Research: Innodata

Innodata

What they do:

- data engineering

- solve complex data challenges that companies face when they build and maintain artificial intelligence (AI) systems and analytics platforms

- seems like they basically manipulate large data sets so it is more usable

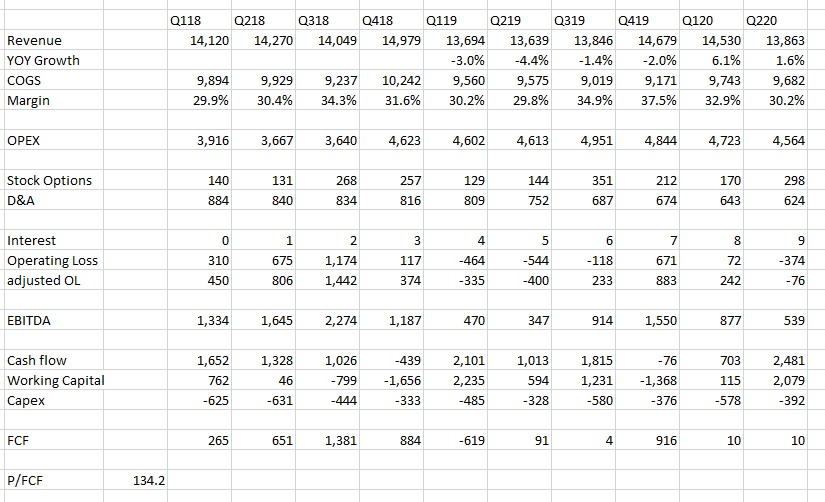

- 27.6mm shares outstanding at $1.95 for $56mm market cap

- they have $11mm of cash and $5mm of debt

- revenues were flat yoy on Sept quarter

- about 35% gross margins

- they made about 3c EPS in September quarter

- they were operating cash flow positive $4mm of operating cash flow in 9m

Employees:

- have 3000+ employees

- deep data domain expertise in various fields, including law, sciences, health, finance, and technology

- process data in over 25 languages

- work from our global operations centers in India, Israel, Sri Lanka and the Philippines

- expert staff provides an attractive alternative to the crowdsourced labor pools of competitors

- well-suited for high-context data, such as legal contract classification, medical images, medical records, and scientific and legal literature

- hybrid approach to produce large-scale, highly accurate data – AI and human expertise to tackle

AI SaaS Platform

- have AI-augmented SaaS platforms

- automates complex data annotation and data transformation tasks

- combines advanced dataflow, deep learning (a branch of AI), and purpose-built applications used by human experts

- enables us to perform data annotation and data transformation at higher efficiency

- dataflow technology enables us to configure workflows for specific data annotation and transformation setting and refining our accuracy thresholds and quality assurance parameters

- our AI is suite of domain-specific and task-specific microservices each of which performs a discrete data-related task

- AI microservices have a range of capabilities for data annotation and data transformation including deep sequence labelling, categorization, segmentation and sequence-to-sequence mapping

- when review required, dataflow automatically routes data to an appropriate human expert

- Synodex intelligent data platform – competes with Risk Righter, EMSI, Parameds and a few BPO companies

- Agility intelligent data platform competes with Meltwater, Cision, Kantar, Infomart and West Corporation

Problem they seem to be trying to solve:

- For AI-based algorithms to perform accurately, they need to be trained on large amounts of high-quality data

- projects fail, stall or perform inadequately because data sciences teams are unable to perform the complex and resource-intensive data preparation tasks necessary to properly train, tune, and operationalize AI models

- preparing high-quality data takes up 80% of the time for most AI and machine learning projects

- 19% of companies responding stated that lack of data or data quality issues was a main bottleneck holding back further AI adoption

New Market Opp

- re-designed our solutions and product portfolio in order to address the needs of enterprises across verticals for data annotation and data transformation

- aim to dramatically expand our addressable market

- historical core market for providing data services to information companies is relatively small (estimated by us to be approximately $250 million and to not show growth over the next several years), the market for AI and machine learning-relevant data preparation solutions is estimated to grow from $1.5 billion in 2019 to $3.5 billion by the end of 2024

- overall enterprise AI spend that is projected to reach $53.06 billion by 2026, registering a CAGR of 35.4%

- intend to shift our revenue mix from “services” to “solutions” and “SaaS products”

What is data preparation?

