Research: Big 5 Sporting Goods

I have been surprised that Big 5 has not performed better. One reasonable bear case I can think of is that this year will be a flash in the pan. I looked back at the historical results to see how Big 5 has performed over the last 10 years.

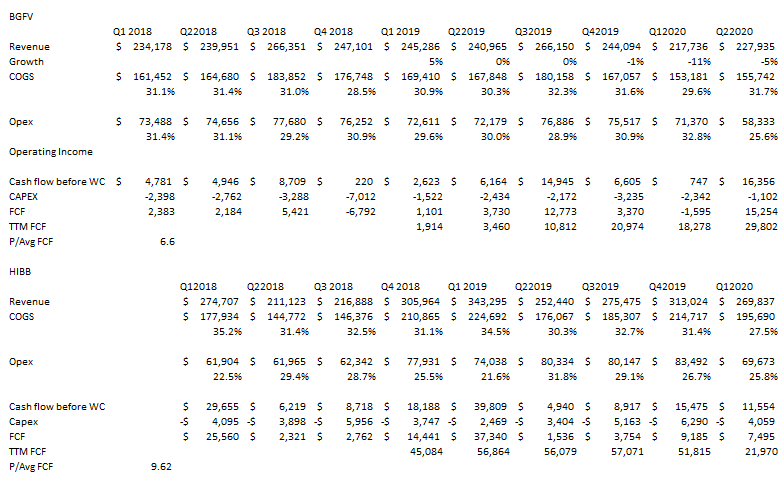

Highlights from Q2:

Highlights from Q2:

Q220 result highlights:

- SSS increased 31.9% in July

- at end of July had no debt and $38mm cash position

- in Q220 they had SSS decrease 4.2% yoy

- in second half of Q2 SSS increased 15.5%

- they had much higher GMs, up to 31.7% from 30.3% yoy – due to product mix favoring high margin categories, less promotional activity

- also they have reduced costs, and reduced warehousing

- SG&A was lower because of “lower employee labor expense reflecting reduced store operating hours and lower advertising expense during the period”

- they are guiding for 5% to 15% SSS increase through the rest of Q320 – would mean 14% to 20% SSS for Q3 as a whole

- EPS for the quarter would be $1-$1.30 per share

- still have 431 stores in operation

- they had opened all closed stores by May

HIBB Comp:

8 Comments

Post a comment

I looked into BGFV and had 2 issues which stopped me from buying. First, its up 6-fold in 4 months and I have not had success buying a stock up that much. Second, they made $1.27 in 2013 and have not come close to that since and have averaged $0.35 EPS for the last 5 years, so their profit this year just seems like it is not sustainable and is more of a Covid-related, people buying lots of sports equipment, excess profit. Am still watching and very interested to see what Q2 results and commentary is like. The Contra The Heard guiys like HIBB (https://www.moneyshow.com/articles/global-51456/) so you are in good company in this industry.

While I get all that, the EV based on their July numbers is $131mm market cap less $38mm of cash and no debt – $93mm. 400 stores, guiding to $1-$1.30 EPS in Q320 and an EV under $100mm? Explain how that is overvalued?

On those metrics, absolutely very cheap. But sporting goods are booming due to the pandemic as per DKS results and others. My concern is that you’ve had a 6-fold increase in price, so the strong Q2/Q3 and overall 2020 is getting priced in. Investors are still going to be looking at what the ongoing non-pandemic EPS will be, which could be back to the $0.35 range. If this increased interest in sports turns out to be a longer trend, these stocks are a steal.

As an aside, like the new research reports – appreciate all the info you are providing.

Hi,

I bought BGFV some years ago. The financials looked good and the book value was equal to market cap. But, after some months of reading about the company, i realized that the main problem was the company’s strategy. The sports retail has suffered a lot of changes during last years: some companies closed all the stores and other companies had been acquired. During those years, while other big companies like Dick’s Sporting Goods were buying companies to increase its market share, Big Five sales increased and the profits were used to pay more dividends. Some of the members of the board are the major shareholders, and looks like the company is taking those decisions to compensate them.

Maybe BGFV is a great short term investment, but not for long term.

I hope that comment it will help you a little. Thanks for your work on this blog, i think is amazing (I’m following you since 2013 😉 )

Regards!

While I get all that, the EV based on their July numbers is $131mm market cap less $38mm of cash and no debt – $93mm. 400 stores, guiding to $1-$1.30 EPS in Q320 and an EV under $100mm? Explain how that is overvalued?

I can’t explain.

Sorry if the comment came across poorly. If there is one thing that I wonder about with BGFV it is why working capital has been consistently negative. If you look at the table I made, FCF before working capital is nearly double that of just FCF in the last 9 years. Seems odd?

Nice buy on BGFV, looks like it is staring another leg up. the sports retailers seems to be in market favour now.