Let’s Take a Look at Silvergate Capital

I don’t know if I was the first to start talking about Silvergate Capital but I think I can say that I was ahead of most of the crowd. As is usually the case, I was also one of the first out the door and way too early. I bought Silvergate in September 2020 at $22 and sold it a few months later at $70. It seemed like a crazy win at the time.

But Silvergate just kept on going. The stock was over $200 at one point!!!

It was bizarre to me. This was still a bank after all. And the economics of their cryptocurrency on-boarding platform were okay, but they needed a lot of transactions to make their fees amount to enough to justify the stock price of $200.

Maybe most concerting was simply that this was a bank trading at 4x book value and banks don’t trade at 4x book. Could Silvergate really have found the secret sauce? One that other banks could not replicate?

Well… as it turns out Silvergate sauce is not quite as tasty as we originally thought.

The stock price is down a lot. We’re at $55 now. Below where I sold it two years ago. Trading at 1.4x Tangible Book Value (they were smart to raise capital when the stock was nose-bleed), a decent earnings multiple.

It seems worth a look.

First lets see what we have here. Silvergate is a $1.7b market cap bank. They trade at 11x PE on this year’s earnings, 6.7x on next year’s earnings.

Silvergate makes money from net interest on loans and securities they purchase less what they pay on deposits just like every other bank. What makes them unique are A. their deposits come from crypto players and B. they make money on fees related to their Silvergate Exchange Network, which is the crypto on-boarding platform.

This is all the same stuff they did two years ago. It is really no more or less amazing then it was then, when investors decided it was worth $200+ share.

First, some numbers and notes from their Q322:

