My Canaco Debacle

My post on Canaco’s Magambazi deposit has received more attention than perhaps any other post I have made. What is sadly ironic is that while I put a lot of work into my evaluation of Magambazi, the net return of all of that work has been less than zero. I want to take a few paragraphs here to do a post-mortem on the subject and to come up with a few lessons learned.

Lesson #1 Analysts can be lazy and you shouldn’t believe they know more than you

I began my relationship with Canaco at the end of last year in an attempt to take advantage of tax loss selling. I bought the stock at $1.10 having done very little research into the company besides having read through the corporate presentation, acknowledged they had a significant amount of cash on the balance sheet, and read through a couple of Canaccord reports that I got my hands on, suggesting that Magambazi had somewhere between 2-3 Moz of gold.

![]()

Soon after the stock ran up along with all the other gold stocks and I felt like I better get a more clear idea of what I owned and whether I should continue to own it at that elevated price. Thus came about my analysis of the Magambazi desposit. I did my analysis of Magambazi when the stock was $1.70. The analysis suggested that the Magambazi deposit was unlikely to contain 2-3 Moz and was far more likely to contain 1-2 Moz, with the greater potential being on the low end of that range.

As I wrote at the time, while my analysis raised a lot of questions, I was reluctant to believe it over the parade of analysts with estimates of 2 million ounces plus grading 3 g/t or more:

All 3 of these estimates are lower than I would have expected. To be honest, I’m not sure what to make of that. I don’t know how much I trust my own work given the uncertainty with specific gravity and obviously the low-tech tools I am using.

In the end I concluded that I could quite possibly be wrong, and that even if I was right, the stock was probably trading not too far away from where it should given the cash on the balance sheet. I concluded that while I wouldn’t add more, I wouldn’t sell my holding right away either.

Fortunately my conviction tends to be heavily influenced by price level, and as the stock began to fall, I changed my tune. Soon after my write-up gold stocks began to fall (in particular junior explorers began to be decimated). I wrote the following:

While I still question whether there is an error in my analysis, I do think I raised enough questions about the deposit, and enough uncertainty about the eventual resource estimate to be somewhat wary of the NI 43-101 that will be out shortly. I decided to step aside until that resource comes out, or the share price falls back to the point where I feel like the downside is priced in.

I sold my position at $1.47 per share.

It is at this point that it all could have ended well. I could have ridden off into the sunset with a tidy profit and a big “I told you so” in the mail when the 43-101 on Magambazi came out.

But it didn’t end well. Because I got cute.

Lesson #2 Don’t get cute

In retrospect my reasoning on the matter was fairly sound. The logic based on the knowledge available was acceptable. The problem, I believe, lay in optimism of my original assessment, which was perhaps unconsciously skewed by an attempt to match analyst estimates that were far more robust than what I was seeing.

Anyways, here is how it went down.

Canaco was trading at 85 cents. They had 50 cents of cash in the bank give or take. I looked at Magambazi and thought, look, they are going to report at worst 1 Moz at 3 g/t, how much lower can the share price go? Its priced in right?

I bought Canaco at 87 cents.

![]()

It didn’t seem like a bad bet at the time. And fortunately I didn’t buy a very large position (actually looking at the relative size of the position in my practice portfolio it appears I over-bought there. My actual position in Canaco was about 1% of my overall portfolio, but it looks like I bought around 3% in the practice portfolio. I’ve noticed this is a continuing problem for me because I’m not doing the ratios with each trade and so my practice portfolio has gotten somewhat out of sync with my actual portfolio. But enough of that).

Nevertheless, unfortunately it would turn out to be large enough to take away all the profits I had made and then some.

When I look back on this fateful purchase I notice two catalysts to the downside that I really underestimated at the time:

- The junior market was about to go into a deep bear market where even cash is not valued at cash anymore

- The reported 43-101 grade of Magambazi would be based on an open-pit model

Number 1 is what it is and what can you say. Its a shitty market. It was #2 that really killed the stock. When the deposit came in at 1.5 g/t that was final nail in the coffin. Even my estimates calculated that the average grade would be 3 g/t.

