Revisiting IDT – again

IDT is at it again. They are generating free cash and incubating businesses. Spin-offs will be soon to follow.

A brief history of IDT:

IDT is run by the Jonas family (first father Howard, now son Samuel, and I think some other relatives are involved). They are majority owners and they run this business however they see fit. If they don’t want to answer questions at an earnings call, they don’t. If they don’t like a question on the call, they say so. They do want they want and disclose what they want.

In other words they don’t really care about what shareholders have to say. And you know what? I am okay with that because the Jonas family does one thing very well – make money for shareholders. If they make even more for themselves in the process, who am I to protest?

The IDT template that has played out 5-6 times over the last 10+ years: They start with their boring legacy business of international calling and carrier services. This business does not grow very much but does spit off a lot of cash. Then they use the cash to incubate losses from new, fledgling businesses that are started. Once those fledgling businesses gain traction, they spin them off into their own companies, with the shares going to existing shareholders.

They did this with IDW Media, Genie Energy, StraightPath, Zedge and Rafael, and that is in addition to Fabrix, which rather than spin-off they sold to Ericsson for $65 million. If you aren’t familiar, look up the history of StraightPath and what happened to that stock.

After the Rafael spin off in 2018 it looked like the cupboard was bare. But as the old saying goes, never count out a Jonas.

I hadn’t looked at IDT since Rafael. What brought it to my attention again was simply that the stock was up. Given that IDT gets no respect, I figured that a move in the stock like we have seen was most likely because something good was happening.

It turns out that was the case. The folks at IDT are doing what they do best, incubating businesses and letting them grow.

This time around we get three nascent businesses:

- BOSS Revolution Money Transfer – an international money remittance/payment transfer

- National Retailer Solutions – nationwide POS payment processing solution aimed at independent convenience store

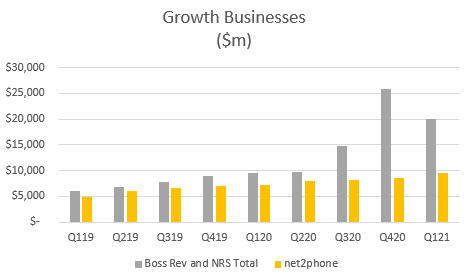

- net2phone – a UCaaS cloud communications solution aimed at LatAm

The BOSS Money Transfer and NRS businesses are both growing at 100% yoy. net2phone is growing at 40% yoy.

Both the money transfer and payment processing businesses have recently announced expansion plans. The next step for Boss Money Transfer is to become a neo-bank (in all probability the Jonas’s have noted that neo-banks (like chime) get ridiculous valuations and all they really do is collect interchange fees, which BOSS already does with transfers). IDT first mentioned this on the fiscal Q4 call two weeks ago:

we will roll out BOSS Money Visa card in peer-to-peer transfers early next year. This is the first step in a broader and strategic challenger bank initiative that we are now focusing on to help our immigrant, underbanked and unbanked customers conveniently access and participate fully in the digital economy.

With NRS, the expansion will be to a broader range of locations. Right now NRS is focused on independent convenience stores, of which they are in 12,000 locations and increasing those deployments by 450-500 terminals per month. The expansion will target liquor stores, gas stations and fast-pay restaurants.

The NRS business is particularly interesting because companies in this space get eye-popping valuations. Consider Lightspeed POS. Lightspeed recently made two acquisitions: Upserve and ShopKeeep

Upserve is a POS platform for restaurants. Lightspeed bought it for $430 million, which is 10-11x trailing revenue.

The second was ShopKeep, a general small-business oriented POS. Lightspeed bought ShopKeep for $440 million. That works out to a multiple of about 9x trailing revenue.

NRS has trailing revenue of around $15 million. And like I said, it is growing at 100%.

Now NRS, like all things IDT, is not going to have a flashy, silicon valley start-up type of look or feel. That simply is not the way that IDT works. Check out the website of NRS. Now look at ShopKeep and Upserve. The latter two look slick and hip. The former looks like an infomercial.

