I need to come up with a way to get my writing out on this blog more regularly. I haven’t posted in a while but that doesn’t mean I haven’t been researching and writing. I have. I have posts on Air Canada, Blue Bird, Crocs, UIPath, PagerDuty, Snowflake, HBT Financial, Innovative Solutions and a few others. I just keep getting this uncomfortable feeling about all the emails that get sent out when I put them on the blog.

To try to get past that, I deleted about 400 subscribers that I have again accumulated over the past 4-5 years, when I last did a purge. There is only about 40-50 left and I think I know pretty much all of those names in some way.

So hopefully that is going to help me get over this stage-fright and put up some of the stuff I’ve written. I’ll try to stagger it out.

This post is about Star Bulk Carriers, which I don’t own, but am thinking I will own some time soon.

What I wanted to do here is see whether this company is cheap at this level. I have begun to convince myself that it is.

First lets go through the numbers.

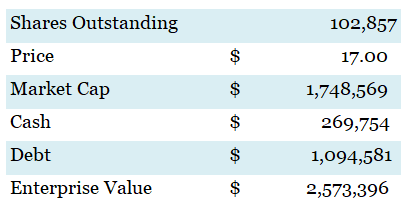

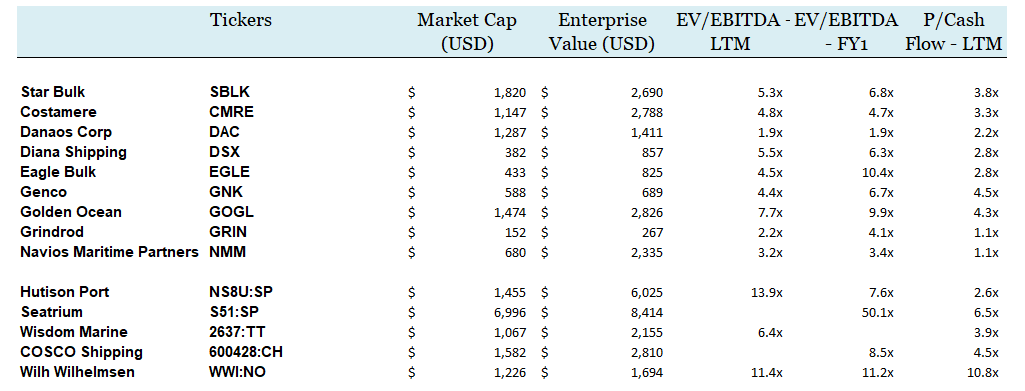

Right now SBLK trades at 9.7x P/E and 6.8x forward 2023 EV/EBITDA. All these dry bulk stocks trade quite cheaply on TTM cash flow:

WHAT ABOUT Q2 RESULTS

SBLK earned 47c EPS in Q223. They paid out a dividend of 40c for the quarter. They have a variable dividend that follows their earnings closely. This means that you can’t count on that dividend, it is more of a bonus.

SBLK also bought back 307k shares in Q2 – that’s a buyback rate of 1% of outstanding per year. If you go back through the last few years the share count has risen, not fallen, so while they are buying back stock, it isn’t offsetting dilution.