- data annotation (which is estimated to take up 25% of the time)

- image and video annotation services and platforms may be used to annotate, or label, objects or people in images/video for facial recognition systems

- text annotation services and platforms may be used to convert raw text data into richly tagged, AI training data

- provide image/video data annotation and text annotation as full solutions, in which we provide all required technology, infrastructure and expert resources

- provide data annotation for healthcare, compliance, scientific, financial and legal markets

- data transformation (which includes data identification, aggregation, cleansing and augmentation and is estimated to take 55% of the time)

- data transformation solutions for high-accuracy data identification, aggregation, cleansing, augmentation and extraction

- enables data to be extracted from websites, as well as internal data stores; converted from disparate formats including PDF; enriched with the necessary semantics, metadata and linking; and classified in accordance with an ontology or knowledge graph

- consumed via API

- TAM: AI and machine learning-relevant data preparation solutions is estimated to grow from $1.5 billion in 2019 to $3.5 billion by the end of 2024

- global services and technology company focused on data transformation, enrichment, and management

Q2 Results/CC

- Synodex and Agility: expecting that we grow both of these businesses this year

- Synodex

- have built the technology and systems to extract complex medical data from unstructured medical records

- first half revenues increased 28% over last year, with revenues this quarter increasing 31% year-over-year.

- enjoys strong 60% plus incremental margins, and nearly all of its revenue is recurring in nature

- Agility

- SaaS Platform

- providing full PR workflow platform

- small player in the overall $3 billion global PR workflow market

- ended the quarter with a year-to-date net retention of 87%, just a few points shy of our internal target of 90%

- booked about $750,000 of new business with a small direct sales staff

- from Q1 2019 to Q4 2019, we practically tripled bookings per sales executive.

- given improved productivity, economics now support rapidly scaling the sales force

- on AI market:

- late last year, we discovered a whole other market, practically made-to-order for us, just in its formative stages with significant growth expected in the next several years. This market is the AI data preparation and annotation market

- Data sciences teams that want to build AI models need to train those models with large quantities of very high-quality data. But they express continued frustration that creating high-quality data is a task for which they are ill equipped

- started marketing and selling AI data prep and annotation services in Q4 of last year

- have closed 15 new customers. We have another 16 customers in late-stage pipeline that are expected to close in the second half.

- majority of these deals will produce recurring managed services revenue at our target margins.

- one of our recent data annotation wins is with a prominent big tech company

- did a very important release just in the fourth quarter. And the result of the work that we’ve done, the release that we’ve done is enabling us to compete with the 2 largest companies that dominate this market.

- product has been validated by Atlas and ranked highly in, I think, 7 out of 9 areas. It’s ranked as the top product

- saw a couple of important acquisitions take place last year in this space. One of which was -I want to say it was 5x revenue, their valuation

- Forecast:

- new data annotation market in combination with a forecasted expansion from one of our largest traditional market clients will nevertheless enable us to show sequentially improving revenues

- just the first half of 2020, we have already booked 71% of our full year 2019 bookings

- presently forecasting beating 2019 bookings by 32%,

- expect that the result will be a net savings of approximately $2 million in 2020 and $2.6 million in 2021

Tough to buy this after the big move.

Tough to buy this after the big move.

4 Comments

Post a comment

Good summary. I own this one and have held for a few years and am finally back to break even. The new news is promising, so I’m going to hold for now and hopefully get a couple quarters of good results, which excites the market and I can make a good sale.

The other thing about INOD is management has tended to be overly optimistic and over promise and under-deliver. Hopefully this is not another of those times.

I don’t get why it popped at the time it did? It wasn’t right after earnings, there wasn’t any news. Honestly I can justify buying it at $2 from what I see but I’m worried there was one of those stock board pump and dumps that caused this run up (since I can’t see what else would have caused it) and that this isn’t real buying. But I don’t know. Any thoughts?

Yeah, I’m not sure why it jumped the day it did either. Maybe there was some pumping going on. Optimistically, it is a small company and it just took a couple weeks of the potential business transformation to get into the market and then some big players bid the stock up taking large positions.

But I very likely would not buy it now if I did not own it. But since I do own it, I think it is worth holding for a while and see where it does go.

Sold half today at a little oer $4.00

Think I will let the other half ride for a while and maybe we can see another big pop assuming good news comes out.