What’s not Working

Those of you that have read this blog for a while will know that my posts mostly focus on the stocks that aren’t working.

If a stock is working, I rarely write about it. If a stock works off the get-go, I may not even mention it all.

Why is that?

It’s no fun writing about what’s going up. This is a private blog with a handful of readers so its not like I’m getting some sort of chest beating bravado by talking about a winner. I’m certainly not trying to procure subscribers. When I reread something I wrote about something that has gone up, I usually cringe.

It is far more interesting to talk about what isn’t working. And that is, in fact, where I spend my time.

Again, if a stock is working I may not re-visit it for months. This is sometimes to my detriment as I have found that I can lose the thesis: in other words something changes even though the price doesn’t and I don’t realize it until its too late.

But there is only so much time in the day and it is better to spend it on what worries you the most.

What has worried me for the past couple months is biotech in general. But now that is right-siding for the most part. My worry now has become more dialed in. To a specific biotech. Eiger.

I already went through the story of what is going on with EIGR a few posts ago. I’m not going to rehash that.

But we are in June now, 3 weeks from July, and there is still no EUA and no real update for that matter.

A friend asked me whether I was concerned. In particular he asked me about this tweet:

Here was my response.

Yeah it is related to what I was saying. But its more nuanced than his tweet. I had to talk to some folks to understand this, but I think I have it straight now:

So EIGR owns peg-interferon lambda. It is not an approved product. If you want to do a trial using an unapproved product, like peg-interferon lambda, you have to get EIGR’s permission. This is different than if a drug is already approved for an indication. If it is approved, then you can just buy it and use it in the trial – the company doesn’t have a say.

In this case for whatever reason the TOGETHER doctors went to EIGR and asked for permission. EIGR said okay. Some agreement was reached.

But this isn’t EIGR’s trial. They don’t have anything to do with the trial itself, the data collection or the primary data analysis. They aren’t a sponsor. That is all on the TOGETHER doctors.

Yet while the TOGETHER doctors are responsible, at some point there is a data transfer to EIGR. We know this because on the Q1 CC EIGR said they would be the ones publishing a manuscript and they would be the one’s publishing the data. They are also the one’s doing the secondary analysis, so the more detailed breakdowns and such.

Unidentified Participant [6]

So also, I have one — just a clarify question to do the — this TOGETHER data will need to be published? Or do you need to just complete the analysis to submit to the Agency?

David Cory, Eiger BioPharmaceuticals, Inc. – President & CEO [7]

Ingrid?

Ingrid Choong, Eiger BioPharmaceuticals, Inc. – SVP, Clinical Development [8]

Thanks. Yes. So our plan is to complete the secondary analysis and submit all of it in totality to the FDA. Concurrent with that, we will submit a manuscript that will include all of the data as well.

When Boulware talks about how slow EIGR is, I don’t think he is understanding the above situation. One day before that tweet EIGR had their Q1 CC. On that CC EIGR said they were still waiting for the full dataset from the Together doctors. In fact, there is a tweet in that same thread below from one of the doctors confirming they have not finished the data set yet.

Its actually kind of interesting IMO since I love to think there are conspiracies. A bunch of guys on stocktwits are screaming that EIGR is too slow. Yes, its true, EIGR is slow in general. But in this case we don’t actually know. We don’t know when they got the data or for that matter even if they have the data right now (hopefully they have it by now though). I’m more than a little skeptical of some of the motives of these folks that are using this as a tool to bash EIGR management. But I’m always skeptical.

I was worried about how long the process was taking as well, but from another angle. I was worried the doctors hadn’t published anything yet.

I’m not as worried now. My misunderstanding was thinking that the TOGETHER doctors could publish something before the EUA came out. I had looked at the fluvoxamine arm of the TOGETHER trial and saw that it was about 2 months from last data collection to paper. We are way past that with lambda – its probably at 90 days or so. That had me worried.

But I’m not worried as much now because I think when EIGR signed an agreement with the TOGETHER doctors, they had the doctors agree to hand-off the process to EIGR at some point. So we won’t see anything come out until EIGR comes out with their EUA.

The real gotcha here IMO is the incentive misalignment. Think about it from the TOGETHER doctor side. They had to do this trial, compile the data, do all the primary analysis, but now they have to hand it off to someone else to do the fun stuff, write the paper, take the credit. I’m sure they’ll get their names on it but they aren’t in control of the process.

