Research: PagerDuty into Earnings

So just like HOME, PD is going to report after a big move. I reviewed the stock again to decide whether to sell some or all before earnings. With HOME I ended up selling 2/3 (should have sold it all). I wasn’t planning to but the stock went crazy yesterday which forced my hand. Same thing looked like it was going to happen with PD but it reversed so fast today I’m not sure whether I will sell or not any more.

General

PagerDuty

- collect machine generated data from any software enabled device, combine with human response data and analyze it

- their tech sits on top of company’s technology system

- takes in data from underlying applications and applies automation and machine learning to orchestrate actions of experts to fix problems it has identified

- so PD can look at incidents, compare to past incidents, address severity on past, route to proper DevOps person

- in an abstract description:

you need solutions to understand how that technology is operating, automatically use software signals to detect whether something is having a problem or not. And then getting those software signals turned into actionable work and routing that work to the right people in the right moment to solve a big problem at the right time is super important.

- ingests all of the incoming alerts from monitoring tools, analyzes and whittles them down to ones that require responses

- it’s a way of detecting issues quickly through data analysis:

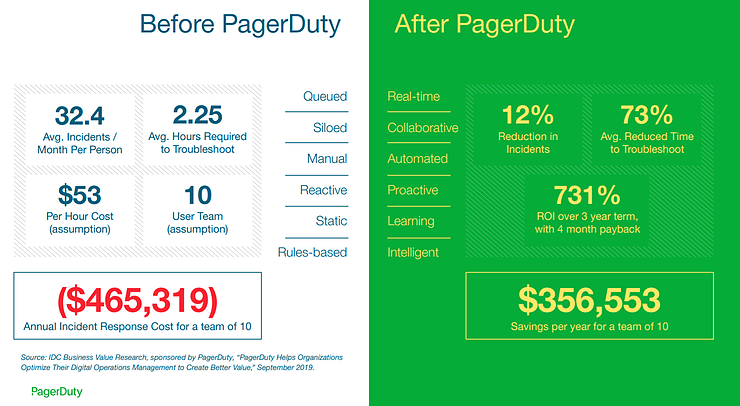

ROI

- they claim IDC has identified 731% ROI for customers over 3 yearrs – by reducing number of incidents, time to resolution

- the ROI is tied to down time or disruption time – makes it quantifiable

- example of a large retail bank in the U.K. that’s got millions of customers and thousands of employees. And when they implemented PagerDuty, they saw an 85% reduction in the number of nonactionable alerts that were coming their way

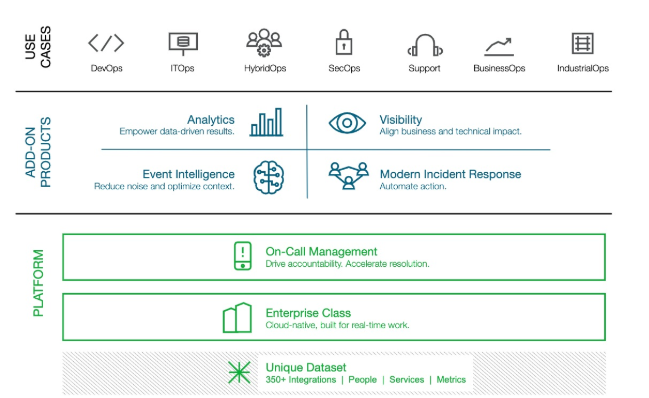

Developer Focus

Developer Focus

- product has been focused on software developers – on DevOps – so resources that are focused on issue investigation

- have many large developer focused customers – Twilio, Zoom, Box, Elastic, Datadog, Okta, Cloudflare

- platform is cloud-native

- can drop PagerDuty into a small team and have it up and running in 10 minutes

- one primary products (on-call management) and 4 add-on products:

- they are tied into data sources like: AWS, Datadog, HashiCorp, New Relic and Splunk

- also have bidirectional integration into Atlassian, Microsoft VSTS, Salesforce, ServiceNow, Slack

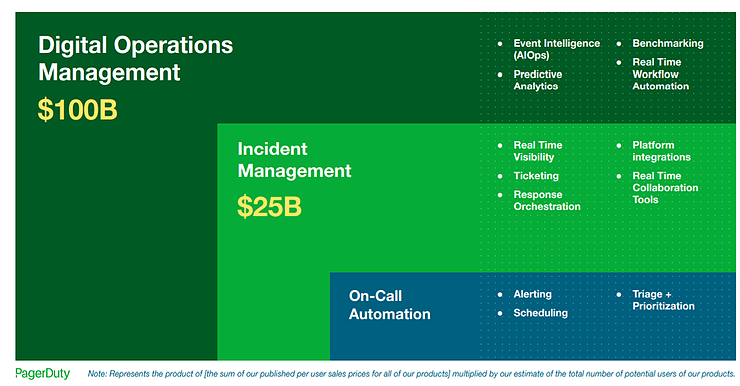

TAM

- they estimate their addressable market is $25b

- based on 85mm potential users x $295/y in revenue

- this is the size of the DevOps or incident management market, which is their traditional market

- the 85mm users comes from this:

- right now PD has 348 customers with $100k+ ARR

- reason for smaller deals is likely b/c

- 12,000 customers – 1/3 from Fortune 500

- 16% of those customers are outside of DevOps

New Market Penetration

- so traditional market is targeting DevOps in incident management market

- trying to enter a broader enterprise market – where apps would be built on their platform

- they estimate the size of this market at $75b, so much bigger:

Digital Operations Management

- examples of enterprises using PD for Digital Operations Management:

- Box uses PagerDuty to help ensure that its services are always available to its customers, leveraging PagerDuty Modern Incident Response to run automated response plays that enable teams to mobilize faster and take action in real time.