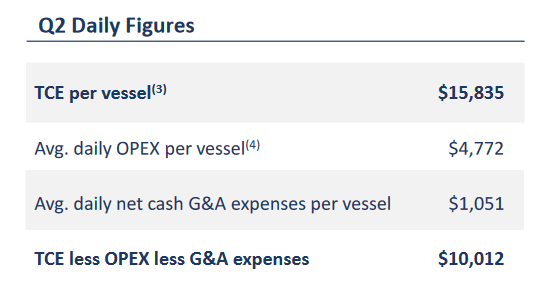

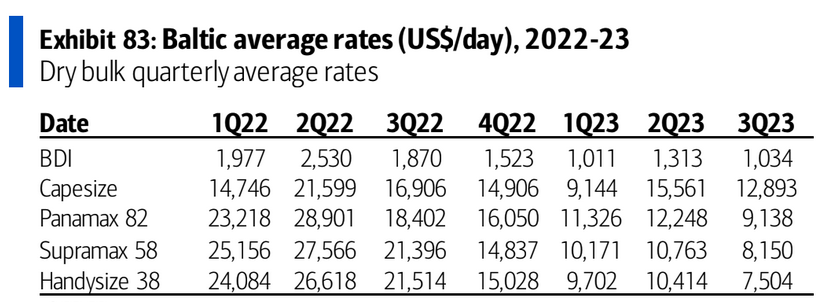

TCE for the quarter was $15,835 per vessel per day. This has come down A LOT from the highs of a few years ago. We are pretty close to historic levels now, which is one of the reasons I’m thinking about the stock:

SBLK has definitely been paying down debt and raising cash the last couple of years. They aren’t really levered at all, which was always a knock against these shipping companies.

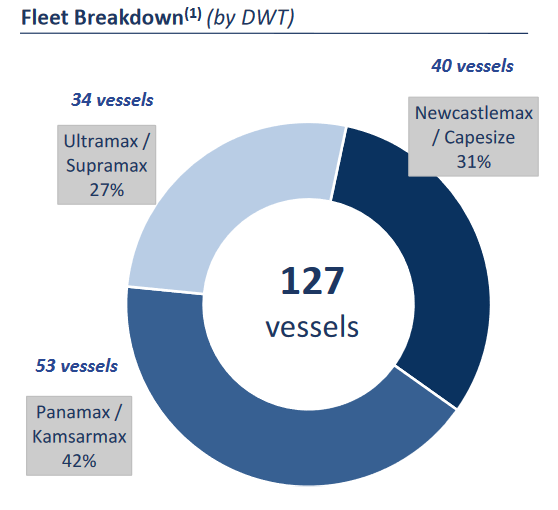

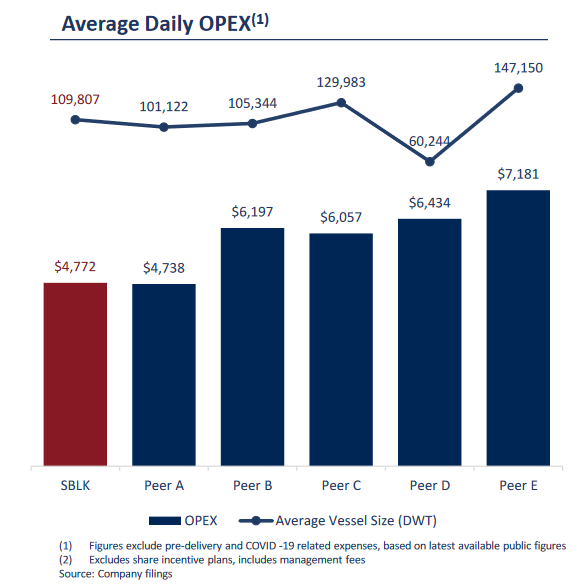

SBLK owns 120 ships with total tonnes of 13,347,973 DWT. This is the largest fleet among US and EU peers. They own a pretty even breakdown of the big, bigger and biggest dry bulks ships:

They have another 6 new builds coming in 2024. 4 are Kamsarmax and 2 are Ultramax.

From everything I have read, Star Bulk is one of the best operators. They have some of the lowest costs in the industry (I have a chart on that at the end). They haven’t done anything particularly stupid like some of these shipping companies are prone to do. They just are what they are – a shipping company that moves with the dry bulk market.

WHAT ABOUT DRY BULK SUPPLY/DEMAND

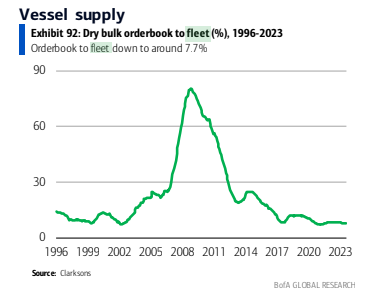

According to Star Bulk the order book is low:

Looking back historically, that is about as low as it goes.

