Research: More Digging on Silvergate

More of a dive on Silvergate. The stock has moved quite a bit now, so can’t really justify it as a “bank” like a few weeks or months ago.

But still, I’m reluctant to sell because you can still justify it as a “fintech” or whatever other trendy term you want. The revenue growth here is fee income, which is not really tied to the traditional tethers of a bank. If they grow the number of customers, grow members on the platform then fee income grows and its not really as important what the tangible book value is.

Also, Bitcoin has been going up, so there’s that.

- market cap of $523mm

- book value of $277mm

Operate Silvergate Exchange Network

- entered space in 2014

- Silvergate network was created 3 years ago

- was originally just a way of gathering deposits

- proprietary, virtually instantaneous payment network for participants in the digital currency industry

- offer holding deposits of CC for exchanges, institutional investors, and stablecoin issuers (I think this is other in their segments)

- so it’s a real-time, 24hr payments platform that lets you send USD from one exchange to another in a simpler and lower cost way

- for example if you are an institutional investor, you may want to be switching dollars between exchanges for trading strategies, SEN lets you do that with little friction

- also as exchanges, if investors move from one to the other, or trades occur from one to another, they can swap deposit dollars via the platform

- notable exchange customers are: Coinbase, Genesis Kraken, and Bitstamp

- one thing they do is allow their clients to receive USD payments in scalable fashion, quickly and programmatically

- they don’t charge for use of SEN, so the fee income is from traditional banking of those deposits – wires, ACH, foreign currency exchange

- want to keep barriers of adoption low

- they do talk about charging for SEN though

- the foreign exchange product is relatively new – they have launched it in the last year or so

- foreign currency product took “a lot of work that goes in upfront to establishing correspondent banking relationships with other banks around the world, so we can trade currencies directly with them. But there’s not a significant additional technology spend that needs to happen there”

- they have launched direct access to Swiss fran and euro

- their wire and ACH fee is competitive (ACH stands for automated clearing house)

- in Q220 when fee income was $2.4mm, primarily that was from ACH and wire transfers

- fee income will track underlying activity in the CC markets

- biggest of their exchange customers is JPMorgan Banking

- the deposits from SEN are volatile – exchange and institutional deposits could leave at any time, don’t want to be investing in long-term assets – mortgage warehousing is a good complement to this

SEN Leverage

- also have SEN leverage – this allows customers to get USD loans collateralized by BTC

- can be used to lever the long book, but also to execute trading strategies

- they launched this in Q120

- two strategic partners for Sen Leverage – Bitstamp and Anchorage

- bitstamp is bitcoin exchange in luxembourg, been around 4 years, seems like it is was one of more secure exchanges

- Anchorage is DC asset platform/custodian for institutional investors, their website doesn’t work well, were written up in techcrunch,

- don’t expect to develop their own custody services, will use these partners

- with Anchorage – so Anchorage safely stores the bitcoin, monitors value, interacts with customer on loan draw/repayment, Silvergate services the loan

- but I get the impression they’d be interested in acquiring one – they see having one as “table stakes” for institutional investors

- expect to start small with SEN Leverage – less than 100% of capital – so less than $400mm

- use example of 6000 institutional investors, if each wanted a $0.5mm loan, would be $300mm

- they are limiting growth in this business though, they could grow faster if they wanted to

- they yield opportunity on loans is in mid-high single digits

- make comp to Genesis Capital, which is lending off of Bitcoin collateral:

a firm called Genesis Global Capital. And they announced at the end of the second quarter that they have about $1.4 billion outstanding in a loan portfolio related to digital assets. And Genesis has said publicly that they have about 50 clients that are making up that $1.4 billion number. So as we think about the opportunity for Silvergate, we have those 566 clients that you mentioned, Eugene. And most of those clients are looking for some type of capital efficiency or leverage on their bitcoin. So if you just took a round number and said, 300 of those 566 would be looking for, and I’m just making that number up, but looking for the loan product, and then you say, if it’s $1 million, then it’s a $300 million opportunity. If it’s $10 million, then it’s a $3 billion opportunity.

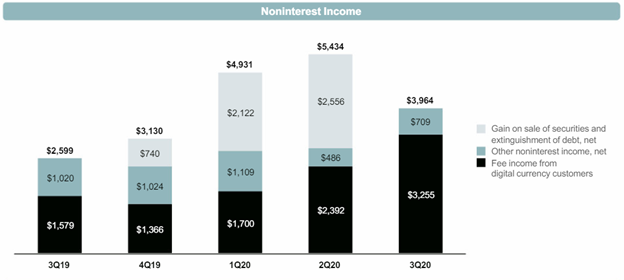

- saw 68,361 transactions, volume of $36.7b – this is up 70% and 65% over Q220

- Digital currency fee income of $3.3mm – up 36% compared to Q220

- say they have over 200 prospective digital currency customers

- Digital currency deposits grew by $586mm to $2.1b in quarter – most of their deposits are digital curency, about 90%

- overall NII was down but that was because of no GOS:

- their fee income is exploding

- consider that net income for the quarter was $7mm and they had fee income from digital currencies of $3.2mm and that is increasing at $1mm per quarter right now

