Stelco, Algoma and Carbon

It is a little hard to write about the commodity investments I am making. Because I am just not sure yet – about the short term.

The long-term trend to me is clear – and it is all about carbon. But whether this is the right time to be buying some of these names – I have less confidence in that.

Right now I own some copper, some tin, some steel and a few shipping stocks. All of these names have had big runs already, and they have all pulled back. But most are way above their historic levels, and so they could pull back a lot more.

So I am more cautious than bullish right now.

But at the same time, these stocks are trading at extremely cheap multiples if you think that the price of the underlying commodity can hold these levels.

I bought Atico Mining a few weeks ago – it is at around 2x cash flow with copper that this level.

Or take the shipping stocks I own. Euroseas 2022 EPS is projected at $6.50 per share – the stock is ~$15. Navios Maritime Partners 2022 EPS is projected at $11.45 next year. The stock is ~$26.

And yes, I know, commodity stocks are to be sold when the multiple is low. And yes, with respect to shipping, management will inevitably destroy any shareholder value they create during the cycle, so even more buyer-beware there. Nevertheless, as I’ve been posting on IV, there are reasons to see the glass half full.

Steel is another sector with crazy low multiples if you believe in anything close to current prices are sustainable (current prices are a little more than 2x their average over the last 3 years).

On their first quarter call Stelco put the following statement on one of their slides:

On the call Stelco management said that if they generated $2 billion of EBITDA, that will convert to $1.4 billion of free cash. Stelco has an EV of about $2.9 billion right now.

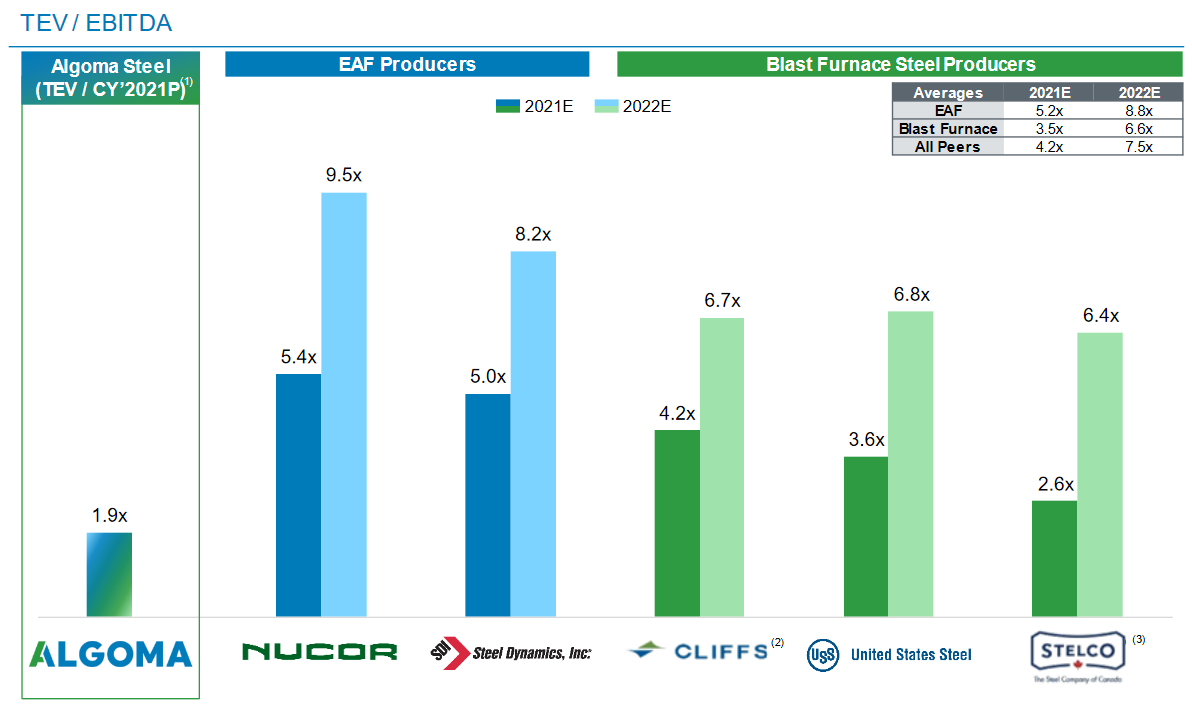

I thought wow, you can’t get much cheaper than that can you? Well, it turns out that you can at least come close. Last week Algoma Steel decided to go public via a SPAC deal with Legato Merger Corp.

