Research: Renalytix

- $82mm of cash

- no debt

- 72mm shares outstanding at $22/2 for $792mm market cap – or 36mm shares – its actually an ADR where 1 ADR is 2 shares of the common

- They hardly seem to be covered by anyone – Stifel and that’s it?

- KidneyIntelX is their diagnostic tool/platform

- tool for the management of Chronic Kidney Disease

- currently rolling-out across the Mount Sinai hospital system

- incorporates machine learning algorithm for in vitro diagnostics

- early-stage prognosis of kidney disease

- tool has been able to identify patients that are at high or low risk of rapid disease progression in the early stages of CKD

- that means you can provide better care earlier

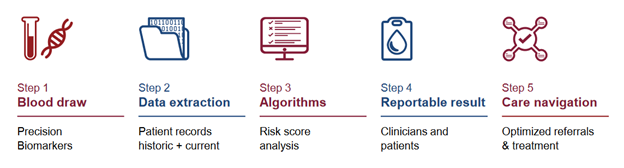

- here are the basics of how it works:

- do a blood draw

- look for 3 circulating proteins

- incorporate features out of the patients EMR

- takes this info and put into ML algorithm and it generates a prognostic

- graphically how it works:

- pursuing both FDA regulated pathway and reimbursement pathway

- they can test in all 50 states

- expect FDA clearance in 2021

- price for diagnostic set by medicare, $950/result

- launch partner is Mount Sinai Disease Network – very large group

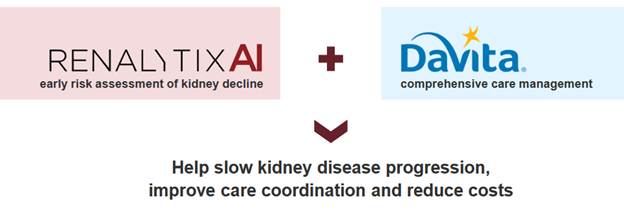

- have partnership with Davita

- partnership announced Jan 5/21

- RNLX KidneyIntelX assay will be used to stratify patients into risk groups

- Mid/high risk patients will receive care from Davita

- will launch in 3 markets this year

- Davita has 200,000 dialysis patients, relationships with 2,800 outpatient dialysis centers

- In August they announced partnership with AstraZeneca

- AstraZeneca will use the test to optimize the use of multiple therapies for Diabetic Kidney Disease (DKD) and Chronic Kidney Disease (CKD) management

- will use KidneyIntelX to help optimize therapeutics under current standard care protocols.

- SGLT2 inhibitor Farxiga, anemia drug Roxadustat, Lokelma

- This is just first stage

- before that, in June, they had announced a partnership with a top-10 global pharma company

- their TAM based on diabetic kidney disease is $12b – based on 12-13mm patients with Stage 1-3 diabetic kidney disease

- plan then is to expand the label to CKD – another 37mm people in the US

- expand outside the US in 2023

- Worldwide there is 850mm people (really?) with CKD

- Costs the US $120b annually to deal with them

- so this is a big TAM and I think that’s the story here, especially since they don’t have a lot of competition

- estimate 50-60% of patients have Medicare or Medicare Advantage

- doesn’t sound like there is any competition – see a few places that mention there is no one else developing a risk stratification tool for kidney disease

- new medicare rules are disruptive – they can get medicare coverage off their FDA clearance, this is significant event, pathway for emerging diagnostic companies

- they are going to benefit from this recent change in Medicare because they have received BDD:

- Medicare Coverage of Innovative Technology (MCIT), which automatically issues a national coverage determination (NCD) and Medicare coverage for four years for any device or diagnostic test that had received a breakthrough device designation (BDD)

- I think* this is why the stock popped early January, before this decision it was mid-2021 till you knew about the medicare reimbursement, but now it’s a done deal

- Just need FDA clearance, they submitted for this in August

- So they will have commercial rollout in 2021

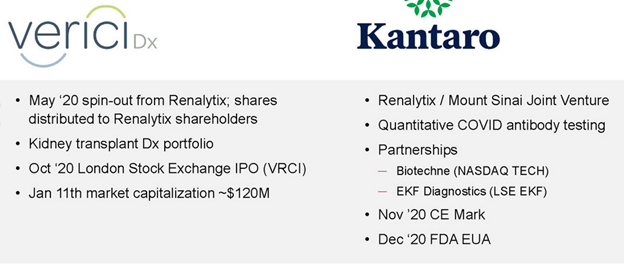

- they owned a piece of a company called Verici that they spun-out, still have 25% stake in another company called Kantaro – not sure what this is worth?

This one looks pretty good to me, even in a market that leaves me skittish.

13 Comments

Post a comment

This sounds impressive.

On Thu, Jan 21, 2021, 8:08 PM Reminiscences of a Stockblogger, wrote:

> Lsigurd posted: ” $82mm of cashno debt72mm shares outstanding at $22/2 for > $792mm market cap – or 36mm shares – its actually an ADR where 1 ADR is 2 > shares of the commonThey hardly seem to be covered by anyone – Stifel and > that’s it?KidneyIntelX is their diagnostic tool/p” >

Hey Lsigurd, love readying your blog post and your anylisis. Just wanted to check on your opinion regarding the big surge CLBS had due to the phase 2b trials?

