in particular) came out of the woodwork explaining how awful these businesses are and how they would never own them.

Now to be clear, those statements are not completely without merit – I mean a business that can collapse like these did is perhaps awful, and I would have not have owned any of these companies before the COVID collapse, but after virtually every negative event that you could imagine had been thrown at them and after they had fallen to levels that were significantly below what was a much reduced book value, well I was willing to re-evaluate their relative awful-ness at that point.

Much the same can be said (but with even more gusto) of my second foray into the mortgage industry – buying companies that own the MSRs (New Residential, Mr. Cooper and PennyMac Financial).

Here again, I know MSRs fairly well, I made a good deal of money investing in these companies back in 2011-2013 when very few investors knew what an MSR was, and so I have a level of comfort here, both with what makes an MSR good and bad. It is not a perfect asset. It has pitfalls. But it is also not a dumpster fire.

What happened to these stocks is much the same as the agency mREITs – after New Residential, Mr. Cooper and PennyMac Financial had already taken enormous hits to their book value, well, then investors piled on and said these companies are uninvestable.

Quite honestly, the post-mortem trashing of New Residential has become almost a tradition. I swear that every crisis the same thing happens. New Residential gets clobbered (always for basically the same reasons – because their business really is flawed under certain circumstances of extreme volatility), and from there the rants begin about how awful the company is and how it is going bankrupt. This occurs in concert with the Fed stepping in and backstopping what were the main flaws in their business.

But again, I do not necessarily disagree with the term “uninvestable” (though I’m not sure it is actually a word), but I do disagree with the tense – these companies were uninvestable – they are businesses that are very vulnerable to dislocations in the credit market and yet they were priced for a never-ending status quo in a world that was bound to throw a curve ball at some point.

But now? Now they trade at a fraction of their book value, that book value already been greatly reduced because the fatal flaws have been realized, and meanwhile the Fed has insured that there will be liquidity for all and asset price stability.

While it is easy to write off these companies as too hard or too levered or some sort of scheme (all of which are kinda true), I prefer to look at them positively. That is to say – these companies have a lot in common with a bank. They have assets that earn interest. They have liabilities that allow them to fund those asset purchases. The equity is a fraction of the overall balance sheet. So yes, they are very levered – just like any bank is.

The difference, of course, is that their funding sources are not deposits and their assets are not loans. Their funding is a combination of repo, securitizations and bank lines. Their assets are MSRs, mortgage loans, mortgage securities and other instruments that hedge against them.

So when I think about this I ask – is it better to own a bank? – One that has maybe 10% of assets in construction loans, another 10-20% in commercial real estate (that is full of tenants that have been closed the last month), maybe 20% in residential loans (some of which are in forbearance) and a bunch more in business loans (many of which are small businesses that may or may not survive)?

Or is it maybe even bit safer to own a company whose primary asset is an MSR – an asset that sits at the top of the chain in the case of default, that returns cash regularly, and where the government has limited your exposure (in the case of Fannie/Freddie to 4 months of servicing advances, in the case of Ginnie, they have put in place a facility to deal with advances entirely). And which, on the liability side yes, they do not have deposits, which are for sure the preferable funding alternative. But the issues around repo, securitization and bank loans were the risk before this happened. But now? With the Fed buying everything in site and doing whatever it takes to make sure these markets get back to normal? Is this really such a big risk?

Let me say this – if the repo market and securitization market re-freeze now, with the amount of intervention that the Fed is doing and indicated it will do if necessary, then we probably have a much bigger problem to worry about than whether the mortgage servicers will do well.

To punctuate the point – in my opinion, the biggest difference between the banks and the mortgage names at this point (and this goes for both the agency mREITS and the hybrids with MSR assets) is that the mortgage names all had to take their losses up front – they have had to mark their assets and they have had to deal with the margin calls – while the banks get to string it out much longer – extending terms on loans, using government backstops to cover losses, and most importantly, not marking their loan book too closely.

Because of that, banks trade at above book (for the big ones) or only slightly below book (for most of the small ones). Believe me I looked – I went through at least 50 community bank filings looking at how cheap they were and hoping for a bargain. But I was disappointed. This is not 2009 yet – these banks are not trading at a big discount and I am simply not willing to buy a bank for 90% of tangible book given where we are at.

But because the mortgage names have taken their losses upfront, they have been punished. At the time I bought them they traded at less than 50% of their reduced tangible book. This made (and still makes, to a lessor degree) them seem attractive to me. The bad news is out and a lot has been priced in. The Fed has their backs. Yes, these are flawed businesses. And no, I will not be owning New Residential when it trades back to double-digits and announces a 25c per quarter dividend. By then the world will be back on its feet and most likely all those risks that caused New Residential to collapse will be getting put back on the balance sheet. But at $5? Sure, I’ll take a swing at that.

Gold, Natural Gas and Everything Else

Well that discussion of the mortgage names I bought took up much more space than I intended so I will keep the rest of this update short. What else I have bought are a few more gold names – a basket of gold project developers – for as I wrote in my prior post, if this gold market does become a bull market (which is still an open question), these names will begin to outperform. I bought a basket – 4 names – because even though I’ve researched each I find it very hard to tell which will be the biggest winners. So it is simply a method of smoothing out my odds.

I also bought a number of Canadian natural gas producers. This is a very simple bet – if oil is being shut in, so will all the gas associated with that oil. For the first time in maybe 10 years, that means something positive has happened for the natural gas producers. I do not think it is a coincidence that the natural gas producer stocks have been very strong. Their charts echo the best of tech – Amazon, Zoom, or Atlassian. I added Advantage Oil & Gas, Peyto Exploration and Pine Cliff and they are doing particularly well today.