The combined company will have at EV of $1.7 billion, which includes cash of about $300 million and net debt of $200 million.

Algoma expect $900 million of EBITDA this year with the assumption of $1,250/t steel. Stelco’s was based on the H2 forward curve, which was at $1,500/t. So I think that Algoma is actually a little cheaper than Stelco if you were using apples to apples pricing.

Algoma is also getting a cash injection that they plan to use to build out an EAF furnace. EAF steel makers use scrap instead of iron pellets and coking coal to make steel. They trade at larger multiples – Nucor, the biggest EAF steel producer in North America, gets a crazy 8x PE multiple!

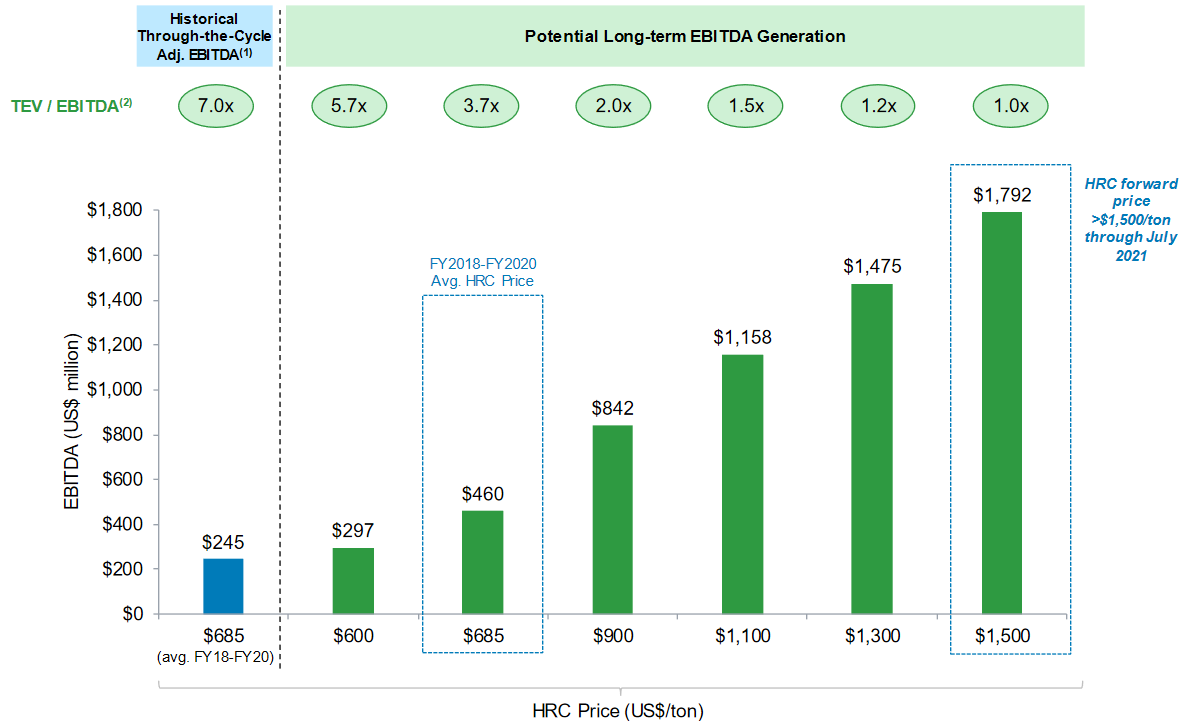

When Algoma finishes their EAF conversion they will be producing 3 million tonnes of steel (versus ~2.4 million tonnes now) and they will be doing it more cheaply. Algoma gave estimates of what their EBITDA multiple post-EAF conversion would look like at various steel prices:

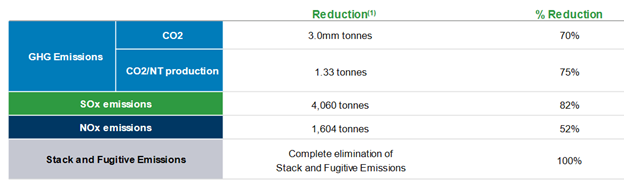

But Algoma told us something else about their EAF conversion that in my opinion is even more important than how profitable they could be was it is done.

