Research: Inspired Entertainment

I bought a small bit of this one this week at a little under $3. I don’t love it, but I do think its reasonable and its probably a bit of a post-COVID play, given that they were getting creamed on the top line from casinos and bars being closed or empty. But I remain a little wishy-washy on it because I played their virtual games online (you can play them for free here) and they were kinda boring to me and they don’t really generate FCF so far.

Just to catch up on the week, I also bought some ELMD today, I’ll get my research on that out. I’ve been watching that one for a while, it has been quite the waterfall but its getting back to a level it seems interesting. I also bought some CWH earlier this week on its pullback, sold my Luby’s yesterday, sold 1/3rd of my Innodata on the pop earlier this week (why is it going up?) and sold Enlivex on the COVID results (its like 5 patients so its probably a little ahead of itself, though it does make sense as a treatment).

Anyway, here is some notes on Inspired Entertainment:

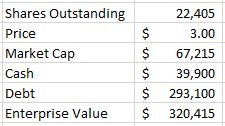

- $67mm market cap at $3.00, whole lot of debt

- global games technology company

- supply virtual sports, mobile gaming and server-based gaming systems

- customers are lottery, betting, gaming operators

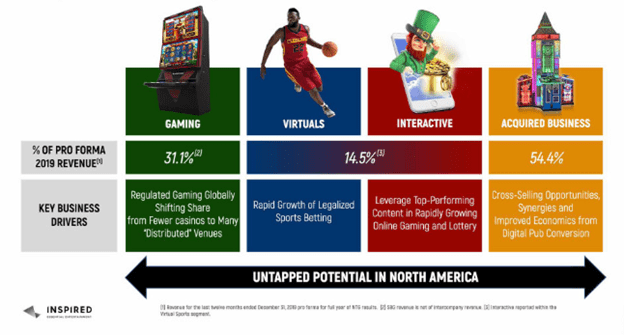

Segments

- operate 4 segments:

Gaming

- gaming is digital slots and gaming machines that are in casinos, bars, etc

- server based so you get change in/out games without replacing machine

- 2,900 additional terminals contracted for deployment

- 32,800 terminal out there at end of Q220 – this is down 10% yoy

- they collect revenue sometimes on sales of SBGs and sometimes through participation

- their games are located on a network – distributed to casinos, allows them to access broader market

- They get an avg participation rate in the games of 6% – so 6% of profits goes to them

- They describe it like this – Customer Gross Win accrued in the period after deducting gaming taxes (defined as a regulatory levy paid by the Customer to government bodies) and applying the Company’s contractual revenue share percentage

- This has been majority of revenue – more than half last year, and was ~70% of revenue in Q419 before COVID

- Operate in UK, Greece, Italy Illinois

- 75% comes from UK operations

Virtual Sports

- available in 44,000 retail channels, 300 websites

- they receive portion of revenue generated from the game plus upfront license

- these are games like Golf, Basketball, Soccer, Horse Racing, etc:

- It doesn’t look like its real players or teams, they use plays off of names

- Its not exactly a video game, it looks close to real, and you basically watch a match, which is not a whole match – for golf its like a hole or 3 holes – and you bet on the winner, long drive, etc

- I played the golf and basketball, it seems kinda boring to me tbh but what do I know

- I think the “interactive” segment, which is just a subset of Virtual Sports, are just the games that aren’t sports related, so the bingo, lotto and the Centurion and Reel King – which are just slots from what I can tell

Novomatic

- This is the acquired business

- acquired Oct 2019

- supplier of Category B1, B3, C and D gaming terminals

- while the other segments are asset-light these guys are basically terminal manufacturers

- this is a different business than the rest – these guys sell “analog machines” while the rest of what they do is digital gaming over a network

- products are installed at pubs, arcades, motorway service areas and holiday resorts in the UK

- but it is a high margin business – if you take a look at the Pro-forma below its more than 75% gross margins

- I’m not sure I understand the acquisition – it seems to be something about taking this Novomatic and making their analog machines, which is their bread and butter, digital, to make them more profitable

- They go to pains in their presentation to differentiate and show how much digital is:

By Area

- have 16,000 machines in UK – this seems low?

- Scotland is about 10% of volume

- – 8,300 machines in Greece, recently deployed 380 Valor terminals

- Recently sold 161 Valor terminals in Illinois – said they have sold 275 in the US in total – I’m not sure if that is all Illinois or some other state(s) as well?