But here’s the thing about IDT. That is just the way it is. You are always buying businesses that make you purse your mouth and squint your eyes. But these Jonas guys find a way to make money.

You can make a simple argument for IDT on valuation. The market cap of the stock is about $330 million. There is around $128 million of cash and securities on the balance sheet. So the EV is about $200 million.

In the last 4 quarters IDT generated $40 million of free cash ex-working capital. That puts you at a 5x FCF multiple.

All of that free cash flow is coming from the boring legacy business. Each of the incubated businesses are losing money right now. But they are also all growing with leaps and bounds.

The NRS business could be worth a significant part of IDT’s capitalization already. 10x revenue on $15 million puts you almost there. Even at 5x you are half the EV.

The Boss Money Transfer business, which has done $55 million in revenue the past 4 quarters, could get a 1-2x revenue multiple just on a comp with MGI, or it could be much higher if IDT is successful in their bid to turn it into the next neo-bank.

net2phone has $34 million in trailing revenue and I don’t even know how to value that one. True UCaaS businesses get 5x revenue multiples and some much higher.

My bottom line is that I don’t know what all these parts are worth. But who cares? They are worth more than the current price of the stock. And you are betting on the jockey here. If history is any guide, the Jonas team will find a way to realize that.

Investing in IDT always gives great results. I discovered Jonas family through your website. I invested in IDT, Straight Path, Zedge, always giving big yields (Zedge appart). I read Howard Jonas book also, which gives his point of view of how he does business. Now Rafael Holdings looks promising, and seems that is the big bet of the whole family.

I’m always waiting for a new IDT movement, and as you comment, those new business could be the next corporate action.

Regards!

Curious why you say Rafael is the big bet of the whole family.

In fact, I didn’t know how many members compose the Jonas family. But the funds of Liora, Michael, Miriam, Samuel, Jonathan, Joseph, Rachel and Tamar Jonas, are invested in Rafael Holdings. Like they have in IDT or Genie Energy, but on the other hand they are not all invested in Zedge, for example.

Howard took the reigns of Rafael Holdings, which is Chairman of the Board. When was incorporated, Jonas and his wife had lend money directly to the company. They do also at this moment through a hedge fund. Maybe they did the same kind of transactions with other companies, but for me it seems they are very active with Rafael.

Wow I had no idea. Thanks. Interesting they are so heavily in Rafael. Just had a discussion about how Rafael doesn’t really seem to have a blockbuster, their drugs are better than what’s out there, but not game changing. Thoughts?

Thanks so much for the insight.

As far as not having a blockbuster drug – have you seen the VIC write up on Rafael from Oct, and the description of CPI-613. Some pretty outlandishly bullish projections in it, but it does seem like there will be an announcement on its FDA approval by end of Q1. Who knows – but I sold out of Straight Path because I didn’t understand spectrum, so while it may be a mistake, I do not want to have the same regret here on Rafael. https://valueinvestorsclub.com/idea/RAFAEL_HOLDINGS_INC/1411438842

Pretty funny–went through exactly this thought process last week, and then last night they filed their investor presentation. I think you nailed it: it’s hard to tell exactly how the value’s going to be realized with IDT, and the fuzziness of the story itself is part of why the opportunity exists. Even excluding Straight Path, the spins over the past 11 years have returned multiples of IDT’s value at the time (even if you don’t measure from 09’s lows), and there’s no reason to think they won’t continue creating value strangely but well.

Completely agree. Rafael is not developing blockbusters. Devimistat for example is a complement for treatment on pancreatic cancer, but not a standing alone drug. Is a drug which improves the treatment.

What’s really interesting are the steps which Rafael is already doing on the commercialization, before having any FDA approval. Some of their developments have the orphan drug designation, and the company signed an out-licensing agreement with Ono to commercialize Devimistat in Japan.

Looks like they want to do business as fast as possible. Devimistat also received the fast track designation.

I realized in different forums that Rafael stock is sometimes misunderstood because is classified as a Real State company XD

The IDT investment in MarketSpark looks like a potential high growth situation as well. Very excited about that. https://www.crunchbase.com/organization/marketspark/company_overview/overview_timeline