The order book also doesn’t look too bad to me. It is just about as low as it has been and it is down YoY for the first 6m

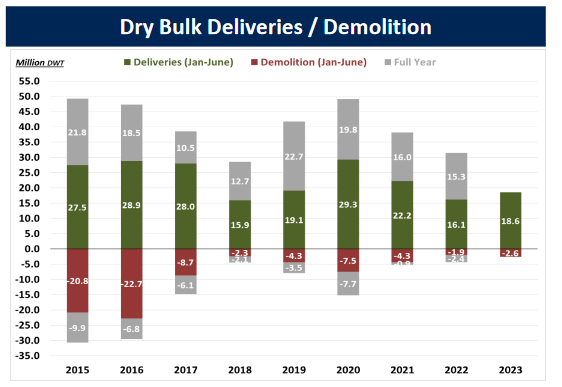

The delivery numbers don’t look too bad but the demolition numbers are low:

Fleet growth is expected to be pretty muted for the next couple of years. Only abought 1% for 2024 and 2025.

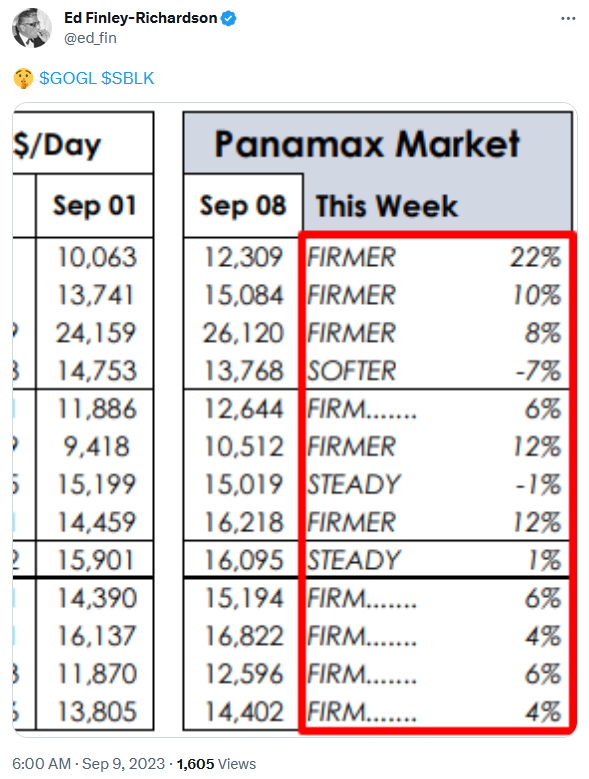

Here are some industry comments from Twitter:

First this. There is some evidence that dry bulk rates are bottoming and firming up.

