Week 324: Underlying Conditions

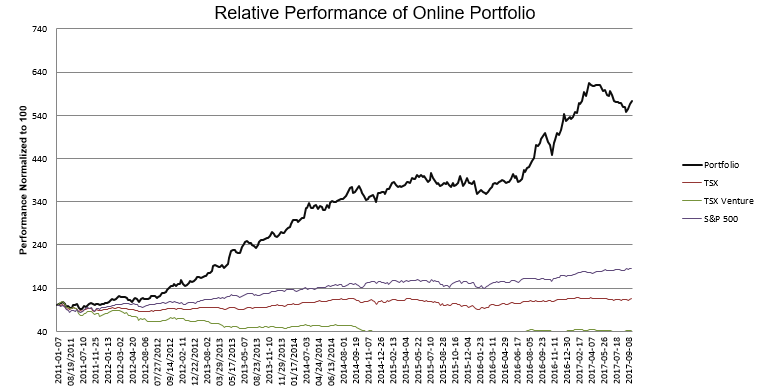

Portfolio Performance

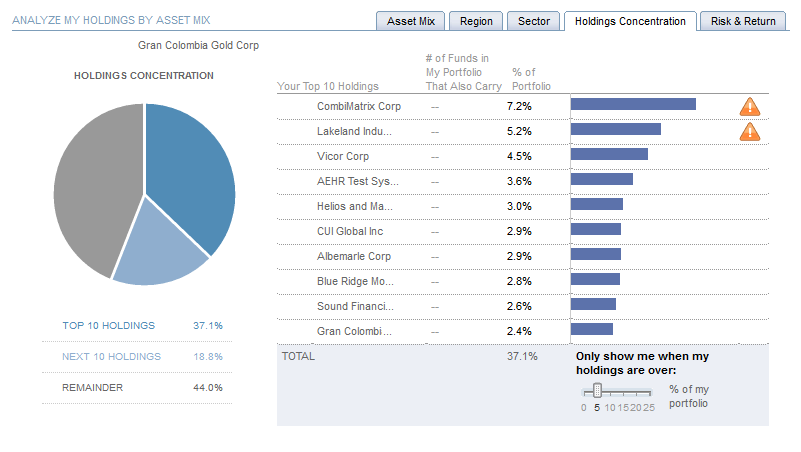

Top 10 Holdings

See the end of the post for my full portfolio breakdown and the last four weeks of trades

Thoughts and Review

The late spring and early summer months were a trying time for my investments.

I haven’t written up my portfolio in a while. Part of that was due to the summer, being away and not having the time to do my usual work. But I also went through a 3 month period, from mid-May to mid-August, where I lost money and struggled with why. That dampened my spirits for putting pen to paper.

Losing money is hard enough, but it is harder when you have been generally right in your decisions. I try, like the namesake of this blog, to analyze underlying conditions and let that determine my general bent on sectors and the market. Where there is a bull market I like to be very long those stocks, and when there is a bear market I like to pull back significantly, retreat into cash, and go short where I can.

Throughout the spring and summer I found myself in a general bull market in US stocks, one that had made me a lot of money throughout the winter. I was, quite rightly, very long US stocks. The market kept going up, albeit in fits and starts. But I began to lose money. Now I didn’t lose money quickly. In retrospect that may have been a better route as at least I would have been forced to discover my error. But instead my losses slowly accumulated over the months of May and June.

What’s more, I did not see noticeably poor performance from any of the stocks I owned. Sure my names weren’t breaking out to new highs, but my core positions at the time, the likes of Radcom, Silicom, Sientra, Combimatrix, Identiv and Vicor were not by any means breaking down (I leave out Radisys as it is a separate discussion).

It wasn’t until my portfolio was down about 6%, in the middle of June, that I woke up to the fact that something was wrong. I scoured my list of stocks but found nothing worrisome with the names I held. I knew that the Canadian dollar had been rising so that must have been having some effect but I had never really quantified my currency exposure. I had always thought of currency as an afterthought, something that balances itself out in the end.

As I crunched through the numbers on my currency losses, I realized that while in the very long run my theory that currency balances itself out might be correct, in the short run a currency can make or break you. The Canadian dollar was in the midst of unwinding 2 years of gains in two months. Measuring my losses from the portfolio top in mid-May, I was 6% down, of which 5% came from currency.

It is here that I made my first big mistake. I was armed with the information I needed to act decisively. I knew my problem: stocks were in a bull market, but clearly the US dollar was not, and I was, rather unwittingly, very long the US dollar.

So what did I do? Something that, in retrospect, was absurd. I made only a token effort towards the problem, taking only the excess US dollar cash in my portfolio and putting it into a Canadian currency ETF. This effort, while directionally correct, impacted about 15% of my US dollar holdings and thus did nothing to alleviate the problem. I followed this up with an even more inexplicable move, even to me looking back on it now. I put on index shorts to hedge my long positions.

Here I was with losses proving that I was wrong. I had determined the source of those losses. And what did I do? I did something that was likely only to exacerbate them.

