Banks, Banks, Banks

There used to be this podcast that I listened to that was a great podcast. It was called Reply All. It was all about the internet and how silly and beautiful it is. It unfortunately blew up because one of the hosts got “canceled”. He was canceled because behind the scenes he was mean to other employees of the show, which was not all that surprising, since what made Reply All great was how he was mean to other employees on the show.

But alas, it is an unfortunate tale of loss that is for another time. The relevance here is that Reply All used to do this segment where their boomer podcast company owner (Alex Blumberg) presented the millennial hosts with tweets he didn’t understand and the hosts had to figure out those tweets and explain them. That segment was called Yes, Yes, No.

At some point the boomer podcast owner decided he would flip the table around and do a different segment where he, a sports enthusiast, would present sports tweets that he understood to the non-sports-enthusiast podcast hosts and explain them to the hosts. This segment was called Sports, Sports, Sports.

And that brings us to today. My new segment is called Banks, Banks, Banks.

This is the second installment. My first was on Home Capital. I didn’t want to blast out an email on that one because HCG is always such a powder keg. If you want to view the post just send me a note.

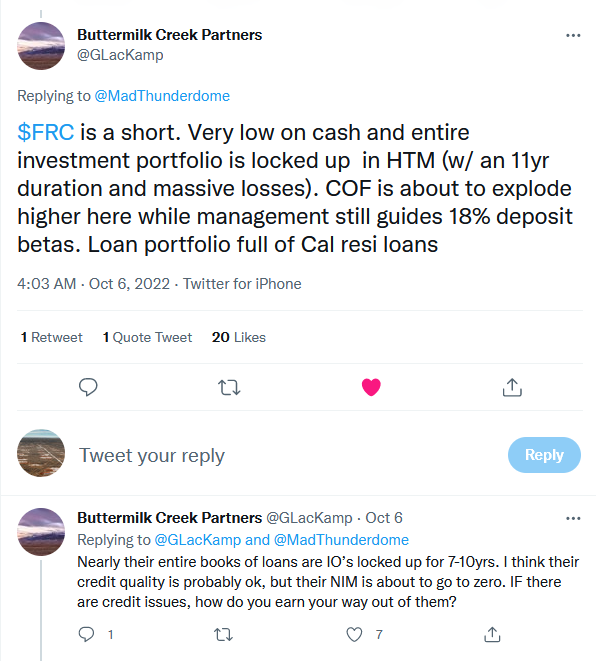

Today I will be discussing this tweet:

I found this tweet interesting because A. Buttermilk is advocating a short on a regional bank that had already been beaten up pretty darn bad and B. I didn’t know WTF he was talking about.

As it turns out, First Republic presents an interesting case. A whole pile of US banks reported on Friday (JPM, C, PNC, WFC, USB). Almost all of them had pretty good days, with most being up, which is an impressive feat considering the market as a whole was very much not up.

First Republic, however, did not do well.

Thankfully, I did not have a long position on FRC. I only sort of half-follow them. They are just one of the charts I have in my bank chart list, and I keep them there because they are a big, regional bank so I need to watch whats going on.

But then I saw the above tweet the other day, and I didn’t understand it. So I tried to figure it out.

I could spend a bunch of time going through what FRC is and does. But I won’t. Suffice to say that they are a California based bank, they pride themselves on their relationships with the households they lend to, they are known for having “pristine” credit quality, and they like to make mortgage loans. There is really not a lot going on here – its plain jane sort of stuff.