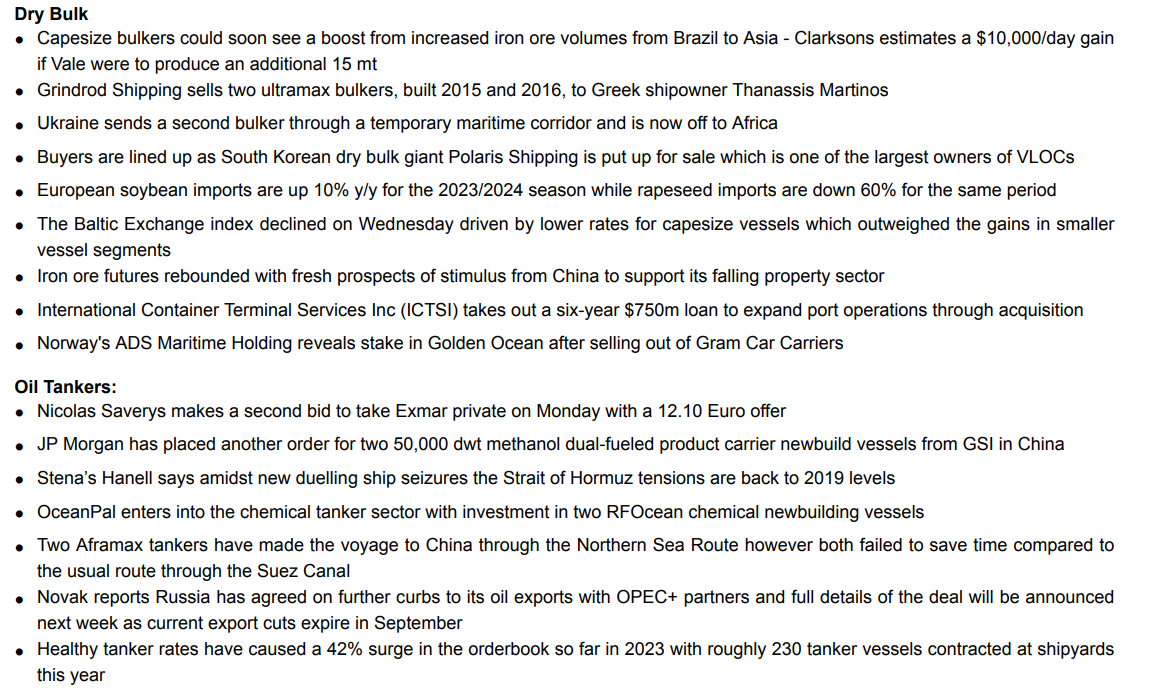

These are some thoughts on the market from Stifel. There isn’t really too much here other than that iron ore volumes could increase:

Stifel has a pretty strong rate outlook. if their base case plays out SBLK almost has to go higher.

VALUATION

Star Bulk has an NAV of $20 based on current vessel values. The stock has pretty consistently traded at between flat to a 30% discount to NAV. It is about a 14% discount right now. But also consider that this is off an NAV that is quite a bit lower than it has been even 6 months ago.

You could make the argument that on P/NAV SBLK is expensive compared to comps like GNK and EGLE. Both of these stocks are trading at more like a 30% discount. But SBLK is also out-earnings those companies. As I mentioned earlier, SBLK has some of the lowest OPEX in the industry. So they get more out of their ships than their peers.

Also playing to the “out-earning” idea, they aren’t comparatively expensive on operating metrics.

What are the risks? In the short-term, I think it is mainly global growth. A deep recession would hit them of course. China needs to pull out of its funk.

Over the longer term I have to think coal demand is a risk. But I don’t know if that is worth considering as a trade idea for the next 6-18 months. I’ve screwed myself enough ignoring oil because of my longer term worries.

But absent a big recession, I don’t think a big decline in rates is a risk any more. Rates have mostly done a round trip.

In Q2 SBLK had an average Time Charter Equivalent rate of $15.8k per vessel. In 2019 they did $13k and in 2018 $13.8k. Looking at the table below, rates were 2x to 4x current levels at the peak, depending on the ship (note that these are spot monthly rates, which are lower than the 1-year charter rates that are in the other charts/tables).

The stock itself is not all that different than it was before Covid. The price (unadjusted for dividends) today is $17.50 vs $12 at YE 2019:

Since that time, net debt has declined by $450 million. So really the difference in total enterprise value today is about $100mm, or a buck a share.

There are lots of ways to think about that comparison. A few are:

SBLK had no FCF yield in 2019 vs. a 30-40% FCF yield today

SBLK paid a 5c dividend in 2019 vs. a $1.90 dividend today

Second hand vessel prices are about 50% higher today than they were then

CONCLUSION

This isn’t a blow your socks off kind of idea. It is also probably not an immediate buy. SBLK could easily go back into the $16s in the next few weeks or months if the market doesn’t leg higher.

