Some Things are Working, so I’m getting Nervous

The shipping trade is working. It’s working!

So I am selling. Not completely, but I pared down a bit (because, after all, this is shipping).

But…. even though the move last week was really good (especially for Euroseas) I am reluctant to take all my money and run after one big week.

My reason? The set-up just seems so darn bullish. Everything I read points to a tighter market in the months ahead. There are 300 containerships trying to dock around the world that are just sitting there waiting. There is an orderbook of containerships and bulkers that won’t deliver material new ships for 2 years minimum. The drybulk order book seems particularly thin. There are environmental regulations on the horizon that are making shipowners think twice about ordering multi-million dollar fossil fueled propulsioned ships that could be deemed obsolete in a few years. There are sky-high rates going into seasonal strength. And now there is COVID at a big Chinese port that has backed things up in China to even worse conditions than the already bad ones they were in. I mean, yeesh.

I subscribed to J. Mintzmyers SeekingAlpha platform a couple months ago, when I thought there might be something to this whole shipping trade. I’m not going to share all of what he says or the research he provides because the subscription is a lot and I don’t want to get into trouble.

But I think I can safely give my conclusions. I have listened to all the post-Q1 interviews that Mintzmyer has done with shipping companies and they are unequivocally bullish. There is just so much running in favor of containerships and dry bulk right now. And I said this in my last post: that even though it is the containership market that is strongest right now, I have a feeling that it will be the dry bulk market that actually does the best in the longer run.

So I am going to stick this one for a while yet. These markets seem destined to get tighter, which could make the stocks go up even more.

Flip-flop on Biotechs

A little over a month ago I sold pretty much all of my biotechs. It was like a mini biotech-centric version of one the portfolio purges that I do from time to time. I stayed out of all my biotech names for about a week or so. And then I bought them back and then some – at pretty much the same prices I sold them at. You can see this in the portfolio page – Lyra’s average cost, for example, went from $10 to $7. That wasn’t magic, it was just me selling, and then thinking better of it.

Why I sold is clear – it was not working. But why did I buy back? During that week I held no biotechs, the stocks did nothing. But they also did nothing. Which is to say, they stopped going down.

I watched Lyra for 5 days, without any skin in the game. Those days are circled in green.

During that time the stock felt like it just did not want to go down any more. I had been watching the stock since December and the intraday action was different than it was during the March to May period when the stock fell and fell and fell.

But it was not just Lyra. A number of the Biotech stocks that I track were following the same pattern. It made me go hmmm. And that led me to buy back Lyra, and add two other names.

I added Zosana Pharma and Clearpoint Neuro. I am not going to talk about Clearpoint because everyone talks about Clearpoint and I am just renting here, not owning.

As for Zosana, I owned Zosana briefly in February when biotech stocks were doing those crazy pre-market gap-ups. For whatever reason, Zosana is one of those 2nd or 3rd tier momentum stocks – not with the consistent momo of a GameStop or AMC, but a stock that every so often catches fire and runs up. If you can catch that, you can do okay on it.

But Zosana is not just a do-nothing shitco. Well, I guess it kind of is, but not completely. They do have something that may be worth something someday. Maybe.

Zosana has been going through clinical trial for a transdermal microneedle form of a drug called zomitriptan.

Zolmitriptan is used in acute migraines. Zolmitriptan is one of most potent triptans. The triptan market is big – $4.8b market overall. The standard delivery for zolmitrptan is oral, injectable, or nasal. Non-orals represent $650mm of the market. Zosana is offering a different delivery, through a patch. Indications from the trials are that it works better than the existing alternatives.

So Zosana has potentially a better vehicle. It is called Qtrypta. You put this little patch on and the drug is administered through your arm.

I got interested in Zosana a few months ago because the stock is very reasonable (the stock has a $100 million market cap and $17 million of cash), and the brokerage reports that I read seemed quite positive on the outlook.

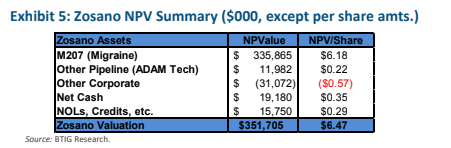

While I never know whether I can trust the research of HC Wainwright or BTIG, they at least paint a compelling upside if all goes according to plan. For example, BTIG gave the stock a $6.47 NAV in their initiation report:

Zosana’s problem is that the FDA did not approve the drug after Zosana completed their Phase 3 study. They gave them a complete response letter, or CRL, which is usually a letter saying no dice.