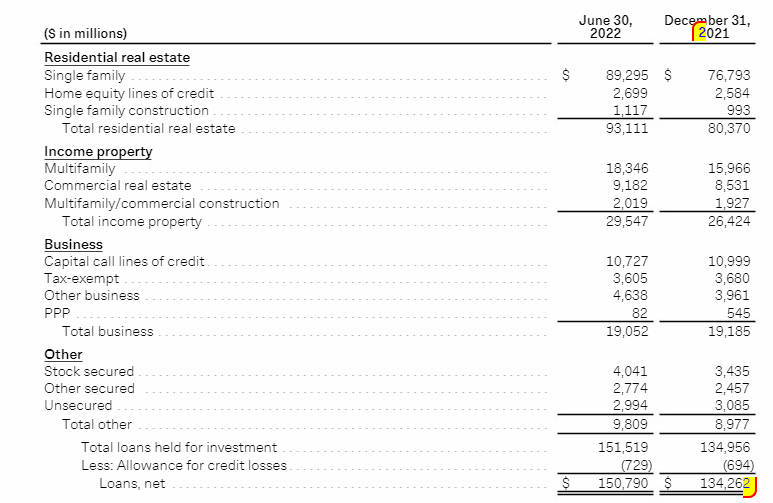

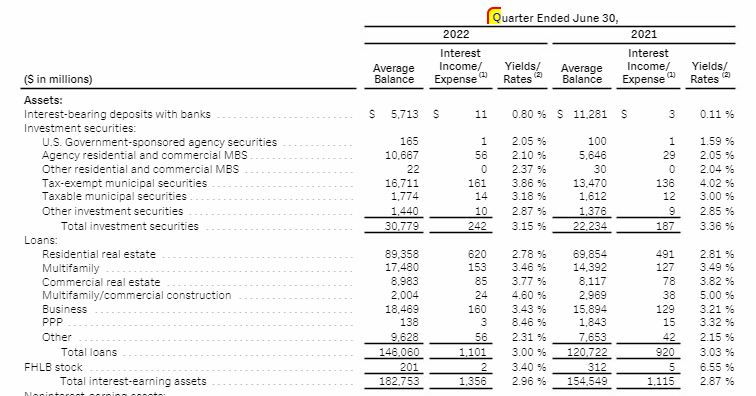

Anyway, this is First Republic’s loan book at a high level (I’m using the Q2 tables here because the 10Q wasn’t out when I looked at this but it is essentially the same for our purposes after Q3):

A couple of things about this loan book. First, its a lot of residential real estate loans. $93mm of $150mm in Q2. Second, though you can’t see it in the table, their balance sheet is pretty stuffed with loans. After Q3, they have $158b of loans and $172b of deposits. Compare that to a JP Morgan, where loans are ~50% of deposits.

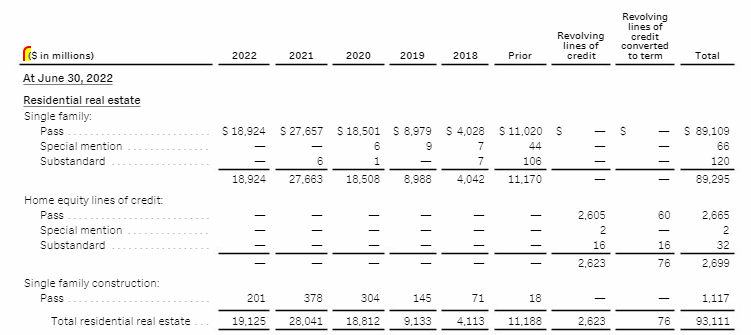

Like Buttermilk says, 52% of the single family home loans are in California. Take that for what its worth. More importantly, 60% of their single family home loans are interest only loans (I/O), with a very long interest only period – they amortize to maturity after 10 years.

I honestly didn’t even know interest only loans were still a big thing in the US. Who knew?

What’s more, most of these loans were made quite recently, in the last 4 years, meaning they are all still I/O and will be for a very long time:

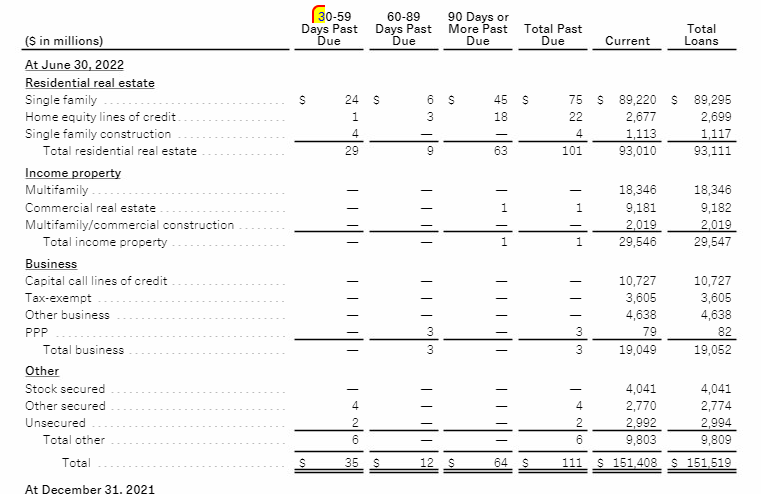

Now, to First Republic’s credit, these loans are not going bad. Very little of their SF loan book is past due.

If you compare the past due loans at the end of Q3 to the number at year end, it is actually doing better now, so its not like there is some big looming default risk here.

Instead, the risk is more on what they are going to earn from these loans.

We know that interest rates have gone up a lot. Many banks are seeing their net interest margin increase in Q3. That is why the banks that reported on Friday all did well.

When I looked at this earlier this week I was looking at First Republic’s Q2 numbers. This is what I saw:

Their residential real estate loans were actually seeing a tiny decline in yield. Now that was a bit odd because I/O loans are usually adjusted rate mortgages, or ARMs. I looked it up. But I don’t think that is the case here. They must be making fixed rate loans, or at least loans that have some sort of lag attached.