- EPS of $1.28

- ROE was 1.04%, ROA was 13%

- Their NIM was up from 1.96% to 2.31% – 36bps

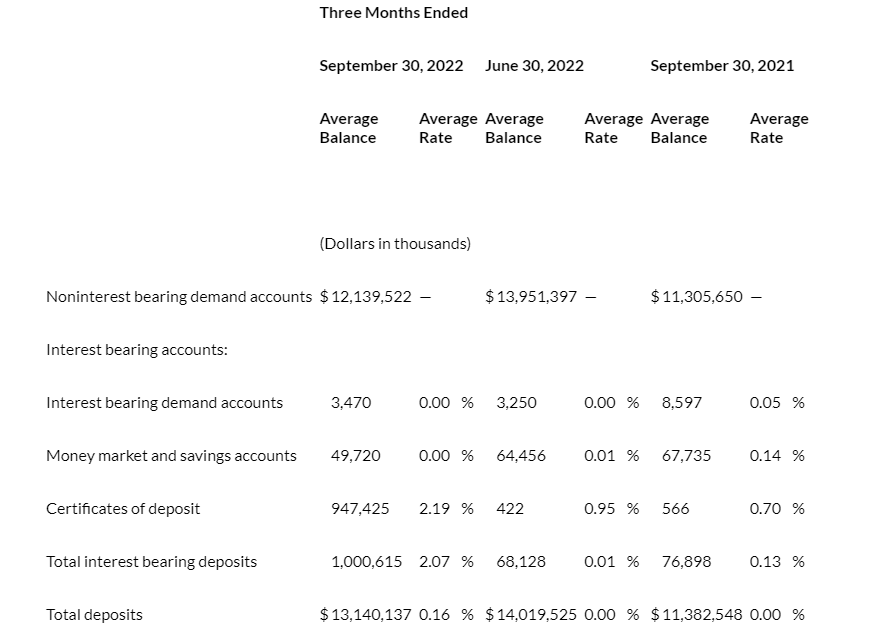

- Cost of deposits rose from 0% to 0.16%

- Book value is $36

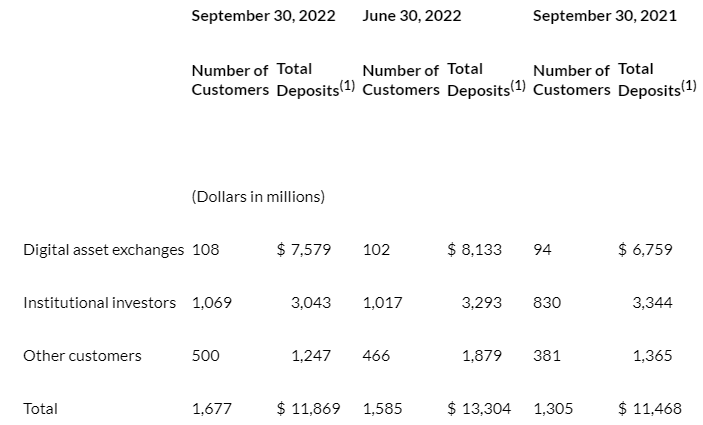

- Total deposits was down a touch – from $13.5b to $13.2b

- Digital Asset Customers: Q321: 1,305, Q222: 1,585, Q322: 1,677

- Digital Asset Transfers down big: Q321: $162b, Q222: $191b, Q322: $113b

- Overall net interest income was up $10mm to $84.7mm

- Fee income was down from $8.8mm in Q22 to $7.95mm in Q322 – it was flattish YoY – $8.2mm in Q321

- Interest margin on securities was up a lot: from 1.66% to 2.21%

- They used more broker deposits and more FHLB advances

A couple of things stand out.

First, fee income. Its not up at all YoY. This was supposed to be a growth driver. I was not convinced. I was right to be skeptical.

It could be worse though. If you look at how much transactions were down, you might have expected fee income to be worse. I couldn’t really find anything that explained why fee income held up so well.

Second, digital asset transfers were down a lot in Q322. Digital asset transfers refers to their main fee business, which is moving money back and forth from crypto to US dollars. I didn’t realize it until reading the transcript today, but Silvergate’s biggest customers are stablecoins, USDC for example (they said back in May they don’t bank Tether).

Silvergate is “the regulated stablecoin transactional bank” – so when coin is minted or burned it goes through SEN.

USDC, like the rest of crypto, has been slumping in terms of market cap (not in valuation, since it is pegged to the dollar). There have been less USDC deposits at Silvergate. They said on the call that:

So, I think in the quarter between Q2 and Q3, we saw the total market value of USDC declined from $55 billion to $47 billion, which is about a decrease of 15%. Silvergate average deposits were down about 13% or so

So we know the deposits at Silvergate are tied to stablecoins. Yet if you look at the balance sheet, Silvergate has not seen a noticeable decline in its overall deposits. From my notes above “total deposits were down a touch – from $13.5b to $13.2b”.

How is that possible?

It turns out that while deposits did not decline, digital asset deposits did. Overall deposits only dropped $262mm. Digital asset deposits dropped $1.4b.

How did Silvergate make up for the difference? Using certificate of deposits (CDs), which skyrocketed to $1b.

That is no problem, except… CD’s carry a 2.07% rate on them, whereas the deposits they replace carry a 0% rate.

The result is that “the average rate on total interest bearing liabilities increased from 1.17% for the third quarter of 2021 to 2.19% for the third quarter of 2022, primarily due to the impact of increased interest rates on short-term borrowings”.

As you can see from the table below, those interest bearing deposits increased rather rapidly QoQ. If they keep increasing like this, they are going to squeeze net interest margin a little eventually.

But there are mitigating factors. Mainly, that Silvergate is not run by crazy crypto bulls. They are run by bankers doing banker things.