I suspect that is contributing to the time its taking. Its probably lower on their priority list than it was for fluvoxamine, where they got to write the paper, make the conclusions, present it at conferences.

I think my takeaway is that yes, its taking longer than I would have expected. And that may be saying something but it may not. Bottomline is that EIGR said end of June for a reason, and until it gets passed that date you have to assume its inline with their expectations.

There are other things to worry about with EIGR and COVID as well. One is whether the FDA is going to approve this. I’ve been talking with another Twitter contributor that has recently taken an interest in EIGR. His big worry is that the FDA won’t approve this regardless, because they will protect Pfizer profits.

I’m not sure what to say about this. There are certainly a number of biotech investors that think Novovax got hosed for this reason. That there are now myocarditis issues with the Novovax vaccine that the FDA just leaked are laughable to many given that the FDA approved Moderna, which had similar issues.

I spent some time looking at the Novovax data and I can see both sides. That is to say: I’m not convinced that the FDA isn’t in the pockets of Pfizer, and if that is the case it certainly could work against Eiger. Its a risk I think.

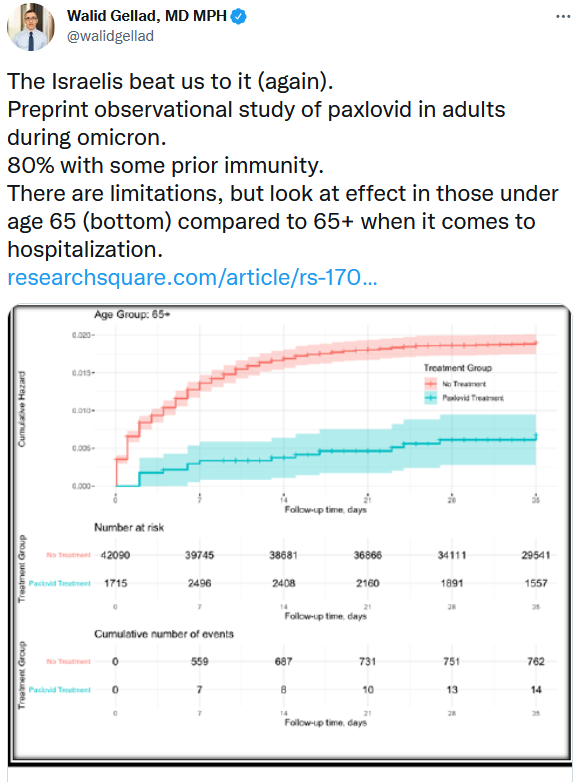

There is also the matter of a recent study from Israel which does show efficacy of Pfizers paxlovid in a largely vaccinated population:

Once you delve in to the study, it is kind of a good/bad story with a whole bunch of uncertainty. It does show very good efficacy against hospitalizations in 65+ (about the same as Lambda did overall in TOGETHER) but it doesn’t show any efficacy in younger people. That is interesting because in the US right now, as it was described by one biotech commentator, they are giving paxlovid out like candy.

