Research: Bionano

Bionano is another one of these examples of finding a stock shortly before it takes off. I don’t know why it happens that I research something and a day or two later a press release comes out and I am left scrambling, but it happens over and over again. And while I really don’t like writing about something that just popped like Bionano did yesterday, the blog is locked (again) and I am trying to write mostly for myself, so I need to write about what is top of mind. Just bare in mind that the news announced yesterday was not really all that earth-shattering. It is another layer of evidence that seems to be proving out that Bionano’s Saphyr system has a larger place in the genomics ecosystem, which is what I am going to talk about.

I stumbled on Bionano twice. Oppenheimer had a note on Bionano back in mid-November. I read it, and flagged it, and then promptly forgot to follow up. Then Oppenheimer had another note on them Monday and I was like, oh yeah, I meant to look into that, so I did.

So I dug into Bionano on Monday and (of course) yesterday the company has a press release. I had learned enough about Bionano that I had decided I was going to buy the stock and it did not pop right away in the morning so I had a chance. You could call it lucky or unlucky timing, depending on how you want to frame it. But I don’t know if that pop will stick – like I said the news is not really a game-changer in and of itself.

There are a few angles to the story. First, for the last 10 years Bionano has been a company with one of these ‘platforms for research’ business models that doesn’t generate much revenue because the market is limited to a few labs. They have been selling their platform for a decade with only niche success. The story today is that this could be changing.

There have been a number of papers published this year where doctors are saying that Bionano’s platform (called Saphyr) can replace the standard of care (SOC) for something called cytogenetics.

Cytogenetics is a broad term for studying changes in chromosomes. Chromosomes are long strands of DNA. Right now, if you want to detect changes in chromosomes, you have to use pretty old techniques like karyotyping, FISH and microarrays.

What about the sequencing platforms, like those from Illumina and Pacific Biosciences? It turns out that those platforms are not so good at reading long-strands of DNA like you need to do for cytogenetics. The Illumina platform isn’t really cut out for it and while the Pacific Biosciences platform does read long-strands better, it is not good enough for cytogenetics. If you do a search through the filings of Pacific Biosciences for cytogenetics you don’t even get one hit.

The Saphyr platform does work. It uses a different technology, called optical mapping, to capture the DNA sequence.

Saphyr can detect large-length differences in the DNA, which are also called structural abnormalities (these have the short-hand SV for some reason).

These SVs aren’t important for detecting the genetic markings of most diseases. But they are important for detection of some. Bionano got its start selling Saphyr and its predecessor system called Irys to labs investigating rare pediatric diseases where there was a need to detect SVs.

The problem with that focus is that these diseases are rare so they are not much of a market. But this year a number of studies have been published that have presented data showing that Saphyr is good for other, more common diseases – specifically some types of cancer – that are characterized by SVs and where right now microarrays, FISH and karyotyping are used to detect the genetic anomalies.

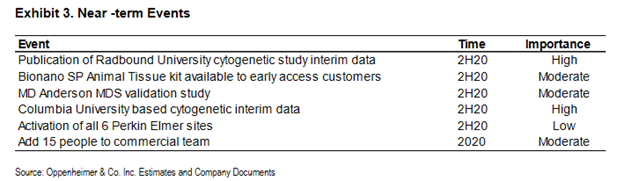

At the beginning of this year Oppenheimer initiated coverage of Bionano. In that report they gave this handy little table of the expected events of 2020. Included were a number of studies that would determine whether Saphyr would make it or break it as a replacement for SOC.

Now flash forward to today. The three studies noted in the table have been presented. In addition there is at least one more positive readout. In all the literature released this year, Saphyr looks to be a better solution.

Its faster (5 days versus 3 weeks). Its cheaper. It finds all the anomalies of the existing tech and in some cases is finding anomalies that the existing tech did not.