Now they do say that 23% of their loans are adjustable rate or mature in 1 year. But they don’t tell us just how much of that is adjustable and I have to assume the 23% really is skewed to the <1 year maturity because rates didn’t budge YOY on any bucket in Q2 (and only moved marginally in Q3, as you will shortly see) and if there was a sizable amount of adjustable loans those rates should be moving.

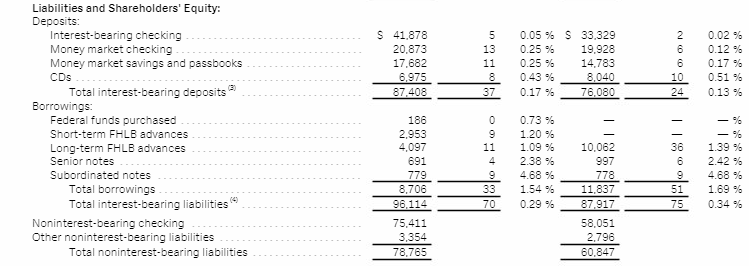

Nevertheless, in Q2 FRC was okay, because their deposit rates were quite low as well. They had hardly budged off a very low number (this is a Q2 10Q table).

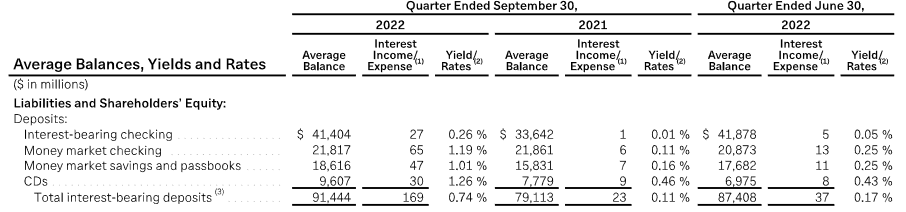

So everything was rosy. Cue the foreboding music. But, but , but… that changed in Q3. Some might call this an inflection. Here are deposit yields in Q3:

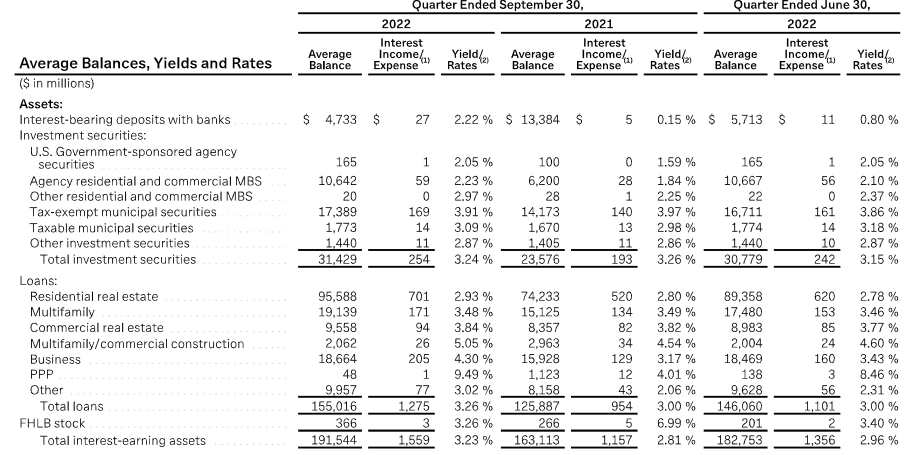

So deposits are costing more. But because their I/O loan book is not so adjustable, their loan interest did not keep up:

First Republic acknowledges they have a bit of an issue here. They guided NIM down for Q4.

In their closing remarks, they also kind of implied that things will likely get worse before it gets better:

Analysts are a little concerned. This is from another tweet, quoting the JPM analyst, who by the sounds of it has been a bull on the stock, and now appears worried about NIM:

And I think that is the story here.

Going back to the original tweet, let’s sum it up in Reply All style. We start with First Republic, a safe, plain-jane, regional bank that makes a lot of loans that people use to buy homes with. Many of these loans are long-term, interest only loans that appear to not be adjustable rate. Their loan book is also very full relative to their deposits – they have very little room to write more loans. Some investors like Buttermilk clued in that this might be a problem but until now, it wasn’t. In the third quarter it became a problem. Investors saw that First Republic needed to provide higher rates to their depositors but that they weren’t seeing a similar increase in rates from their (largely fixed rate real estate) loan book. This caused their interest margins to decline in Q3 and First Republic had to warn that these margins would likely keep going down. Everyone freaked out and sold the stock.

And that brings us to Banks, Banks, Banks.

It is a treacherous time to invest. Be careful.

Can you please send the post on Home Capital? Thank you. Mark ________________________________

I’d love to read the HCG post, thanks