- meanwhile their non-interest expense barely moved, up about $150k qoq

- ROA was 1.13% in the quarter, ROE was 10.14% – these seem like decent numbers even if you are buying it at 1.5x book

Q220 Results

- experienced highest volume of wire transfers ever

- deposits were down quite a bit – from $2b in March to $1.7b – they said this was caused by bitcoin volatility

- their securities portfolio, which is large, has yield of 2.67% – balance $964mm

- had about 13% of loans in deferrment

- they mentioned SEN Leverage – could do $1mm to $10mm loans for the 566 institutional investors, they won’t grow that fast though

- sometime in Q220 the gov’t announced that banks could be custodian for digital assets

- this is important – need ability to custody an asset to be able to lend against it

- have pipeline of 200 prospects that want to onboard with them

- don’t see pressure on existing deposits because we are in 0-interest rate environment, they have seen pressure in the past when competitors willing to offer interest

- have been investing in tax-exempt munis – they see some dislocations from COVID, have had experience in other banks with munis, looking to build portfolio, take advantage

- JPM entering the space – they see as positive for industry, validation of their strategy

- JPM providing banking to Coinbase and Gemini – both of these are clients of Silvergate

- their exchange partners want to have multiple banking relationships

- comments on the OCC announcement allowing banks to be custodians:

the OCC announcements and providing custody, it’s one thing to — for the regulators to come out and say that, yes, that is legally permissible. It’s quite another thing to spin up a custody service for digital assets. And one of the primary differences here, and it’s — at times, a difference that is lost on folks is that with bitcoin and other cryptocurrencies, these are bearer instruments. So the custody regimen that needs to be put in place to safely store a bearer instrument is quite a bit different. Especially a bearer — a digital bearer instrument is quite a bit different than the existing custody solutions that exist in the traditional financial markets. And so those that have been working on this for a while, and there are certainly a plethora of digital currency custodians that have been working on this, I think they’re very well positioned.

- there are players trying to move into full-prime offerings – this is basically becoming a prime broker to digital assets

- Silvergate sees a big part of prime broker business being able to deliver loans on the assets and that is area they are focused on

- talked again about acquisitions to fill out that suite of services for customers with digital assets

Q320 Results

- Silvergate exchange transactions up to 68,361 – 70% increase qoq

- their network handled $36.7 billion of transfers – up 64% qoq

- they generated fee income of $3.3mm from these, up from $2.4mm

- overall though, non-interest income was down qoq because of no GOS of securities

- they did have some fees from mortgage warehousing

- so on a per transaction $ basis fees were $.00009/$ transferred (was about $0.0001 in Q220)

- on per transaction basis was – $47/transaction (was about $59.50 in Q2)

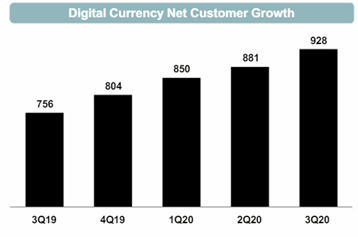

- digital currency customers u to 928 from 881

- digital currency deposits up $586mm – to $2.1b

- started up “SEN leverage” – completed pilot, have approved LOCs of $35mm, up from $22mm in Q220

- exited pilot on SEN Leverage in Q320

- $15 book value

- NIM was 3.19%, which is upfrom Q220 but down from Q319 (3.39%)

- they hold a lot of securities – of $2.42b of interesting earning assets about $930mm of them are securities

- I don’t really see much in the way of Noninterest expense

- 95% of deposits are non-interest bearing

- pretty much all of these deposits are digital currency deposits

- they really saw an increase in onboarding of institutional investors with big money – so in Q220 they have 566 investors with $577mm – so about $1mm per investor – in Q320 they onboard 30 and increased deposits by $270mm – $9mm per investor

- their loan book is residential, commercial, mortage warehousing

- LTVS are 53% for commercial and MF, ad 55% for SF

- they have very small NPAs – 0.16%

- they have $143mm, or 19% of loans modified – consisted of 56 loans – but down to $32.7mm at end of Q320 – 4.4% of loans

- on the CC one analyst (Block Research??) explained recent developments:

Just the announcements that have come out even in the past few weeks, whether that’s SEC’s second interpretive letter on banks holding reserve assets behind stablecoins, corporate treasury balances into bits from some companies, PayPal, obviously, last week. You mentioned not providing guidance on SEN volumes per se, and we talked about the strategic rationale for not charging for SEN.

Barclays Conference

- not much new here

- on MicroStrategy:

And then when you think about sort of what’s going on in the macro environment in terms of fiscal and monetary policy, what we’re seeing is we’re seeing macro investors look at the asset class and make an allocation to bitcoin. And I guess 2 of the examples that I would highlight are Paul Tudor Jones earlier in the year, and then recently, a publicly traded company called MicroStrategy that trades on the NASDAQ. MicroStrategy, I think, sort of took everyone some — for a surprise in the sense that they’ve looked at — they’ve clearly done their research on bitcoin. And just this morning, announced that they’ve upped their allocation in bitcoin to $425 million. To put that number in perspective, they have a total market cap, they trade on the NASDAQ, and their market cap is about $1.3 billion. As of quarter end, I think their total balance sheet was about $850 million.