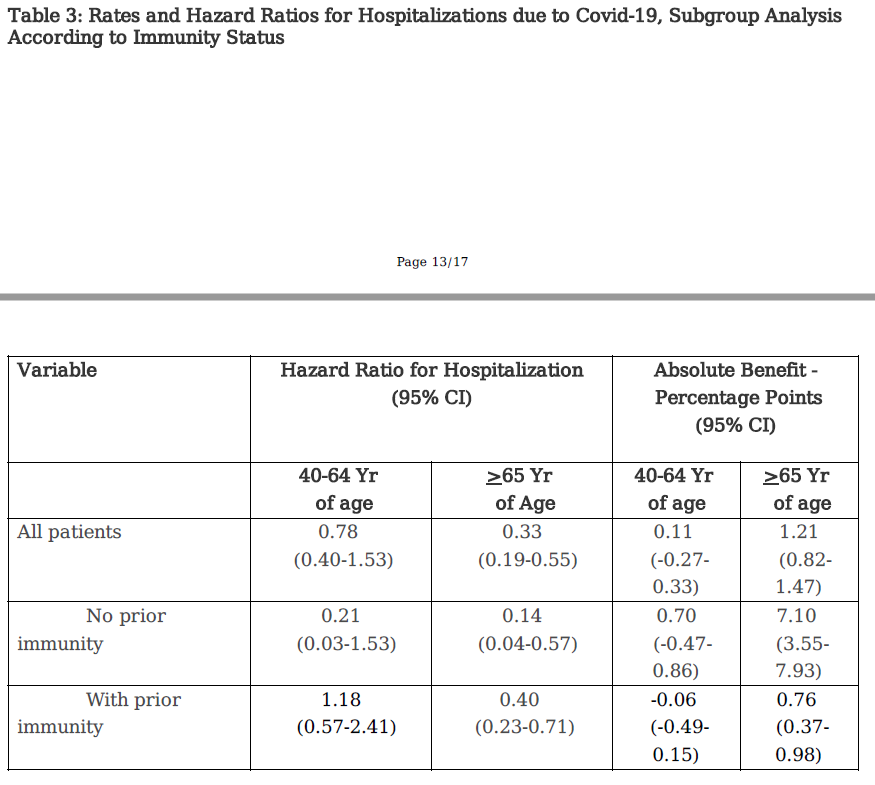

Even the 65+ cohort, results are a bit less positive if you dig deeper in the study (or the twitter thread!). In particular when you separate those that have been exposed versus those that have not.

You can see that even in the 65+ population, there is a big difference between the benefit of paxlovid in the prior immunity vs no prior immunity groups. If I understand absolute benefit correctly (and I might not) it is saying that for every 100 people that take paxlovid, you get 0.7 less hospitalizations from the prior immunity cohort, which doesn’t seem like that much benefit to me.

Absolute benefit also has issues. There are lots of papers that talk about them. Not the least of which is that it really depends on the baseline. And the Israeli trial is tricky there too. The cohort not taking paxlovid is massive – 42,000 people. The cohort taking paxlovid is much smaller – 2,504 people. Is this apples to apples?

Anyway I could go on and on. There is other things too but I’m not sure enough about them to write them up. Bottom-line, I don’t think this study is a negative for EIGR.

What is going to really matter for EIGR is how the lambda detailed data plays out. We know that the TOGETHER trial study showed lambda 3-day data is comparable to what we are seeing from paxlovid here and that included everyone, over 65, under 65, prior immunity or not. What we don’t know yet is how all that data breaks down on the lambda side. Is it just way better in the 65+ without prior exposure group like paxlovid? Or is its benefit more general? And what is the population comparison? Are these unhealthier people, or more healthy? We just don’t know any of that yet.

So where do I stand after considering all these (and some other) issues? Probably about the same place I did a month ago. I don’t see any evidence that the FDA will rescind the EUA process any time soon. There is too much worry about a fall wave with a new variant. I’m a little worried about the motives of FDA but not enough to sell. I’m not too worried about the Paxlovid competition – it isn’t really any better and it has lots of other issues, like the rebound effect that has been reported and all the drug interactions that make it hard to take for some people, but I’m also aware that until we have detailed data from lambda, we just don’t know enough to compare.

Lambda’s big positive is that it is a molecule that is in our body right now, and is used by our immune system to protect it against viruses coming in. In fact in people that don’t get COVID that bad, its probably lambda that contributes to that. It has been tested extensively already – its not an unknown like other drugs with worries about poorly understood side-effects.

Meawhile EIGR stock has been on a roller coaster. There isn’t a lot of volume but there are a bunch of big blocks that happen, which is unusual for EIGR and I don’t know what to make of it. Price wise it is back to pretty much where it was when I talked last time. $250 MC, $100 EV. It doesn’t take much in the way of lambda sales to generate that much cash.

But we’ll see. This is a gamble as are all biotechs. There are all kinds of possible unknown unknowns that could be gotcha’s. The downside is the EUA doesn’t happen, its probably a $3-4 stock again. I don’t think it goes any lower just because COVID is still a bit of a sideshow here to the HDV, which are going to report out in Q4. So I think if it sells off too much you will see new buyers that want a cheap ticket on those results. At any rate, it is sure to be an interesting summer.

nice timing https://ir.eigerbio.com/news-releases/news-release-details/eiger-biopharmaceuticals-enters-75m-term-loan-agreement-and-5m

some good and bad. The financing is good. The omicron analysis they gave is good. The delay is bad.