- Are planning to deploy 100 terminals into Western Canada

Financials

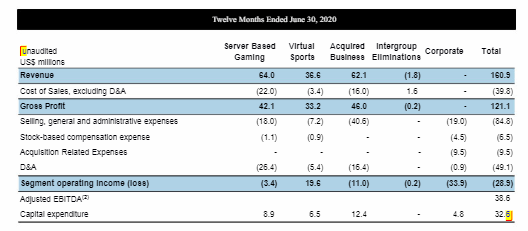

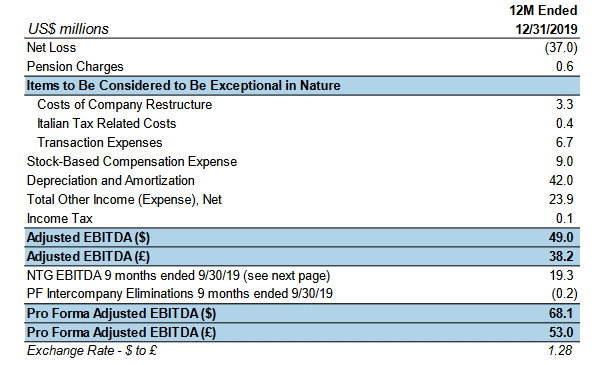

- this is the pro-forma EBITDA including the Novomatic business for 2019:

- would have been $68mm

- right now EV is $320mm – 4.7x EBITDA

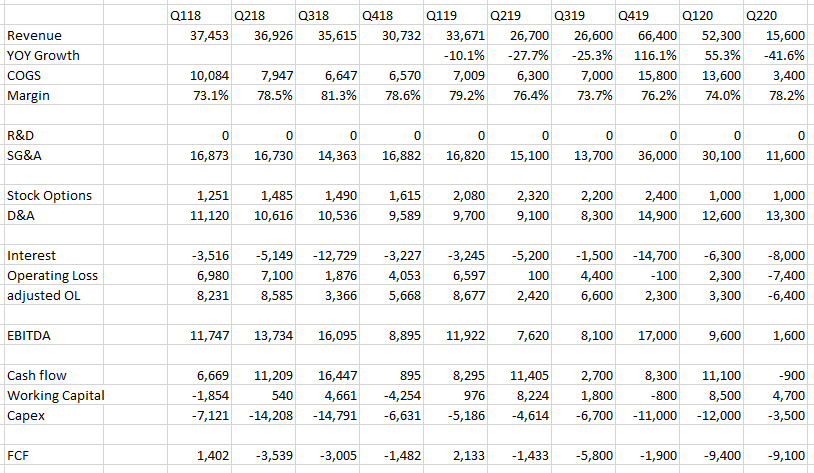

- They generate decent EBITDA but it doesn’t really follow through into FCF:

- I probably need to dig into why the FCF is so bad (whats the CAPEX?)

Customers

- operators of lotteries, licensed sports bookmakers, gaming and bingo halls, casinos and regulated online operators, adult gaming centers, pubs, holiday parks, and motorway service areas

- key customers: William Hill, SNAI, Sisal, Lottomatica, Betfred, Paddy Power Betfair, Genting, Bet365, Sky Bet, Fortuna, the Greek Organisation of Football Prognostics S.A. (OPAP S.A.), GVC Holdings Plc (including Ladbrokes Coral), the Pennsylvania Lottery, Bourne Leisure, Greentube, Stonegate, Mitchells & Butler, Marstons PLC, Greene King, JD Wetherspoon PLC, Park Dene Resort, Centre Parcs Resorts and Novomatic. Geographically

Q2 Results

- basically, their entire retail business shut down in March

- their online business accelerated – Virtual Sports:

Our Q2 performance is noteworthy due to the outstanding performance from the online virtuals part of that business, which increased over Q1 by 76% and was 109% higher than the same quarter in 2019.

- their retail business is small, local venues, expect them to come back online quickly

- said they are beginning to see a quick ramp in Greece, Italy and UK

- in Greece operating above pre-COVID levels

- in UK are seeing less machines operating at William Hill due to distancing

- Italy numbers close but slightly lower than pre-covid

- they reduced their headcount from 1,800 to 300

- managed to be EBITDA positive in Q220 – $2mm of EBITDA

- their margin actually goes up when shops close if revenue of remaining shops increases proportionately