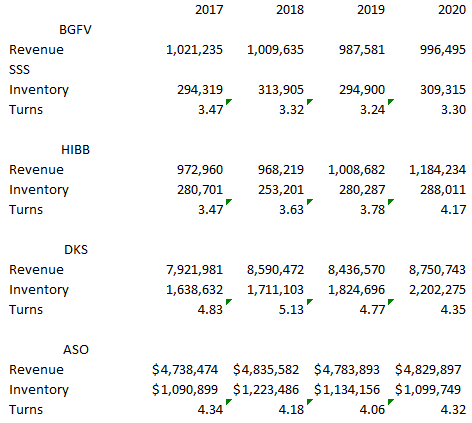

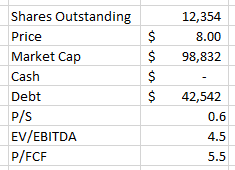

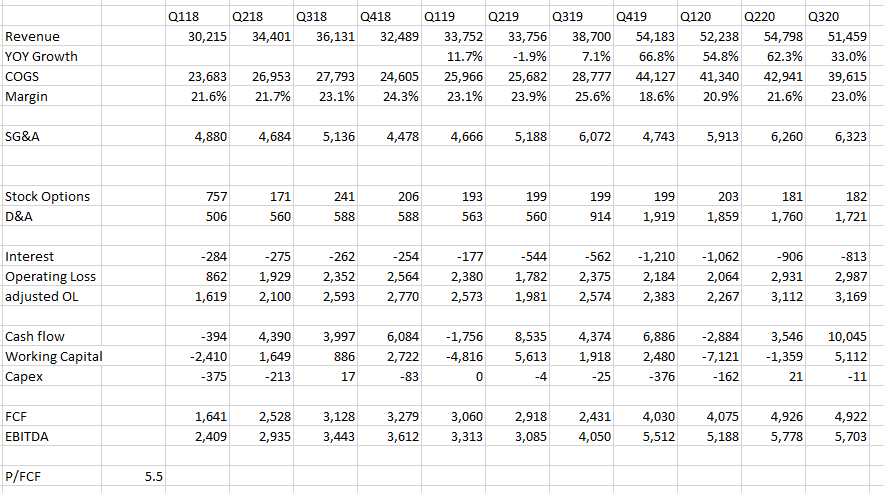

ASO IPO’d on Friday. It was below their target of $15-$17. I bought it under $13. Sports retailers are still doing quite well. BGFV has finally moved. ASO is not as cheap as BGFV but it is more comparable to DKS and HIBB – it is a better business. You can make legit arguments that BGFV does not turn over inventory as fast, that it has no online presence, and that SSS have been much worse than the competition. With ASO they compare favorably to DKS and HIBB, and the FCF they generated in H1 was really good. I imagine they generate almost all of the $760mm of FCF in Q220. Another quarter that is even close to as good would be a signifcant percentage of the market cap and close to enough to pay down the rest of the debt. A couple of charts to demonstrate the comps. I’ll post up some notes on it later.

DLHC is a stock I bought in April and sold later in June or July and now I bought it again on Monday.

They have some debt that they took when they made a big acquisition last year, and they aren’t in a great business or anything – this is basically staffing and project deployment. And they have some customer retention issues – as you’ll read there is a small business set aside that could bump them with the VA, but from what I read they would still end up as a sub-contractor anyway so its not as big of a deal as it sounds.

Its a cheap stock, and really that’s the thesis. It trades at 5.5x FCF. The larger staffing companies trade at 8x to 10x EBITDA. It is not going to the moon but I think it should be worth more than this.

market cap of $98mm at $8

trades at 4.5x EV/EBITDA, 7.1x P/E, 5.5x FCF

revenue is expected to grow if analyst estimates can be believed – 34% growth yoy in 2020

they provide professional healthcare and social services

geared at: large-scale federal health and human service initiatives

over 1,000 employees

100% of revenue is from Federal gov’t

agencies they service include: VA, HHS and DoD from their legacy business

also NIH and CMS from the SSS business they acquired last year

revenue last year can be divided between 3 markets within the Federal govt:

