LGFVs

Markets look to be up for the second day straight. Crisis over?

Fintwit thinks so – the mocking of the Evergrande posse is well underway. The VIX is almost back to where it started. I listened to the first 10 minutes of Cramer last night and he said that the moves by Xi took the Evergrande worry “off the table”.

me? Well, I’m going to keep my cautious stance a little longer, even as right now it is wrong.

I read a thread from Hugh Hendry last night. It was – as always – cryptic.

But I get about half way through and Hendry mentions this:

And I’m like – wait, what?

So… I do not profess to know much, but one thing I know is that $8.4t is a lot of money.

It caught my attention. So I start digging.

This is primarily going to be a cut and paste excerpts/charts from FT. Please don’t forward because FT doesn’t like people using excerpts and I don’t want to get in trouble.

My take, which is evolving, is that Evergrande is kinda a sideshow here. Maybe a better description would be a symptom. But there is an underlying ailment that seems to be gaining steam and I’m not all that sure how that plays out.

Start with the basics. Property prices in China have gone up a lot, much like the rest of the world:

Today, China has a lot of unsold housing inventory:

On top of that unsold inventory, China has another 90mm of empty property:

China seems to recognize this has become a problem. In addition to all the usual consequences of a property bubble, China has the additional issue that their 1-child policy means a smaller population in about 10 years. I think the government realizes they have to deal with this now before it gets even more out of hand in 10 years.

China is unquestionably squeezing developers to try to reduce the investment made in new properties. China drafted rules in the summer of 2020 – so not that long ago – that constrained how much leverage developer could take on.

They called this 3 red lines. It limited borrowing to developers/financials based on ceilings they apply to 3 metrics: debt to cash, debt to equity and debt to assets.

One detail of this that I got from a Youtube video is that China gave developers 3 years to comply with these limits. The Youtuber pointed out this implied that many developers were likely far over these limits right now.

Not surprisingly Evergrande stock began to slip at around that same time. And financing to developers has gone negative the last 12 months.

But developers and Evergrande aren’t the headliner here. They are like the cog in the gear system that is stuck. The engine seems to come from the regional and local governments (more on that in a second) and that could be a problem. It has to do with the end-source of the financing new infrastructure development in China.

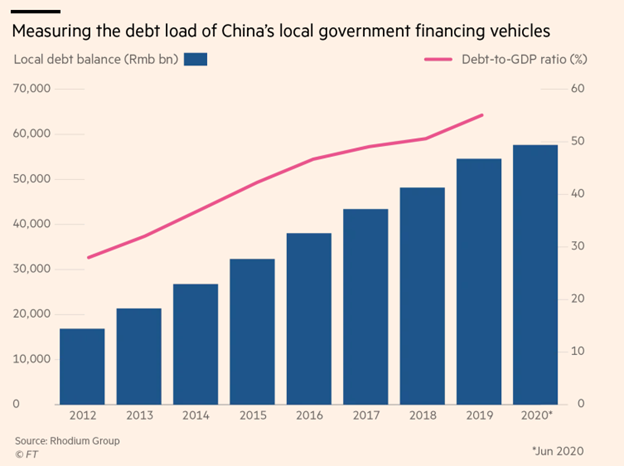

So…. there are these sources of capital for Chinese local and regional governments called local government financing vehicles (LGFVs).

LGFVs are an off-balance sheet way for local governments in China to raise money. The money they raise is mostly used to fund infrastructure (ie. what you need for property development). FT calls them the “main lenders behind China’s infrastructure building boom”.

Why do local and regional governments use these “vehicles”? To get around the limits put to local government borrowing. They are “off-balance sheet” so they mean a government can lend without looking like its lending.

Way back in 2019, so before Evergrande was on anybody’s radar, China “hit the brakes” on LGFVs, saying they could only refinance existing debt in the second half of the year.

But then Covid hit and the brakes came off.

Now the brakes are on again. And not surprisingly, Evergrande and other developers that depend on development (and thus LGFVs) are back on a downward path.

So LGFVs fund infrastructure and infrastructure is a big part of China’s economy. 43% of GDP was fixed asset investment last year.

Here’s the thing about the LGFVs. They have a shitload of debt. And I mean a shitload. Here is where Hendry almost assuredly got his number from:

$60t Renminbi of debt is over $8t USD. That is real money.

And here is, IMO, the big reveal:

Hmmm – that sounds an awful lot like the “house prices don’t have to go down, they just have to stop going up so fast” argument of the Great Financial Crisis.

So there is all this debt outstanding at the local and regional levels. It is kept afloat by land sales. But land sales are collapsing because the big developers like Evergrande have been squeezed and are in trouble.

I don’t know… I’m not smart enough to say how this plays out. But I am cautious enough to think there is somthing more tectonic at play than a property developer going bust.

Very thought provoking. Thanks for sharing!

Yeah I decreased my commodity exposure. Housing starts of 15mn is not sustainable. Evergrande made me dig into the whole China real estate situation as well.

Although I think one thing people are missing is that a lot of real estate in China was built before 2000. So new housing starts were about 220m total in the past 2 decades. With 450-500mn households, and a lot of people still living in what is basically third world housing with public wash and bath rooms, there is a lot of room for excess building still. This also inflates the the number of square meters, when a lot of these square meters were built in a period when GDP was <$1 trillion a year and are close to worthless anyway in a write off.

And China has a GDP per capita of $10k, which is 1/3 of OECD average. While Spain's bubble got popped close to OECD average and Japan's got popped when it was greater than OECD average. Unless there is a structural reason China should not further catch up, they can basically normalize a lot of this stuff and grow out of it by chugging along 3-5% a year for a decade while keeping their housing situation stable.

Still though, normalized housing starts should probably be about 4-5mn a year, and it is 10-15mn a year in the past decade. So plenty of room for a large correction. The question is when. If another 100mn legacy housing units are replaced, it might mean the current situation continues for another 5 years.

And current short term figures might also be distorted by Covid outbreaks, givne that Sinovac doesn't protect so well against Delta variant.

Thanks for sharing that data.