But in this case the letter just outlined a few issues that Zosana had to rectify before the FDA would approve the drug. They wanted clarification on safety data, and they wanted Zosana to repeat the bioequivalence study. It seems there are concerns that the drug levels administered to all the patients were not consistent.

While none of this is ideal, it is also not a death knell. In April, Zosana announced that they had met with the FDA and come up with an acceptable study to satisfy the concerns. They said “we believe that this study can be executed quickly and will address the last remaining clinical request from FDA regarding the resubmission of our NDA for Qtrypta”.

Ok, so great. They do the study, maybe they get approved, maybe they are successful at marketing their alternative delivery system, maybe the stock gets to the BTIG NAV. Maybe not.

I am not smart enough to be able to tell you how this all plays out in the next 1-3 years. But I can say that: A. the bad news is baked in, B. the news flow seems to have gone positive, C. the stock is one of these “jumpy” meme-esque kind on names in a market that is going meme-me again, and D. the stock chart is a lot like Lyra.

So…. worth a punt.

Eastside

Eastside Distilling has been a frustrating laggard up until just recently. I wrote about Eastside a couple of times last year. I took what is for me a pretty large position and watched the stock drastically underperform other microcaps through the end of last year and the beginning of this year.

It was painful. Apart from one short-lived run up at the beginning of February, Eastside languished at about the price that I bought it.

What was confounding was that Eastside seemed like such a perfect play for reopening. The stock was well below its pre-pandemic level (it was in the $1.50 range vs $3 per share a year before). Eastside had clearly suffered from restaurant and bar closures and that would be changing shortly. And… at a corporate level the company was in far better condition that it was a year earlier. The new management team had a plan, they were clearly focused on driving cash and not just running up revenue and losses.

Yet the stock did pretty much nothing.

That has changed in the last few weeks.

The stock began to rise shortly after the company announced Q1 results. While those results were nothing particularly amazing, they were another step in the right direction. So who knows, maybe management talked to some fund, maybe there is a brokerage report that I don’t know about? Someone is buying the stock.

What I do know is that the new management at Eastside has done an admirable job of reducing costs, selling off unprofitable product lines, monetizing inventory, reducing cash burn and just generally turning the business around.

The two numbers that highlight the turnaround are that. year-over-year, gross profit was up 25% and opEx was down 17%. Management has really focused on selling spirits that have better gross margins while dialing back their marketing and G&A expense. No surprise that leads to a more profitable business.

Having said all these positives, I am starting to take some of my position off here. It has been a good run and while I can envision how this could be a $5 or $10 stock some day, it is going to take time I think and god only knows what the bumps in the road will be.

But beware! This has been my Achilles heel. Over the last 9 or so months I have been burnt by taking profits. I have taken profits on soooo many stocks that have gone much higher. Kopin, Silvergate, Inspired Entertainment, Identiv, Beam Global, Prothena, Bionano, Foresight and on and on – it’s ridiculous when you think of all the stocks that have been doubles or even multi-baggers after I sold out.

I have treated all these tiny little microcap speculations the same way I always do – when they go up enough, start selling (while you can). In the past, that has been the prudent strategy. Over the last 12 months, it has meant leaving a lot of money on the table.

But what can you do? You gotta stick to your playbook.

Tornado

Speaking of moonshots, and one that I have not sold: I have no idea why Tornado Hydrovacs is going up.

This is one of those stocks that I have owned forever. It was a spinout of Empire Industries, and while I gave up on Empire (now Dynamic Technologies) a while ago, I have stuck with Tornado.

Tornado makes hydrovacs. They operate out of Alberta. Right before Covid they bought a large facility in Red Deer to expand their production. Everything seemed to be on-track. But…

Obviously, since Covid the results have been pretty meh. As of Q1, they had not turned around just yet. In the press release of their Q1 report Tornado said “production at the facility located in Stettler, Alberta was reduced by approximately 60% for the second half of 2020 and 20% for Q1/2021. As at March 31, 2021, approximately 25% of the Company’s employees had been permanently laid off.”