Defense and Veteran Health Services – 45% of revenue

Human Services and Solutions – 20%

Public Health and Life Sciences – 35%

before they acquired SSS the VA was 65% of revenue

it isn’t just contract labor, they do provide labor but also are responsible for delivering some processes,services on behalf of the gov’t

these services are to gov’t – to Veteran Affairs, Health and Human Services, DoD

there is definitely contract risk though – before renewing they had 9 contracts with the VA that were coming due in Oct 2019 – so a loss of these would have been devastasting

there were some contracts that they were precluded on bidding on at renewal because they were supposed to go to small business

but the RFP for the renewal is off the table, at least for now, this is what they said on Q3 10Q:

As previously reported, a single renewal request for proposal (“RFP”) had been issued for the nine (9) pharmacy contracts that required the prime contractor be a service-disabled veteran owned small business (“SDVOSB”), which would have precluded us from bidding on the RFP as a prime contractor. We had joined a SDVOSB team as a subcontractor to respond to this RFP. However, the government has canceled the previously issued RFP for these contracts. The government has neither indicated nor announced its future procurement strategy. Due to the time required to conduct a procurement process, we expect these contracts to be further extended

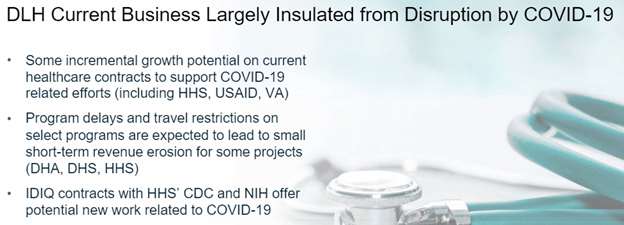

They aren’t impacted much by COVID. In March 25th presentation they said:

– since then have actually won business due to COVID in Q220

– they do have net debt of $42mm – this is down from $55mm at beginning of year – and from over $63mm at time of acquisition

– they took on debt in the large SSS acquisition last year

Q120 Results

they had $5mm EBITDA in Q12020

reduced debt by $4.8mm in January

said past 6m are good benchmark for going forward – had $106mm of revenue, $6.5mm OI, and $10mm EBITDA in last 6m

not surprisingly operating margins are tight – 6% in Q12020

Q12020 results were EPS of 13c, cash flow from ops before WC of $4.2mm, capex is minimal

if I go back to F2019 – EPS was 44c, $13mm of cash flow before WC, $0.4mm capex – so trading at 4x FCF

debt was only $7.2mm in FY2018 – so it was all debt for acquisition

Q220 Results

Q2 was a little weaker

revenue was down a little because of COVID – the revenue they get includes “accommodation” so travel of employees, expenses

saw some organic yoy growth but they didn’t qualify how much

they didn’t get this in Q220 b/c of COVID

but almost all the rest of revenue is directly related to their contract workers:

numbers of workdays and slight things like that, that represents about 93% to 95% of our revenue quarter-in, quarter-out. The remaining 5% to 7% is comprised of what we would call accommodation revenue, so things that you would not independently seek to bid on

still had EPS of 16c per share, $5.5mm of EBITDA

also generated $10mm of cash

debt down to $44.5mm – expect reduction to $40mm by YE

received contracts to assist the National Institutes of Health in their fight against infectious diseases – in this case, COVID-19. With recent awards expected to generate approximately $15 million in calendar 2020

this is related to COVID trial – so I think they are administering the trials, so the amt and timing depends on the progress of those trials

could be additional revenue from other yet to be announced COVID programs – its changing all the time

Social & Scientific Systems Acquisition

provide healthcare staffing

to: Department of Health & Human Services – including the National Institutes of Health (NIH) and the Centers for Medicare and Medicaid Services (CMS) – along with other healthcare-related institutions

400 employees

paid $70mm for acquisition of Social & Scientific Systems, Inc – $63mm net of cash that they would receive from tax rebate

expected that they would contribute $65mm of revenue annually

had a backlog of $346mm at time of acquisition

Acquisition of Irving Burton Associates

acquired for $32mm

provides government healthcare research and IT services to clients including the US Army Medical Research and Development Command, the Telemedicine and Advanced Technology Research Center (TATRC), and the Defense Health Agency.

increases DLH’s overall portfolio of services

likely improves the company’s contract bid prospects relative to competitors in the government healthcare services space.

company’s current revenue run-rate is ~$25M annually with a $143M outstanding backlog.

