Research: Daseke

I’ve been following Daseke ever since they took over another company I used to own called Aveda Transportation (I think that was 2018?). There was a large contingent payout for Aveda based on EBITDA that quite honestly I think us shareholders of Aveda may have been screwed out of, but whatevs, that business basically imploded with oil and has been a disaster for Daseke so it turned out okay anyway.

Daseke put together another good quarter. That is two in a row. Some of the sequential improvement was one-time in nature but the new management team has clearly turned things around since the old founder Don Daseke was let go.

I don’t own the stock but I do own some of the old SPAC warrants which covert at $11.50 and expire Feb 2022. They remain a long-shot but I paid about 15c for them and it just seems like on the off-chance that Daseke continues to improve through 2021, maybe we get an infrastructure bill, maybe wind continues to take off (they ship a lot of turbines on their flatbeds) that the warrants are as good of a moonshot as anything else right now.

That said, while the quarter was good, it seems to have a lot of one-time tailwinds so I’m not sure how sustainable this stock move yesterday is.

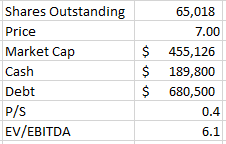

Here’s where we stand with share structure.

So based on TTM EBITDA I see them at about 6x. Its not incredibly cheap or expensive.

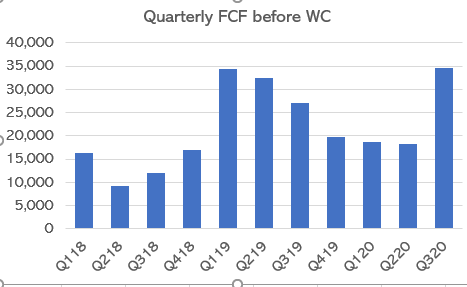

They did generate a lot of free cash again in the quarter:

The thing about the warrants is that because of the leverage, a relatively modest change in valuation or operational improvement can make a big difference to the stock price. So if they get to trade at 8x EBITDA instead of 6x EBITDA (or if, conversely, they can keep the EBITDA improvements coming and say, get to a $50mm per quarter run rate sustainably and a 6x multiple), the common goes to $12 and the warrants are in the money.

So its not impossible. Unlikely? Yes, but not impossible. A moonshot.

Below are the notes from the quarter as well as the notes from the Q2 that I had made previously and I don’t think I ever posted.

Q320

- another big improvement to operating ratio – 92.5% for the quarter down from 96.5% in Q220

- but sounds like this is a bit of one-time anomaly, not really representative of further business improvement

- still focused on getting operating ratio below 90%

- expecting OR improvement in 2021 over 2020

- up to $15mm of net income – 22c EPS

- aEBITDA of $56mm

- have delivered $156mm of fcf year-to-date

- net debt is now under $500mm – down $135mm yoy

- they finished the divestiture of the Aveda shitshow!

- still seeing lower freight volumes in flatbed

- specialized revenue was flat yoy excluding Aveda

- all the EBITDA improvement yoy was from specialized

- had a big (one-time??) benefit from disruptions in wind and high security – this is a lot, $15mm added to EBITDA from these

- kinda seems like these one-timers were all the uplift:

So Q2 was 96.5; Q3, 92.5 million, if I do the back-of-the-envelope math on the $15 million benefit you mentioned this quarter from nonrecurring items or unique items, I guess, this quarter, it implies virtually all of — kind of the sequential improvement was onetime in nature.

- also saw tailwind from COVID cost reductions that won’t continue

- tailwind from wind is contining at least in part in oct

- very difficult to forecast wind – they don’t know how 2021 will look, too project based

- expect insurance to be $2mm per quarter headwind in 2021

- kinda guided to an okay Q4 but seasonality will kick in and make it down a bit

- expect capex of $75mm to $80mm in 2021

- still seeing many of their industrial markets trending down

- seeing pockets of strength in roofing, pgysum, commercial glass

- turnover: finished this quarter, I think, just under 62% in total turnover, which is down from a year ago and down sequentially as well. So we’re having a good year from a turnover perspective – I think its been around this level for at least 2 years now

Q220 results

- they had an operating ratio for the combined company of 96.5%

- best operating ratio since they went public over 3 years ago

- yoy operating ratio improvement of 250 bps

- divested Aveda Transportation and Energy Services – collecting $48mm from PP&E sales so far – but with winddown costs will be $7-$10mm cash drain

- o&g exposure will drop to 2% from 13%

- core business revenue was down 13% in Q220 excluding Aveda – EBITDA down 5% – EBITDA was $45.8mm excluding Aveda – Aveda was a drag of $1.8mm EBITDA

- they actually showed an EBITDA increase in Q220, up 13%

- are investing in their fleet – lowered average truck age from 3.8y to 3.4y from start of year

- it wasn’t totally clear to me but sounds like avg age depends on specialized vs. regular flatbed fleet

- of the 9 operating companies they have, several are operating at “sub-90%” operating ratios today

- their specialized segment is what includes Aveda – it saw revenue of $221.5mm and EBITDA of $33mm – so it is a big driver of bottomline

- their specialized segment OR is 90% – that is up 410 bps yoy

- flatbed segment had revenue of $137mm – this was down 22% yoy

- but EBITDA in Flatbed was $20.4mm – which was up a little yoy

- they decreased net debt $118mm yoy – leveraged at 3x which is below 4x of covenant

- they guided to capex of $60mm to $65mm – this must be $160-$165?

- maintenance capital is in $75mm to $100mm range

- their goal is to get operating ratio down to 90% across all the business lines

- segments that were strong: lumber, wind, defence – while aerospace not likely to come back soon, metals is weak

- July trends are flat – improvement through April, May, June but July is flat

- they expect to see continued OR improvement through the rest of the year

- CEO was “shocked” at resilience of Daseke model – how well freight held up in Q220