And look, there is no getting around that the whole idea hinges on the economy not deteriorating significantly. You can’t deny that risk. The bulkers are screwed if we get a global recession.

But if we aren’t going to have a significant recession it just seems like this stock is likely bottoming at this level. And with the fleet growth muted and interest rates high to deter new entrants, there are some levers to make me think a cycle up could come quite quickly.

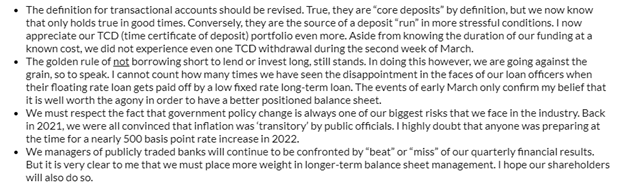

Bank7 got hit in March, along with the rest of the banking sector, but it never really traded down close to its 52-week lows. It corrected, but the move in the stock looked more like volatility than any real secular change.

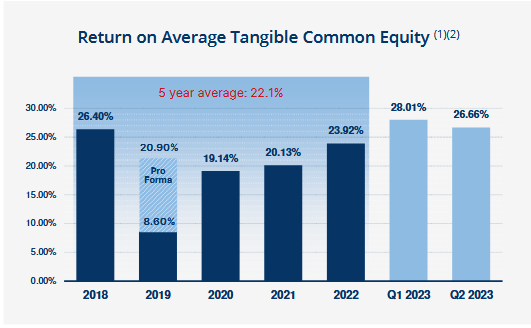

That is probably for good reason. Essentially it comes down to this. For the last 5 years Bank7 has been averaging 22.1% return on tangible common equity. Those returns even accelerated in Q1 and Q2 of this year.

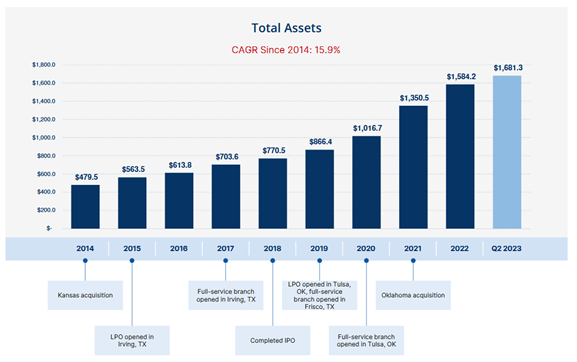

Since 2014 Bank7 has grown assets at a 15.9% CAGR. Most of that organically, as this has only included a couple of acquisitions.

Bank7 managed through COVID and now through inflation and they just keep growing. That has left them with a nice problem, which they articulated on the last conference call:

In the current moment of high interest rates and a (surprisingly) strong economy, Bank7 fits my criteria of a bank that should do well. They are heavily weighted to the loan side (as opposed to securities), to variable rate loans, to the type of loans that will hold up better in a good economy, and the loans they are making are at 8%+ rates.

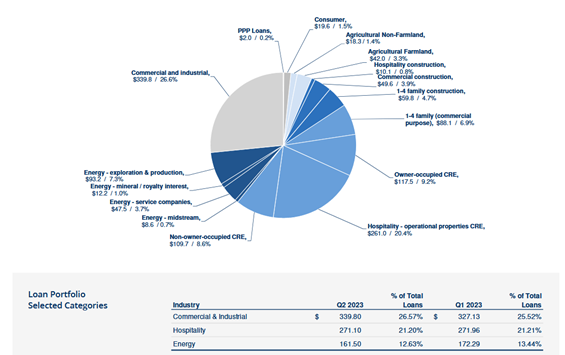

Of course all this means the loans that Bank7 makes are riskier than most. There is quite a bit of energy and quite a bit of hospitality CRE in their portfolio. In a bad economic environment those could cause trouble.