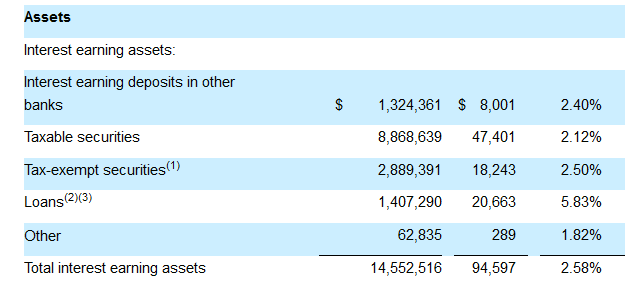

Silvergate is a bit funny for a bank because they don’t actually make very many loans. They only have about $1.4b of loans outstanding. Most of their assets are securities.

Silvergate is also very smart by only buying short-dated government securities. If you look at their security book, its almost all coming up in less than 12 months.

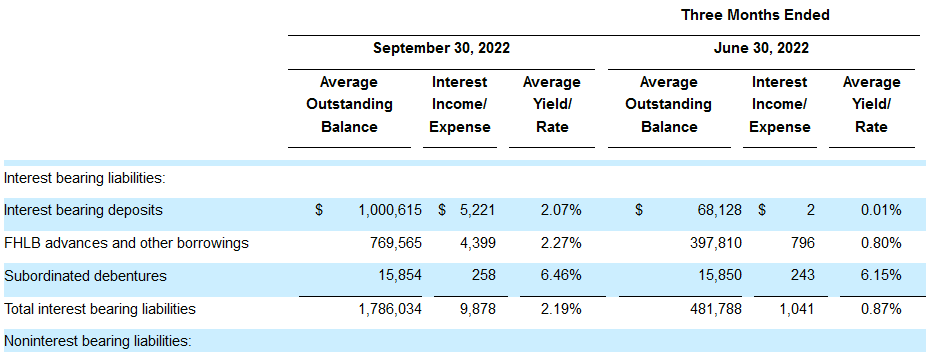

Here’s the thing about where Silvergate is at. If you look at the interest they collect, 2.58%, its only a smidge higher than their interest bearing liabilities – 2.19%. On the surface, this could be a big red flag.

But not as much as it might seem. For one, that is only considering interest bearing liabilities, and even though they are losing some non-interest bearing deposits, most are still non-interest bearing. For two, because they have prudently invested in very short dated government securities, they can reinvest at higher rates even as they need to pay higher rates for deposits.

And because there are so few loans, Silvergate doesn’t have to worry too much about default risk. They have no trouble with regulatory capital (their common equity tier 1 capital, a measure of how much capital they have to cover losses, is a rather ridiculously high 41%).

All this makes Silvergate a little uninteresting right now. They seem to be run pretty conservatively, so I don’t think anything is going to blow up here. On the other hand, because their main source of fee income is tied to crypto, it is hard to get excited about buying the stock.

They said themselves on their conference call that their business is based on Bitcoin and crypto volatility. Volatility brings on transactions and they get more fees the more the money moves. Until we get through this bear market I’m not sure we are going to see meaningful upticks in Bitcoin transactions.

The one other interesting thing of not is that they are planning a true dollar token:

We continue to balance our culture of innovation with our prudent risk-based approach to launching new products and are actively engaged with regulators and policymakers in anticipation of launching a regulatory compliant tokenized dollar on the blockchain. Unfortunately, we no longer expect that to happen this year.

The stablecoin they want to issue themselves is tied up with regulatory hurdles. But I can see why they want to have their own stablecoin.

The thing right now is that they don’t have stability in deposits. When transaction volume decreases, stablecoins don’t need to hold as much deposits with them. Silvergate said on the call that “we have always encouraged our customers to take their sort of excess deposits, if you will, or the deposits that they don’t need for issuance and redemption to other banks that do pay interest.”

So in bad times those deposits go away. That wouldn’t be the case if they had their own stablecoin.

You know, all this time everyone talked about how the risk to Silvergate was a big bank getting in the business. That they would eventually get squashed.

That may still be the case in the long-run. But it seems to me that the big risk right now is a long crypto-winter that pulls money out of the bank and eventually causes them to have to shrink.

It would be no spectacular blow up. It would be just slow dimming until the next Bitcoin bull market comes.