They told us how much carbon will be reduced.

I am not sure of very much yet with this commodity cycle but the one thing I am convinced of is that it is going to be driven by carbon. The changes we are going to make over the next 10 years are going to be massive. And they are going to have an equally massive impacts on commodities, both good and bad.

Look at what Algoma is saying. They plan to reduce their carbon emissions by 70%, by 3 million tonnes, by converting to an EAF.

But you might say – so what? Well, in 2030 we are likely in a world of $150 per tonne carbon. $100 per tonne is guaranteed. Those 3 million tonnes are worth $300 million to $450 million a year.

So what happens to those Chinese steel producers, those that are far higher carbon emitters than Algoma? I am convinced that the EU is going to put up carbon tariffs at some point. The US and the rest of the west will eventually follow. They won’t have a market.

The Chinese are not making overtures about shutting down steel mills by the end of this year because they are altruistic. They see the writing on the wall. Those mills are going down one way or another. They go from low-cost producer to uncompetitive in a world where carbon is priced accordingly.

So I’m not sure what the price of steel is going to be next year. Probably lower than it is now. Same with copper, same with container ship pricing. But I am getting more sure that in the long run some of these commodities are going maintain the levels that we are seeing and maybe even go higher. In fact its possible that the market, which has run up these commodities to heights that I don’t think anyone expected, is telling us just that. Because pricing carbon changes everything.

Thanks for the Algoma idea, looks very interesting. Why are they selling those shares so cheaply? They are lower cost producer, don’t have much debt, why not do an IPO? Or why not sell out for a higher valuation in this SPAC deal?

What is stopping other mills from doing these EAF conversions and possibly driving up scrap prices?

Here is what they said:

“So the SPAC afforded us a few advantages. One was speed to market. Second was the flexibility to talk to the private investors that are part of this process and talk a little bit more speculatively about what could happen, what we could do in particular the potential for an EAF. So it allowed us to be a little more forthcoming with respect to perspective plans.”

They also said the SPAC gives them the cash they need for the conversion. Maybe they didn’t think they could raise $300mm in an IPO, not sure.

There are other conversions happening. X for example. Part of the Stelco case is that they aren’t an EAF producer and they think scrap is going to tighten just like you are thinking:

Prospective customers have taken note of our capabilities and our thesis, and we are engaged in ongoing discussions. Related to this point, last quarter, Paul and I shared with you part of our thesis related to the impact of scrap pricing on our EAF competitors. As we look forward at the projected price of busheling scrap, it continues to be higher than the implied cost of our blended product mix by a substantial margin. I will ask Paul to again share the details with you, but we view this as a significant competitive advantage considering our significantly lower exposure to scrap than our EAF counterparts.

As the EAF market continues to compete over the tight domestic supply of scrap as well as competing with China, we see significant opportunity to exploit both our low-cost position and our new pig caster to provide high-value iron units when the market conditions are right.

To me its all about trying to navigate this. Its about there being dislocations, both positive and negative, by carbon driven decisions. These EAFs are a good example of that.

I recently read that there’s another reason why China shut down some steel production this year: a power shortage due to drought (less hydro power). I thought I’d add that to your excellent steel/carbon discussion.

“Most of China’s electricity is produced from coal, but domestic coal production is increasingly struggling to keep up – the result of regulatory reforms, under-investment and more stringent HSE inspections. Another important source of electricity generation in China is hydropower, but because of droughts in key parts of the country, hydropower has failed to grow this year too. Over the summer, this led to power crunches that forced regional governments to curtail consumption.” (Morgan Stanley)

Yeah I’m seeing this too. It seems like a big impact is coming from local gov’ts pulling back on power supply to meet their carbon targets