Rada has been a frustrating stock. The pullback in the stock is unwarranted from what I can see. Rada gets no respect. Even though Rada grew revenue 75% yoy in Q220, year to date order are up over 100%, revenue guidance increased to $70mm, announced another $10mm of orders recently, the stock has gone from $7.75 to under $6 over the last few months.

What can you do? Only buy more, which is what I have been doing.

This weekend I saw the article referenced below. The IM-SHORAD production deal looks like it is done. Rada has been delivering prototypes for testing over the past couple years – now production orders should be coming soon. Estimates are for at least $60mm of revenue from this next year (from Canaccord). Maybe the stock will get some respect.

Notes I’ve accumulated on IM-SHORAD below, including the article.

program is sold to through DRS relationship:

Leonardo DRS. DRS is a major player in the defense electronics market in North America, with a focus on tactical systems and radars. In 2017, we signed a cooperation agreement with DRS to market and sell our tactical radars in the North American market for counter-UAV, short-range air defense, and other solutions. DRS has acquired a few MHR radars and is actively promoting our radars as part of their system solutions. In 2018, DRS was selected by the US Army as the mission equipment package provider for the Army’s IM-SHORAD program, which includes our MHR radars as onboard search sensors

DRS is a prime on the product along with GD and Raytheon (from this article)

Rada delivers the radars, i believe 4 radars per set, 1 set per UAV

from July 2018: RADA Electronic Industries announced that its Multi-Mission Hemispheric Radar (MHR) will be integrated into the Leonardo DRS mission equipment package (MEP) solution for the U.S. Army?s Initial Maneuver-Short Range Air Defense (IM-SHORAD) capability

nine prototype systems will be the basis for a future production decision of more than 140 systems, beginning in 2020.

is a $60mm annual opportunity in 2021 and 2022 – Canaccord initiation report

From Q219 cc:

IM-SHORAD is the army program, the Marine Corp is named GBAD. The army program is not a typical program of record. It evolved as an urgent need to a very rapid program. And probably all of us, some of us have seen that in the U.S. — AUSA conference being depicted as from slide to prototype within less than a year. So I think everybody involved, including the U.S. Army, are very proud of this momentum. The program itself is a sizable program for us. It’s close to 150 vehicles. And if it goes as planned, then it is now — it was already published by the program executive officer that if it started testing, we do see revenue start towards end of 2020 or mainly, again, 2021. And again, the testing and validation typically takes quite a few months until everybody is settled.

from Q419 call:

IM-SHORAD is not yet in a deployable situation. However, let me describe a bit our understanding of the case here. Maybe you have followed and noted that the U.S. Military is actually closing down some forward operating bases and moving troops to centralized locations because they cannot protect and they don’t have enough means to sense and warn against the fires that they have been suffering from recently. So my understanding is that the US Army at least is using what they have already in the inventories. And this is typically the heavy equipment, the C-RAM heavy equipment.

from Q120 call:

We have delivered 7 sets, which is 28 radars, maybe 30 with some spares. We are delivering soon another set of 4. But these are prototype sets, and as we mentioned in the discussion, we expect to get the several production orders later this year.

in presentation estimate it at 600+ radars when all is said and done – maybe more, not sure but Rada references 3x to 5x potential at one point, not sure if that is referring to potential vs. the 600 known radars

The US Army announced last week that it has given the green light for initial production of an Interim Maneuver Short-Range Air Defense (IM-SHORAD) system

article titled: “Huge contract for Israel’s RADA: US Army procuring dozens of IM-SHORAD vehicles”

I bought a small bit of this one this week at a little under $3. I don’t love it, but I do think its reasonable and its probably a bit of a post-COVID play, given that they were getting creamed on the top line from casinos and bars being closed or empty. But I remain a little wishy-washy on it because I played their virtual games online (you can play them for free here) and they were kinda boring to me and they don’t really generate FCF so far.

Just to catch up on the week, I also bought some ELMD today, I’ll get my research on that out. I’ve been watching that one for a while, it has been quite the waterfall but its getting back to a level it seems interesting. I also bought some CWH earlier this week on its pullback, sold my Luby’s yesterday, sold 1/3rd of my Innodata on the pop earlier this week (why is it going up?) and sold Enlivex on the COVID results (its like 5 patients so its probably a little ahead of itself, though it does make sense as a treatment).