But for now, apart from one outlying energy credit that is going through bankruptcy (and that BSVN expects to recover fully on) their loan book seems to be performing fine.

There’s one large credit, I think that’s out there in the public realm that we really can’t talk about because there’s ongoing litigation. Outside of that line of credit, the energy book is performing very well. I will say that the deal flow there has slowed quite a bit from the pace of last year, and we did contract about. It’s about $10 million during the quarter. I wouldn’t be surprised if there’s a little more contraction as the year goes on in that book, but overall, credit quality there is very strong with primarily companies we bank for a long time.

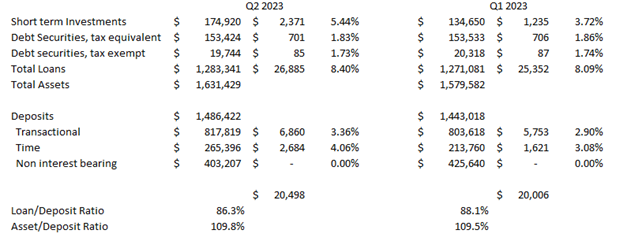

Bank7 Q2 earnings were one of the few bank earnings reports that showed minimal deterioration to the bottom line. Even though they did have a noticeable rise in deposit costs earnings were flat. Bank7 had $1.06 EPS in Q2, essentially the same as Q1. At this run-rate they are trading at 6x P/E.

I found it interesting to walk through Bank7’s interest income numbers in Q2. It kind of highlights how a bank can avoid earnings compression even as its deposit costs rise.

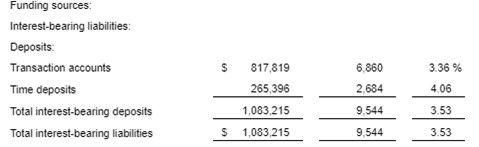

In Q2 Bank7’s deposit costs rose quite a bit. They were far from immune to the repricing of deposits. Their total cost of interest bearing deposits in Q2 was 3.53%. This was up from 2.94% in Q1.

Just purely on cost of deposits Bank7 lost nearly 60 bps of margin. On the surface that would seem a bit worrisome. It had to cut into the bottom line right?

Not so much.

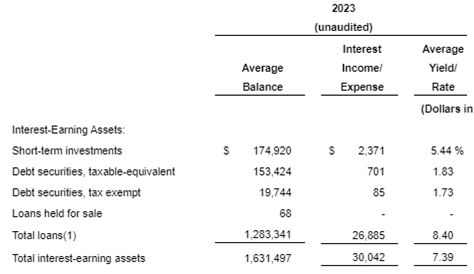

This was, in part, because Bank7’s loans re-rated upwards as well. Their average yield on loans is now 8.4%. That was up from 8.09% in Q1, so up 31 bps.

That loan book repricing is because of variable rate loans. A couple of quarters ago Bank7 put out a slide on their loan book. Three quarters of their loans were variable rate. Some of these loans are hitting a ceiling now though, so I think that going forward the variable-ness of their loan portfolio is less, closer to 50%. But up until now, Bank7 has seen their loan book reprice along with their deposits.

So the loan book re-rating up helps explain why earnings didn’t decline. But it doesn’t explain it entirely. Even with the re-rating of the loan book Bank7’s deposit costs rose a lot more then their loans. Subtracting the interest rate of what Bank7 paid for all its liabilities from the interest rate it got from its assets, you get a spread of 3.85%. This is down 25 bps from Q1 so better than the 60 bps they lost on deposit costs but still not insignificant.

But their actual net interest margin was down only 10 bps from Q1 to Q2. It was 5.04% in Q2 vs 5.14% in Q1. And their net interest income, the dollar amount of net interest they received, was actually up from the first quarter (which is what really matters for earnings).

What sort of black magic is this? How does Bank7 go from losing 25 bps on interest costs to only 10 bps on net interest margin to actually gaining on net interest income?