It really goes to show how wrong one’s logic can be when you are trying to cling to what you had. The reality, I think, is I didn’t want to do what was right. What was right was to sell my US stocks. Not because my US stocks were going down. They were not. Not because the theses behind these positions was not sound. They were. But because I was losing money on those US stocks.

Unfortunately I could not wrap my head around this. All I saw were good stocks with strong catalysts. How could I sell my positions? It’s a bull market!

I spent most of June compounding my problem with band-aid solutions that only dug me in deeper. I fell back on oil stocks as a Canadian dollar hedge. This had saved me the last few times; in the past the Canadian dollar had risen because oil had risen, so I had gone long oil stocks and my losses on currency were more than compensated with my gains on E&Ps. I was saved a lesson and left none the wiser to how impactful currency could be.

But this time around the currency was not rising because of oil. My appraisal that I should be long oil stocks was based on the flawed logic that what works in the past must work again regardless of conditions. That is rarely the case. In June and July I bought and lost money on companies like Resolute Energy, US Silica and Select Sands, all the time continuing to hold onto US dollars and lose on them.

I also went long gold stocks on the similar thesis that if the US dollar is weak then one should be long gold. In this case I was at least partially correct. That is the right thing to do given conditions. But my conviction was misplaced. Rather than being long gold stocks because I thought gold stocks would go up, I was long gold stocks to hedge my US dollar positions. You cannot think clearly about a position when you are in it for the wrong reasons even if a right reason to be in it exists. Thus it was that in late July I actually sold a number of my gold stock positions. It was only a couple weeks later, finally being of a clear head (for reasons I will get to) that I bought them all back, for the right reasons this time, but unfortunately at somewhat higher prices.

As I say it was at the beginning of August that I finally was struck by what I must do. I’m not sure what led me to the conclusion but I think an element of deep disgust played a part. I had just seen my biggest position, Combimatrix, get taken over for a significant premium. My portfolio took a big jump, which took down my losses from my mid-May peak from -10% (over 8% due to currency!) to -7.5%. But then in the ensuing days I saw those gains begin to disappear. Part of this happened because Radisys laid an egg in their quarterly results, but part of it was just a continuation of more of the same. Currency losses, losses on index short hedges, some losses on my remaining oil stocks, and the ups and downs of the rest of my portfolio.

I simply could not handle the thought of my portfolio going back to where it was before Combimatrix had been acquired. I was sick of losing money on currency. And I was reminded by the notion that you never see conditions clearly when you are staked too far to one side. So I sold.

When I say I sold, I really mean I sold. I took my retirement account to 90% cash. I took my investment account to 75% cash. There were only a couple of positions I left untouched. And I took the dollars I received back to Canadian dollars.

I continued to struggle through much of August, but those struggles took on a new bent. I was no longer dealing with portfolio fluctuations of 1%. The amounts were measured at a mere fraction of that. This breathing room afforded me by not losing money began to allow me to look elsewhere for ideas.

I don’t know if there is an old saying that ‘you can’t start making money until you stop losing it’, but if there isn’t there should be. When you are losing money, the first thing you need to do is to stop losing it. Only then can you take a step back and appraise the situation with some objectivity. Only then can you recover the mental energy, which until that time you had been expending justifying losses and coping with frustration, and put it towards the productive endeavor of finding a new idea.

In August, as my portfolio fluctuated only to a small degree but still with a slight downward slant, I mentally recuperated. And slowly new ideas started to come to me. It became clear that I was right about gold, and in particular about very cheap gold stocks like Grand Colombia and Jaguar Mining, so I went long these names and others. I realized that being short the US market was a fools errand, and closed out each and every one of those positions. I saw that maybe this is the start of another commodities bull run, and began to look for metals and mining stocks that I could take advantage of. I found stocks like Aehr Test Systems and Lakeland Industries, and took the time to renew my conviction in existing names like Air Canada, Vicor, Empire Industries and CUI Global.

Since September it has started to come together. I saw the China news on electric vehicles and piled into related names. Not all have been winners; while I have won so far with Albemarle, Volvo, Bearing Lithium and Almonty Industries, I have been flat on Leading Edge Materials and lost on my (recently sold) Lithium X and Largo Resources positions. Overall the basket has led to gains. I’ve also been investigating some other ways of benefiting from the EV shift. It looks like rare earth elements and graphite might be two of the best ways to play the idea, and I have added to my position in Leading Edge Materials (which has a hidden asset by way of a REE deposit at the level of feasibility study) to this end. Likewise nickel, which is not often talked about with electric vehicles and has been pummeled by high stock piles, has much to gain from electric vehicles and could see a resurgence over the next couple of years. I’m looking closely at Sherritt for nickel exposure and took a small position there so far.

I saw that oil fundamentals were improving and got back into a few oil names, albeit only tentatively at first. Such is the case that once you are burned on a trade, as I was when I incorrectly got into oil stocks in June and July for the wrong reasons, you are hesitant to return even when the right reasons present themselves. Thus it has taken me a while, but over the last couple of weeks I have added positions in Canadian service companies Cathedral Energy and Essential Energy, and E&Ps Gear Energy, InPlay Oil and even a small position in my old favorite Bellatrix. A company called Yangarra Resources has had success in a new lower zone of the Cardium, and I see InPlay and Bellatrix as potential beneficiaries. These newer names go along with Blue Ridge Mountain Resources, Silverbow, and Zargon, all of which I held through the first half slump in oil.