I also added a few individual names. Two I went back to the trough for: Radcom and Intelligent Systems – both names I have held in the past (and one’s I only realized Monday I forgotten to add to my tracking portfolio here so I have corrected that now but they aren’t reflected in the positions below) – as well as one brand new name, DLH Holdings, which is a staffing company but with a government bent and where I saw little risk of disruption to their business and a very cheap price.

Finally, I kept my index shorts and yes, they weigh down the performance on days like today, but they more than did their job when the market was in collapse, and I am not smart enough to know with any certainty whether we will go straight up to 5,000 or not, so I will keep them on. The only days I find these shorts supremely frustrating are days when the markets are up 5%+. On these days it is without fail that my longs under-perform the market – usually because 1 or 2 of them is down 5% for no reason at all (usually on less than 1,000 shares, just to really stick it to me).

But this happens every crisis – and I mean every crisis – it happened in 2016, it happened in 2018, and it happened now. While I freaked out about it in 2016 (this was the first time I had been through a collapse with a hedged portfolio) I’ve seen it enough now that I can take it in stride. If we are indeed recovering this will likely unfold like it has the other times – the indexes will settle down and the micro and nano-cap stocks I own will catch up. It is simply a lag.

Portfolio Composition

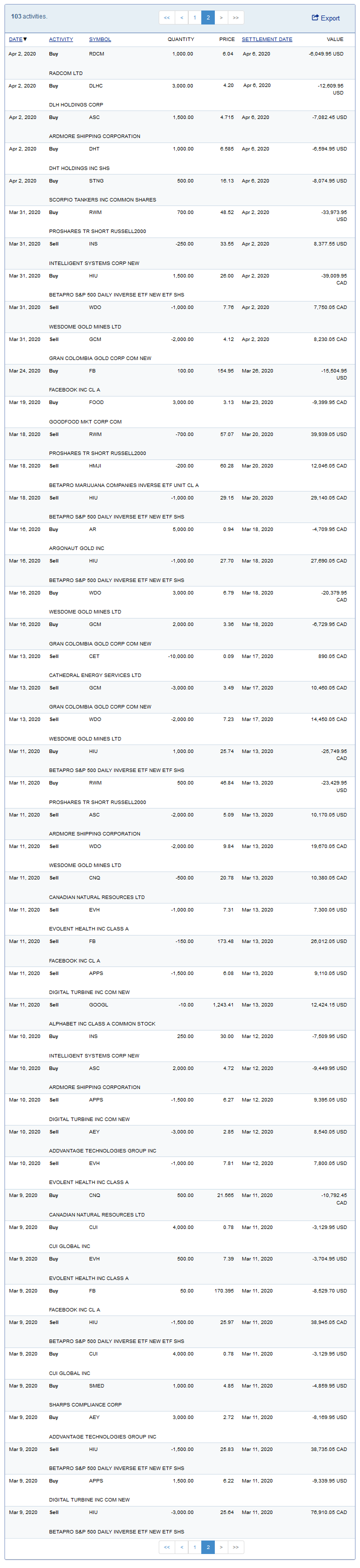

Click here and here for the last eight weeks of trades.

{kind=link}

{kind=link}

What about broadband? Probably demand will go up with work from home and all those extra video conferences (if you pick the consumer facing ones).

Euronav call is interesting. Especially this quote:

“Slide 14 shows the large tanker fleet, we believe, is right for resizing. Financing is becoming ever harder. And with increased regulation from areas like Basel IV and environmental pressure from the EU and the IMO, this is only going to intensify. Contracting of new orders is prevented by the requirement for the new propulsion system in order to meet these new stringent environmental requirements. And with an 18- to 20-year life on average for a VLCC or a Suezmax, ordering a new vessel is also having the additional challenge that the likely medium-term trajectory will demand is also going to be a negative pressure. All of this is just really restricting the new supply of tankers reflected in the 23-year low that we see in the order book.

On Slide 15 to sum up, we look at the continued grounds for optimism at the existing fleet in which the large end of the tanker space, in terms of VLCCs and Suezmax, has an awful lot of potential change coming. On average, for every quarter between now and the end of 2021, there were 27 VLCC equivalents due for special survey on vessels aged over 15 years of age. Why does this matter? The surveys will require several million dollars worth of investment to be spent in order to give your ship certification for the following 30 months. Owners will have to have confidence and visibility that they’ll be able to make a return in this time frame, which, with low freight rates, is going to be harder to justify.

One of a better phrase, this pinch point is critical and historically or often been so. This is usually a catalyst for ships leaving the fleet to an alternative lease or to the scrapyard. To put this into context, though, if 2/3 of the vessels that we see on this final slide were to leave the fleet on Slide 14, the global tanker fleet would resize almost instantly to an oil consumption level of 95 million barrels a day, which is where a lot of commentators believe that even on the barest scenario, that’s where the consumption levels will move off.”

So they get like $10-15m from scrapping. So rates would need to be guaranteed at $35-40k per day to justify getting those tankers back in the market after certification for another 2 years.

And it seems worst it still to come, since oil market is not balanced yet, and European onshore storage is apparently full now. Seems like we might actually have another multiyear oil tanker bull market over the next couple years.

Any thoughts on the latest NRZ deal with Fortress/Canyon? Optics on the deal seem terrible

Its pretty expensive. Not super comfortable with it. You?

Similar position, don’t understand. As a best case, perhaps they see higher 15% – 20% IRR projects and this deal is accretive, but don’t see why the terms had to be so onerous in terms of dilution and cost of debt

The best explanation i have seen is this https://twitter.com/GinSecurities/status/1263232911345664002

Maybe the way the market is looking at it is that there is a “fortress put” on the company?