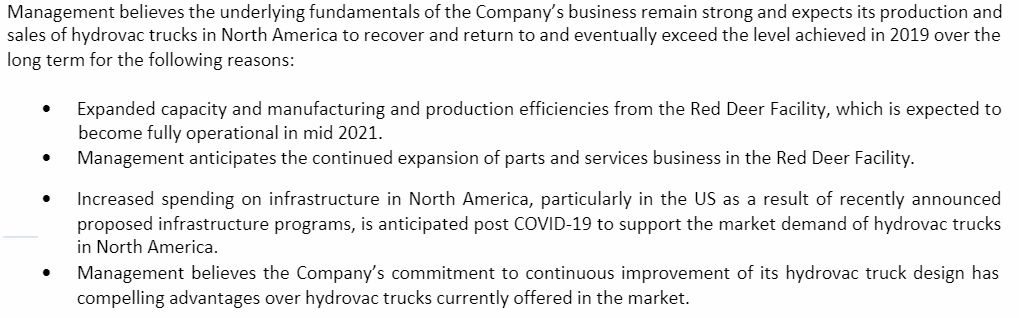

Tornado did make a reasonably positive outlook statement in their Q1 MD&A:

I can kinda get that this stock should do well over the next couple of years. It should benefit from the increased infrastructure spending and such. And that is really why I have held it. But based on the available information, I am not quite sure why its run up like this over the last couple weeks.

Two more thoughts/ideas and then I will be done.

Vertex and Vidler

First, I bought Vertex Energy, a stock I have owned previously, when they announced the acquisition of a refinery from Shell. Hat tip to Glen who compelled me to look at the news after I was so skeptical about it that I ignored it for a day even as the stock went up 100%. I don’t really have much more to say about this one because honestly, I just don’t know. Vertex made a very cheap refinery purchase that they say they can transform them into a biodiesel powerhouse. If they can make good on this, the stock is only getting started. But because I don’t really know, I already sold half. I would probably sell the rest on a move to $12+.

Second, I bought a company called Vidler Water Resources. Vidler owns and develops water assets. I am still pretty early into the name and so I’m still trying to figure out all the details, but the big picture looks good.

Vidler owns water rights and water credits in Nevada, Arizona and Colorado. There is a big water problem brewing in these states. Lake Mead, which is the Hoover Dam lake, is drying up. If you google search Lake Mead you can read about a dozen articles describing how bad its getting and how rationing will be in store this year.

So Vidler is in the right place at the right time. What I haven’t yet worked out is how much they will benefit from the increasingly desperate search for water, it seems pretty clear that they will benefit and the stock does not appear that expensive.

I got the Vidler idea from mrmojorisinX on twitter. He is a smart hedge fund guy that makes very hard to understand tweets that never name names but where if you are enterprising enough to decode what he is saying you can sometimes get very good ideas from. This looks like one of them to me so far.

Gold Stocks

Finally, last thing, gold. So… I’m doing pretty well on my gold names, but that doesn’t really have much to do with gold. It is really to say that I am doing pretty well on Wesdome. Wesdome has been great because the results at Kiena have been tremendous and the stock is going up even as gold is going nowhere.

But that brings me to my larger point. I’m not quite sure what to make of gold stocks right now. They are… strong. That is not a word you associate with gold stocks 95% of the time. But gold stocks are surprisingly strong given that gold is not.

I’ve woken up about a half dozen mornings in the last 3 weeks, looked at the price of gold, looked at the sentiment on gold-twitter, and thought, “yup, this is the day the gold stocks are going to get creamed”.

And then it didn’t happen.

Even today, gold stocks opened down. But they haven’t stayed there.

If this was any other sector I would be saying, THIS IS A SIGN!. But with gold stocks, with whom I have battled with for years with which I am perennially disappointed when I overstay my welcome, I have zero trust in even the strongest signals and therefore I will say nothing except for – it is interesting.

What are your thoughts on a potential Taiwan invasion, and how to hedge against that? I think odds of this happening within the next few years are larger than most people think.

Oh man, I have no idea on that one.

Love the water play. I live out in the SW and it has not rained in a loooong time. Mix that with extremely robust population growth and there is a looming water crisis.

It is interesting that TSM is planning a $35B semi conductor facility in Phoenix – which requires a lot of water…

Another water play in the southwest is GWRS – a water utility located between Phoenix and Tucson Arizona. This corridor is quickly being developed and GWRS already has the hook ups, just needs the population growth, which is happening given affordable housing in Maricopa and build out of Nokila factory.

Thanks, I’ll check that out, definitely in the right spot by the looks of it.