I talked in prior posts about how well-managed banks can manage their earnings and often they have more levers to pull than they are given credit for. With Bank7 it wasn’t so much lever pulling as them setting themselves up with assets and deposits that match in terms of their interest rate sensitivity, so that even when a portion of those liabilities (the interest bearing deposits) was rocketing higher their bottom line was insulated.

When you look at the interest income breakdown for Q1 and Q2, it really comes down to two things.

First, Bank7’s short-term investments, which is really just their own cash that is held at the Federal Reserve banks, yielded more. They also added to the cash pile by $40mm, which was offset by deposit adds of about the same. This had some impact on the net interest income number.

Second is the “magic” of non-interest bearing deposits. Yes, Bank7 saw the cost of their transactional and time deposit costs rise a lot. But their non-interest bearing deposits were (by definition) still non interest bearing. While some of those deposits shifted from non-interest bearing to interest bearing, they didn’t shift that much. As a result, the rise in the interest earned on their loans and their cash held at other banks more than offset the increase in deposit rates.

Their core NIM, so not including any impact from fees and such averaged 4.66% in Q2 2023. This was only down 5 bps from Q1 after excluding a one-time purchase accounting adjustment. On the call they gave some guidance of what to expect with core NIM.

I’m not sure we’ve ever dipped below about 4.25% or 4.3%. And so there’s nothing that we see today that would lead us to believe that we’re going to operate outside of those ranges. And I’m not saying that we’re going to go from 4.55% real time today to 4.30%, but if it happens, it happens.

Their worst case scenario NIM is a drop to 4.25%-4.3%. Their core NIM right now is 4.55% which means worst case it drops down somewhat but still pretty strong. Moreover, 4.55% is their “real time” number and the number they say to use going forward. Which suggests (and this is an important point) they have an expectation that we’re at the bottom.

But even with some continuing slippage in their margins, I don’t see much of an impact on earnings at all in Q3. I modeled out Q3 assuming their overall NIM drops from 5.10% to 4.9%. That assumes they see another, albeit smaller, drop in non-interest bearing deposits in Q3, that the re-rate on their loan book is less than Q2 and that their loan to deposit ratio stays flat. I get earnings of $1.02 EPS, which is a drop for Q2 but not much of one.

Bank7 could manage this to be even better. By simply adding a smidge of growth to their loan book – say 2% sequentially, something that would only move their loan to deposit ratio up from 84% at end of Q2 to 85% – they could offset that drop entirely. And given that their transactional and time deposit costs were already at 3.36% and 4.06% on average in Q2, there isn’t a lot of room for these to go much higher. In fact some of those time deposits might be looking favorable as the Fed has raised rates again and loans are probably in the mid-8s or higher right now.

Is Bank7 a compounder? It seems like I am likely to only really know this after the fact. As someone who is more of a generalist, who cannot know all the intricacies of the Oklahoma market or Bank7’s reputation there, I can only make an educated guess. Banking is a little trickier in this regard than other businesses. While it is relatively straightforward to evaluate a business’s product or service and its enduring value to customers, the value of a banks product, its loans, can only be known for certain in retrospect, after the loans are shown to be good and repaid. All I can say is so far, Bank7 has the earmarks. And they certainly think so:

As I have dug into the bank stocks over the last few months, one thing that has crystalized for me is the importance of flexibility.

Apart from a few banks that aren’t really all that reliant on deposits, usually because they have other ancillary businesses that drive their income or because their loans are high-risk and what they pay for deposits is not that important, pretty much all the others are in the same boat. Rising deposit costs and worries about commercial real estate dominate the risks.

What differs, sometimes significantly, is how much flexibility they have to deal with issues as they arise.

Eastern Bankshares is interesting for this reason. On the surface EBC has many undesirable characteristics. I can make a good case for why you would not want to buy this bank. Yet if you look a bit further, EBC has one big thing going for it – flexibility – and that makes it pretty interesting, and I think could allow it to outperform.