I even saw the Canadian dollar putting in the top, and converted back some currency to US dollars a couple of weeks ago.

Most importantly, got back to my bread and butter. Finding under the radar fliers with big risk but even bigger reward. I have always said it is the 5-bagger that makes my returns. If I don’t get them, then I am an average investor at best.

I found Mission Ready Services, which hasn’t worked yet but I think is worth waiting for. I found some other Canadian names that I think have real upside if things play out right (in addition to the above mentioned metals an oil names, I added a position in Imaflex). Most profitably, I was introduced to Helios and Matheson after reading an article from Mark Gomes.

I don’t completely understand the reason why, but good things do not come to you when you are mired in a mess of doing things that are wrong. It is only when you stop doing what is wrong that other options, some of which may be right, will begin to present themselves.

I also don’t know which of what I am doing now will turn out to be right, and what will turn out to be wrong. I will monitor all my positions closely and try to keep a tighter leash than I have been. What I do know is that I will not continue to be wrong in the same way I was through the months of May to August. And that is a big step in the right direction right there.

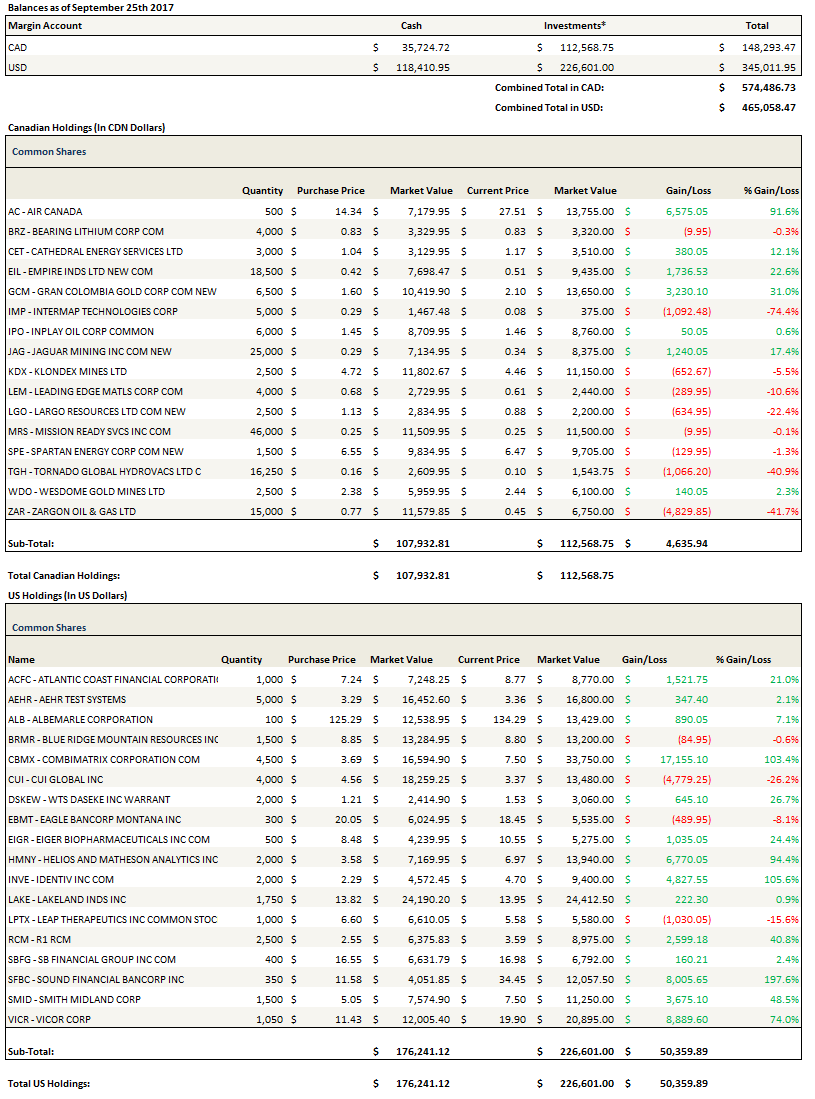

Portfolio Composition

Click here for the last eight (!!) weeks of trades. Note that in the process of writing this update I realized I do not have a position in Gear Energy or Essential Energy in the practice portfolio. I have owned Gear for over a month and Essential for a few weeks. This happens from time to time. I miss adding a stock I talk about and own in my real portfolio. I added them Monday but they are not reflected below.

Note as well that I can’t convert currency in the practice account. I know I could use FXC but in the past I haven’t, I have just let the currency effects have their way with the practice portfolio. Thus you won’t see the currency conversions that I talked about making in my actual portfolio. I may change this strategy the next time the Canadian dollar looks bottomy but as I am inclined to be long US dollars at this point, I’m leaving my allocations where they are for now.

{kind=link}