- GoodEggs uses PagerDuty to enable warehouse operations and development teams to analyze signals from refrigeration units to ensure food stays fresh for deliveries.

- Petoton – have been using it for application development and track issues but are starting to use it to track shipments with customers

- The Gap – uses PagerDuty to directly connect product and IT teams as well as distribution centers, creating smarter, more streamlined approach to handling incidents. We estimate that this digital operations upgrade will save Gap millions of dollars per year.

- large oil and gas organization uses us to manage the efficiency of their fuel trucking terminals.

- We have a payments customer that uses us for their physical security team as well as legal.

- We have a large software company that uses us to manage the real-time workflow across the legal team when they’re trying to finalize contracts across business units

- have a significant number of customers who have adopted us primarily in — for the security use case, particularly as you see DevSecOps taking hold in organizations; and also customer service, where increasingly, the reason customers are engaging with companies, because they’re having a difficult time, tends to be rooted in an issue with technology, the mobile app, the digital app, I can’t finish this e-commerce transaction, I can’t find the pricing that I thought

Competition

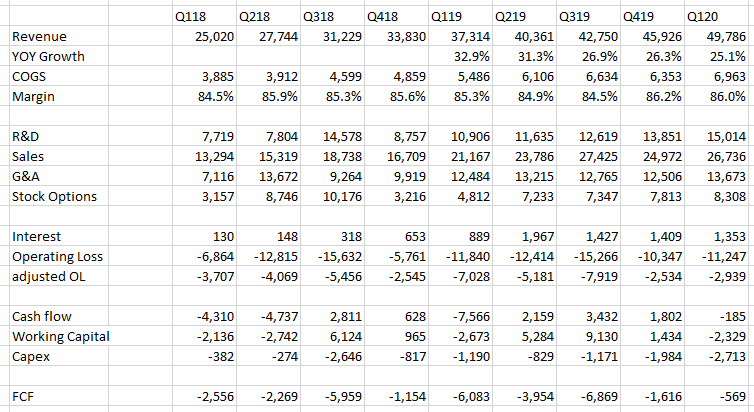

- saw expansion rates decel from 140% plus in 2019 to sort of 122% – I think this was the big negative on the stock over the last number of months

- primary competition is OpsGenie by Atlassian and VictorOps by Splunk

- OpsGenie had 1,396 customers Q2 2019 when Atlassian acquired it

- Atlassian did a new release of OpsGenie with integration with Jira, Bitbucket in June

From William Blair (June2020):

- vast majority of our new customer acquisitions are uncontested

- Let’s touch on competition. It comes up all the time, and you guys probably hear this a lot. But there’s a couple of competitors out there that, certainly, if you take — they’ve cut pricing, some very dramatically.

- in response Tejada notes 95% retention, that they are integrated into 275 of most popular and important apps, not worth ripping out for 10-15% opex savings

- also on enterprise: And then the last thing that I would just mention is we’ve made a significant effort that has really paid off in moving to enterprise, right, in that — we really don’t see any competition in enterprise per se

- she also mentioned lack of competition on enterprise in Q1cc

- they said their churn in SMB in Q120 was macro related

Impact of Covid

- been a mixed bag

- grew ARR in Q120 by 55% – that is an acceleration

- strong quarter with largest customers

- weaker with SMB

- saw deals take longer

- also customers seeing 2x to 11x number of incidents

- seen an acceleration of digital transformation activities that would have taken them years being pulled forward and now being completed in months

- an acceleration to cloud adoption and cloud migration

- know that when PagerDuty is deployed with a cloud migration initiative or cloud adoption initiative, that initiative goes faster, a factor faster (inaudible)

- we think that these are tailwinds that long term are going to continue to be very strong for PagerDuty.

Convertible

- sold $250mm of 1.25% convertible

- price on convertible is $40

RBC on PagerDuty (Aug 28th)

- believe that estimates are reasonable

- SMB is 20% of ARR which is going to be a headwind – saw higher churn in Q120

- feels to me like a beat is almost expected here because the consensus revenue number ($50.7mm) is conservative

- job posting data for PD hasn’t been great – negative QoQ in both Q2 and Q3

- They aren’t quite as reasonably priced as they were when I bought – 15x P/S is a lot more than 9x

- I’m also not sure they really benefit that much from COVID – their pricing is seat based so its not like more incidents from their customers means more revenue

- Finally, OKTA and TEAM seem to be putting on a pricing war

- On the other hand the damn stock crapped out today on a sector rotation – if it was $37-$38 still I think I’d sell at least 2/3