Anyway, here is some notes on Inspired Entertainment:

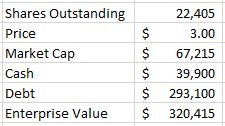

$67mm market cap at $3.00, whole lot of debt

global games technology company

supply virtual sports, mobile gaming and server-based gaming systems

customers are lottery, betting, gaming operators

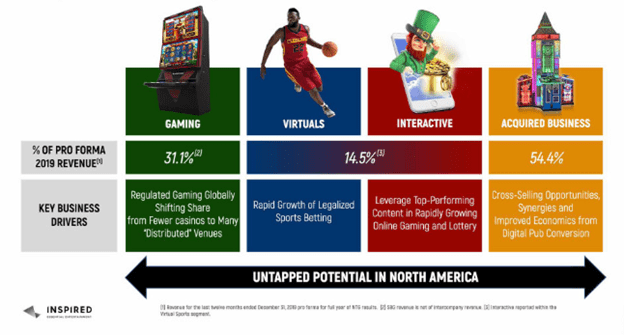

Segments

operate 4 segments:

Gaming

gaming is digital slots and gaming machines that are in casinos, bars, etc

server based so you get change in/out games without replacing machine

2,900 additional terminals contracted for deployment

32,800 terminal out there at end of Q220 – this is down 10% yoy

they collect revenue sometimes on sales of SBGs and sometimes through participation

their games are located on a network – distributed to casinos, allows them to access broader market

They get an avg participation rate in the games of 6% – so 6% of profits goes to them

They describe it like this – Customer Gross Win accrued in the period after deducting gaming taxes (defined as a regulatory levy paid by the Customer to government bodies) and applying the Company’s contractual revenue share percentage

This has been majority of revenue – more than half last year, and was ~70% of revenue in Q419 before COVID

Operate in UK, Greece, Italy Illinois

75% comes from UK operations

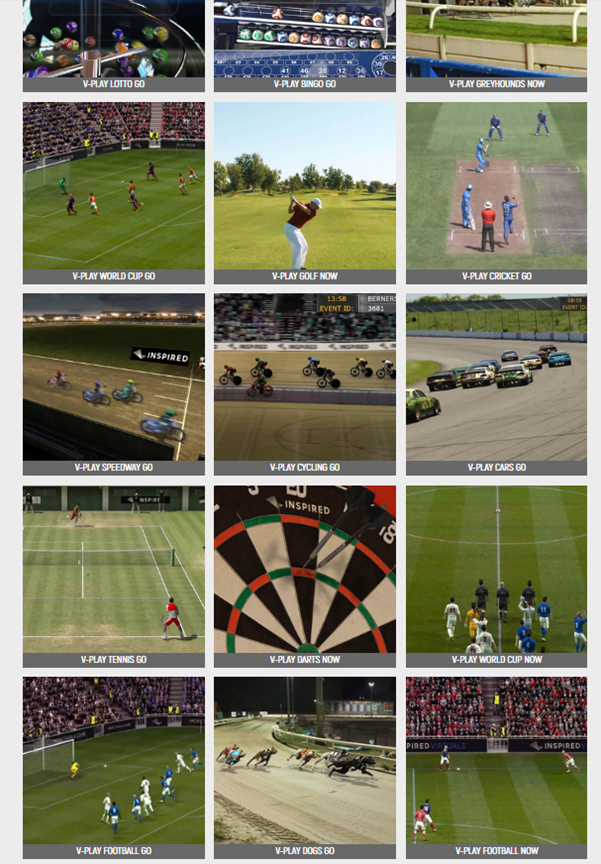

Virtual Sports

available in 44,000 retail channels, 300 websites

they receive portion of revenue generated from the game plus upfront license

these are games like Golf, Basketball, Soccer, Horse Racing, etc:

It doesn’t look like its real players or teams, they use plays off of names

Its not exactly a video game, it looks close to real, and you basically watch a match, which is not a whole match – for golf its like a hole or 3 holes – and you bet on the winner, long drive, etc