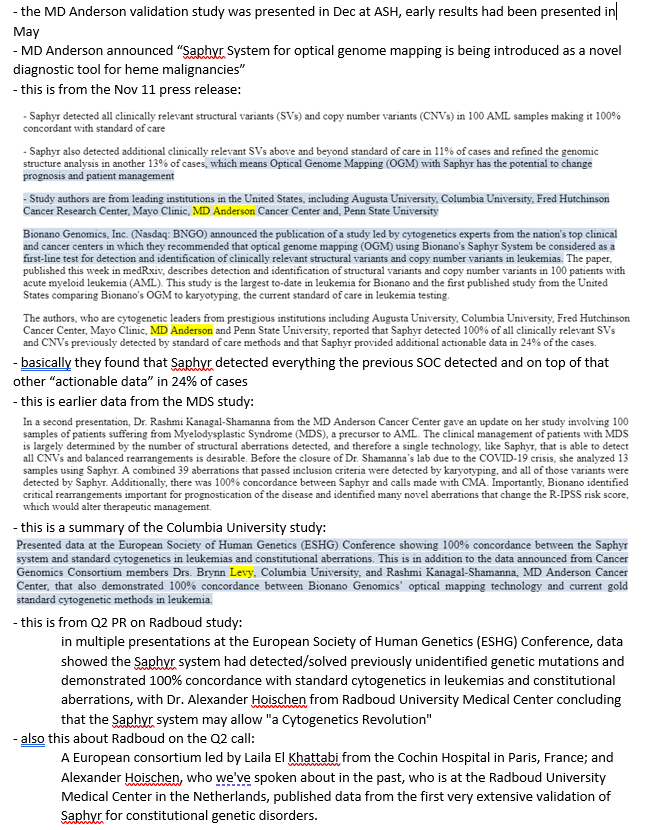

Here’s my summary of the studies that have been presented this year:

The next step, which Oppenheimer noted Monday, is the “pending publication of KOL recommendation of optical mapping to replace traditional cytogenetics tools in a peer-reviewed journal”.

Now some perspective. Bionano is not the next Illumina or Pacific Biosciences. The TAM of cytogenetics is $200-$400 million. Recurring consumable revenue at ~70% gross margins.

If Saphyr becomes SOC for these tests, Bionano is going to capture their fair share of that TAM. And that should make the stock worth more than it is right now.

The question is if there are more applications. I think so, but I’m still trying to figure it out. I did notice that the Radboud study mentioned above describes Saphyr as alternative for “reproductive disorders”:

The study authors describe Saphyr as a viable alternative to both karyotyping and CNV-microarray, especially in reproductive disorders as a potential replacement of karyotyping as the primary cytogenetic testing method. Sequencing-based methods have failed to replace karyotyping, especially in prenatal testing, because of a high incidence of false positive findings, which has not occurred with Saphyr.

That reminds me of Combimatrix, which used micro-arrays for just this sort of test. So that is another potential addressable market for the technology.

So this is a story about a platform that is maybe coming of age. But I also cannot ignore the other angle – which is investor exuberance. You saw that yesterday with the move that far exceeded the news that underlay it. Along these lines, the Ark guys are at least aware of Bionano. Simon Barnett, who is a Genomics Analyst with ArkInvest, has been asked about Bionano a few times. His responses seem to be that he likes the technology, but believes it has limited opportunities. For example:

It is worth keeping an eye on whether Barnett and Ark, which seems to have some responsibility for the rise of small biotech names this year, might be willing reevaluate Bionano given if the role of the platform expands to SOC for cytogenetics.

The other piece, which is silly but still can’t be ignored, is that the market is simply crazy right now. Stocks in the right space are being bid up to ridiculous heights. I’m making the most money from the dumbest ideas.

So here you have a company that is in the right space – genomics – and there is a whole heap load of positive data that has come out this year that expands the application of their technology to a wider range of diseases. You just have to wonder if the market might keep bidding it up even if the opportunity is admittedly limited and this is a niche player.

Bionano has 148 million shares outstanding. There are another 30 million warrants. Most of those are quite far out of the money. The company did do a very dilutive financing with 33c warrants in April but I think most of those warrants have been exercised. I am triangulating a little based on the pre and post offering disclosures but I would guess about 5 million of those low priced warrants are still out there at most.