I sold it on the pop. My strategy with these names right now is to find stocks that seem to have catalysts, and then just wait for the events like that. When you get a crazy move, I mean CLBS was like a 3-bagger over night, and when the news is not really a game changer, I just take the gains and move on. Its the same story for a number of the other tiny biotechs I’ve mentioned. Each may or may not pop like that but if they do I’ll sell into it. In addition to the names I’ve already mentioned, I’m thinking ZSAN and MLND maybe fit the mold right now. Also FLDM is kinda in that vein though it looks actually more interesting longer-term to me.

More generally, you are seeing it all over – I mean OBSV popped from $2 to $4 overnight. ITRM was up I think 40-50% one day. I mean its dumb, to pick stocks that you think may be the next runner, but right now this market is dumb and that is one thing that seems to be working.

And I am keeping a close eye on when it feels like this is ending, because it can’t go on, you see these micro-cap bios raising lots of money and eventually the supply is going to overwhelm the demand. I think you have to be aware that most of these bios are only worth what someone is willing to pay, they aren’t intrinsically worth X amt because most of the time any revenue is highly uncertain and a long way off.

One other thing worth mentioning. You saw how CLBS took advantage of it with an offering. At least it wasn’t at too bad of a price considering where the stock has been. But it goes to show how you have to be careful because these names are little dilution machines. Case and point is this BXRX I was looking at. Check out the offering they did in Dec and then the warrant conversion deal they did just recently. It’s crazy.

Definetly you are right in the statement that the current situation of the market isn’t rational nor logical at all… This is why also I am trying to build up something like what you are saying: stocks with a good catalyst that pops out and sell. However it is not my style of investment and to be honest I am not a great stock picker for this kind of strategy.

As I said, is great to read from your opinion and incorporate parts of your best practice into my style!

For sure. And I mean, the fundamental thing I am doing is looking for biotechs trading at either a small premium to cash or even less than cash but that have a legitimate platform or molecule they are developing with some near-ish term catalysts. If I have to hold those for a year to play out, that’s fine. But if the market is going to be crazy and give me 3 or 4 baggers overnight on nothing I feel like I have to take that certainty rather than speculative on some bigger possible prize down the road.

What do you think of new variants of virus spreading rapidly? Non event at this point?

Both African and UK mutations are likely far more contagious and possibly more deadly as well according to latest research. And vaccines are less effective while requiring a greater coverage now to be effective. And progress on administering them is rather slow.

I don’t know, I remember saying to someone back in June that it looked like the market was inversely correlated to COVID and I have kinda went with that since. I even thought we might see a slowdown in the market as vaccinations increase but probably that $2k is negating that. So I don’t know, as long as the gov’t keeps coming in with more money I’m not sure these strains matter much. Probably the bigger thing to me is that regardless of where covid is, every bubble does burst at some point. Thoughts?

Yeah sounds about right. I don’t see a bubble in the stocks Im interested in though. It seems to be mostly in certain segments of the market.

As for an interesting pharma stock, take a look at Lexagene. Testing machine with accuracy of PCR, at a lower cost (machine costing $20-25k and test costing $5-10), results within 15min-1hour. ability to test for 27 different pathogens at same time, test concentration amount, and quickly add new pathogens to test for. Sort of same thing Genmark has, except better and far cheaper. I got a small speculative position.

This is really interesting. Optimizing the “risk score” calculation is really important for Medicare Advantage – it determines the level of capitated payment that the government pays to the MA provider. More and more people are shifting from Medicare to Medicare Advantage, and this shift actually accelerated during COVID, which ought to increase the importance of risk stratifying tools like this. Honestly think coverage is a no-brainer either way, but really interesting about the change to reimbursement.

I’m sure DaVita would love this too – could drive more people into dialysis earlier and increase their payments.

Also interesting – the CEO and CCO previously started ExosomeDx, which got acquired by Biotechne, with a really similar concept for risk-stratifying patients with a mildly elevated PSA to optimize need for Prostate Biopsy. The buyout was for $550 million, with a TAM similar at 20 million men at risk for prostate cancer, but the company was at an earlier stage. The product ultimately got breakthrough diagnostic designation in 2019 and Medicare coverage. Pricing was bit lower at $760/test. May be a reasonable comp to suggest current market cap is justified.

You don’t think there’s much upside then?

No I didn’t mean that! Sorry I wasn’t clear. I meant that the valuation of Exosome would mean the downside from here might be limited.

Renalytix has a higher price point ($950 vs $760), later stage (already has breakthrough designation), and actually, you might argue the TAM is larger when you look at the total CKD market. Plus, the markets were much less forgiving for biotech back in 2018 when Exosome was bought out.

I think post-approval it’d be worth at least $1-1.5 billion for the right buyer and I could easily see a $2.0 billion+ market cap on approval in today’s frothy market.

At a 20% penetration of the diabetic CKD market you’re looking at $2.3 billion in revenue at peak, and a 3-4X peak sales valuation gives you something like $7-9 billion in peak value. Let’s say time to peak is 6 years and a discount rate of 12% – would imply a valuation around $3.5 billion post-approval.

oh ok got it thanks. I have the Stifel report if you want. Just email me.