I played the golf and basketball, it seems kinda boring to me tbh but what do I know

I think the “interactive” segment, which is just a subset of Virtual Sports, are just the games that aren’t sports related, so the bingo, lotto and the Centurion and Reel King – which are just slots from what I can tell

Novomatic

This is the acquired business

acquired Oct 2019

supplier of Category B1, B3, C and D gaming terminals

while the other segments are asset-light these guys are basically terminal manufacturers

this is a different business than the rest – these guys sell “analog machines” while the rest of what they do is digital gaming over a network

products are installed at pubs, arcades, motorway service areas and holiday resorts in the UK

but it is a high margin business – if you take a look at the Pro-forma below its more than 75% gross margins

I’m not sure I understand the acquisition – it seems to be something about taking this Novomatic and making their analog machines, which is their bread and butter, digital, to make them more profitable

They go to pains in their presentation to differentiate and show how much digital is:

By Area

have 16,000 machines in UK – this seems low?

Scotland is about 10% of volume

– 8,300 machines in Greece, recently deployed 380 Valor terminals

Recently sold 161 Valor terminals in Illinois – said they have sold 275 in the US in total – I’m not sure if that is all Illinois or some other state(s) as well?

Are planning to deploy 100 terminals into Western Canada

Financials

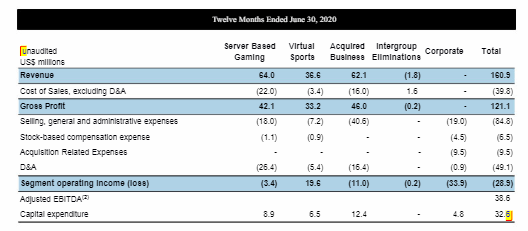

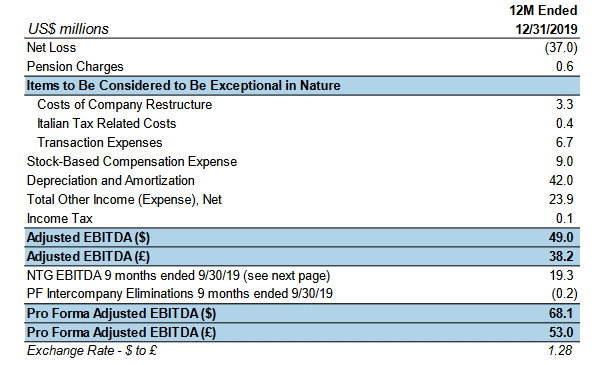

this is the pro-forma EBITDA including the Novomatic business for 2019:

would have been $68mm

right now EV is $320mm – 4.7x EBITDA

They generate decent EBITDA but it doesn’t really follow through into FCF:

I probably need to dig into why the FCF is so bad (whats the CAPEX?)

Customers

operators of lotteries, licensed sports bookmakers, gaming and bingo halls, casinos and regulated online operators, adult gaming centers, pubs, holiday parks, and motorway service areas

key customers: William Hill, SNAI, Sisal, Lottomatica, Betfred, Paddy Power Betfair, Genting, Bet365, Sky Bet, Fortuna, the Greek Organisation of Football Prognostics S.A. (OPAP S.A.), GVC Holdings Plc (including Ladbrokes Coral), the Pennsylvania Lottery, Bourne Leisure, Greentube, Stonegate, Mitchells & Butler, Marstons PLC, Greene King, JD Wetherspoon PLC, Park Dene Resort, Centre Parcs Resorts and Novomatic. Geographically

Q2 Results

basically, their entire retail business shut down in March

their online business accelerated – Virtual Sports:

Our Q2 performance is noteworthy due to the outstanding performance from the online virtuals part of that business, which increased over Q1 by 76% and was 109% higher than the same quarter in 2019.

their retail business is small, local venues, expect them to come back online quickly

said they are beginning to see a quick ramp in Greece, Italy and UK

in Greece operating above pre-COVID levels

in UK are seeing less machines operating at William Hill due to distancing

Italy numbers close but slightly lower than pre-covid

they reduced their headcount from 1,800 to 300

managed to be EBITDA positive in Q220 – $2mm of EBITDA

their margin actually goes up when shops close if revenue of remaining shops increases proportionately