So what happened to the grade?

Canaco hasn’t released the actual Ni 43-101 report so I can’t really talk too specifically about the assumptions made. But they did say in the news release that the resource was based on a pit model:

Measures were taken to validate that the mineral resource meets the condition of “reasonable prospects of economic extraction” as suggested under National Instrument 43-101. To this end, a pit shell was generated using a gold price of US$1,250 per ounce and an overall pit slope of 40° for the purpose of resource tabulation. Only blocks within the pit volume were included in this resource estimate and Table 2 presents a summary of the estimated mineral resource for a range of cut-off grades. The cut-off grade of 0.5 grams per tonne was selected as the resource base case considering extraction by conventional surface mining and mineral processing methods.

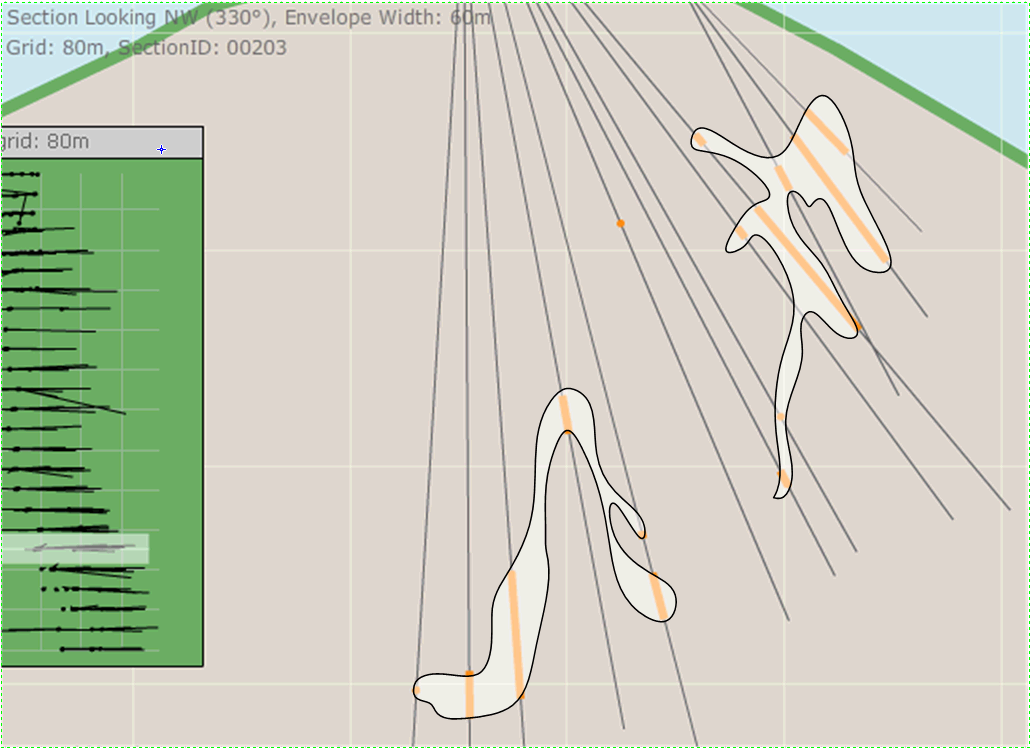

When I did my estimate I made a very tight block model around the high grade intercepts. I drew my lines to fit exactly around each intercept, with no give or take around it. Take a look at the cross-section below for example:

I suspect that what happened is that when the open-pit model was done, it was determined that realistically, you were not going to be able to separate the high grade ore from the low grade shell so easily. You would inevitably end up with a diluted grade going through the mill and so the mined deposit grade would be a lot lower than what you would get if you could just surgically extract the high grade material.

I totally missed this. Its obvious in retrospect. Canaco management even said they were looking at Magambazi as an open pittable project. But I didn’t put two and two together.

