Was this why Atna was down yesterday?

In the last few months I have sold off most of my gold holdings, but I decided to stick it out with Atna Resources. That hasn’t looked like a terribly good decision these last couple of days, as the stock has been clobbered down to well below a buck.

Yesterday I looked at the stock thirty minutes before the market closed. It was at 94 cents. I was rather shocked to see later on that it had closed at 84 cents.

It being an earnings release day, I had already scoured the news release and determined it looked mostly benign. However I also know that Canadian regulations call for a filing of the Management Discussion and Analysis report on Sedar. The thing about Sedar is that these reports become available to paying subscribers a little bit before they do for the general public. When I saw the stock drop I wondered whether there was something in the MD&A that insited it.

This morning the MD&A was made publically available. Though I don’t think it is worthy of a 10% drop, I suspect that the following may have contributed to the drop:

The principal requirement within the next 12 months is expected to be funding development of the Pinson underground mine at a cost of $18 to $22 million. This range of costs is likely to increase when a new Technical Report is completed. Atna is considering additional sources of financing to address any potential contingent risk of having inadequate capital to complete the Pinson underground development in 2012, possibly to accelerate the development of Reward, and to ensure funding for the aforementioned projects.

Normally this might be seen as being fairly benign. In the current environment, where even good news is sold and investors are skittish that all gold stocks will soon be worthless, it carries a particular bite.

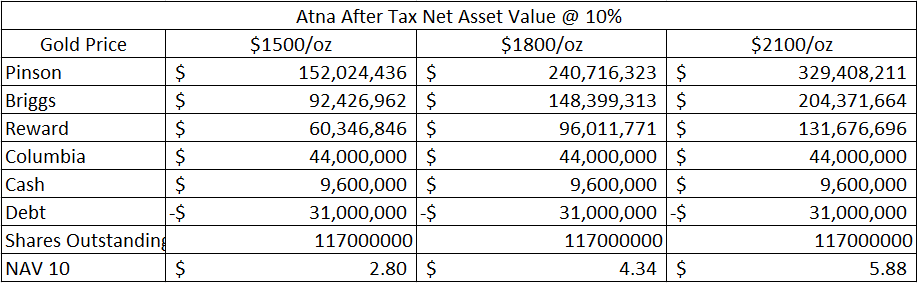

I always have known that Atna is skating on relatively thin ice with respect to the development costs of Pinson and the available cash on hand. The current report merely confirms that. I have to suspect that the reason the company has not released the technical report on Pinson (that they had originally said would be released at the beginning of May) is because they are trying to line up some financing to give the wiggle room they need. With the current share price depressed, I hope the financing is of the debt sort.

However before I concede yesterdays losses to this buried nugget of coal, it must be said that most gold stocks were down significantly. In fact it looked like a day where the larger institutions were throwing in the towel, with companies like Detour Gold and Osisko Mining down more than 10%.

It simply is a terribly time to own any gold stock. I had thought that the growth profile of Atna might overcome that gravity. Unfortunately that has not been the case.

The good news is that Atna is back to a level where it has completely unpriced Pinson from the share price. In other words, how much lower could it possibly go? You also have to wonder whether there are intermediates looking at the company. A company like Aurizon for example, with $200M in cash, could buy Atna, develop Pinson and have a growth platform for the future, all of which could likely be had for less than what they have in the bank.

I remain committed to my shares. The company has the potential to generate cash flow from Reward and Pinson next year that will match or exceed the current share price. Its too bad that the company hasn’t been a bit more prudent in managing cash levels and taking advantage of the $1.50 share price to raise a buffer of cash but that is what it is. The stock, like so many gold stocks, remains deeply depressed and it seems foolish to me to sell my shares at these levels.