Cést la vie.

I remember when I read the news release when it came out in the morning the first thing I thought was, wow, that’s really bad. As I tweeted that morning, that’s why you call it speculation, not investment. I put in a sell at the market order, I figured that with 50 cents of cash I’d still get out at over 50 cents and be done with it. Alas, before the market opened it became clear that the stock wasn’t going to trade at anywhere near 50 cents. It is unfortunate in cases such as this that because I have a job and cannot watch the market during the day, I often have to make decisions to buy or sell at the open in premarket and deal with the consequences later. Weighing the alternatives I took the order off and decided to see where the stock ended up.

Lesson #3 When something is bad, its rarely worth buying

The basic premise here could be applied to many things; bad managements, bad businesses, and bad markets. It certainly could be applied to bad deposits. If its bad, don’t try to put a value on it. Just walk away.

When I bought back Canaco at 87 cents, it was because I figured the market was overestimating the “badness” of Magambazi and underestimating the cash on hand. Between that purchase, and my sale of Canaco at $1.47, I had implicitly put my own valuation on that badness – somewhere between a dollar and a dollar fifty a share less the cash on the balance sheet.

The problem with doing this is that badness tends to have an extremely relative value. Something good tends to hold its value regardless of the market, but something bad tends to fluctuate wildly as participants go between optimistic and pessimisstic evaluations of just how bad it is. To make a case and point, look at Lydian International. I sold out of Lydian a couple of months ago when I was liquidating all things gold but dine that time the stock has held up remarkably well. That is because, as I pointed out in my initial analysis, the Amsular deposit is basically a good, solid deposit. There are always bidders that step in when the stock begins to sway.

Canaco is the opposite. Magambazi is a questionable deposit. It still might work. It might not. Me trying to put a value on that was stupid. When something isn’t good, you need to just walk away.

Where to go from here?

I talk a good game but sometimes I don’t do what I say. Perhaps I will look back on this with another lesson learned and say that yes, I should have just walked away at 30 odd cents. But I haven’t. At least no yet. In the case of Canaco, even though Magambazi had proven to be bad, I was just too tempted by the fact that the company was trading at about 2/3 of its cash on hand. Cash is neither bad or good. It is cash. When cash is valued as though it wasn’t cash, I am always tempted by the opportunity to prosper from its revaluation back to cash.

I bought a few more shares at 32 cents.

![]()

It just seems rather insane to me that we are in an environment where the cash you have on your balance sheet isn’t valued as such. And yes I know this is an exploration company, and they could eat up that cash in a number of stupid ways. But still… a little less than 50 cents of cash trading at a little more than 30 cents?

Another point that Canaco has in its favor is that the actual amount of cash is quite significant compared to drilling and corporate expenditures. If Canaco was a $5M market cap company with $7M in cash, I would be far more skeptical that they would eat through that cash quickly and therefore that it shouldn’t be valued on their balance sheet at whole value. But Canaco is a $60M market cap company with $95M in cash in the bank. The company has apparently stopped drilling on Magambazi at the moment. Cash corporate expenses look like they are about $1.3M per quarter. Its going to take a while and a good number of bad decisions for that cash to disappear.

The other point is that Magambazi, while being a relative disaster, is not a complete disaster. The market, with its unrealistic expectations having been set by the analyst community, certainly viewed it as such. Yet there are 1 Moz there, and there is the potential for more. The cash provides the opportuntiy for good things to happen. Heck, even a general market recovery (something that albeit may be fantasy and that I am not myself leaning towards) could be enough to move the stock significantly towards its cash value.

Anyways, those are the reasons. I make no promises about how long I will continue to hold any of these shares. I may decide that the opportunity cost of holding Canaco isn’t worth it and just dump the whole thing. If the share price goes on a run, which given just how bad it has performed with essentially no bounce makes you think some sort of a pop may be possible, I would likely sell. I would certainly sell at cash value; I might even sell at 40 cents.

Until that time, the debacle continues.