What might make you skittish about Eastern Bankshares? For one, EBC has a very narrow net interest margin.

Net interest margin is the difference between the yield on assets (loans and securities) and the cost of deposits. Narrow is bad, particularly today.

EBC’s net interest margin has been well below 3% each quarter for the last year. That is pretty low. I talked about this in my last post. I consider a NIM in the 3%s to be on the low-end of acceptable, and in the 2%’s I get nervous.

Having a tight NIM puts a bank in a tough position right now because they are more susceptible to rising deposit costs. It is ironic that, as long as the economy is strong, it is actually safer to be invested in more risky, and higher interest, assets.

For example, if you are a bank invested in nothing but credit card loans at 19%, does it really matter much if your deposit costs go from 2% to 3%? Nope. But if your loans are low-risk real estate in the 4% range, it matters a lot.

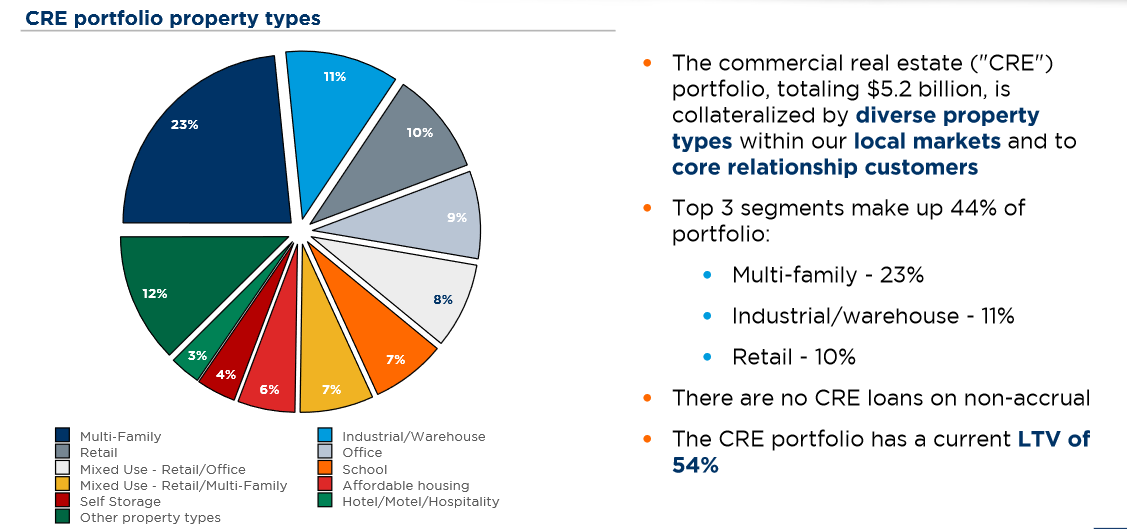

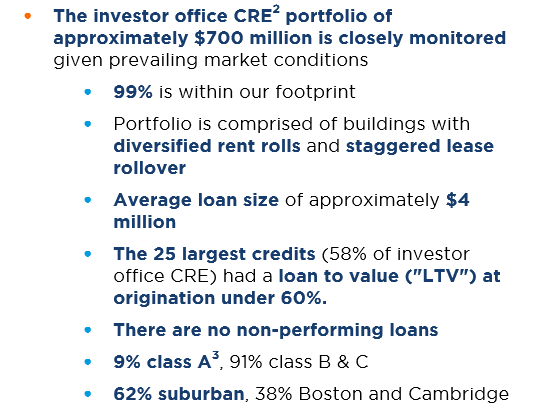

The next thing about EBC is that they have a relatively large commercial real estate portfolio.

EBC operates in “the greater Boston area, specifically eastern and central Massachusetts, southern New Hampshire, including the seacoast region, and northern Rhode Island.” Much of their loan portfolio consists of commercial real estate in this area.

Of that CRE portfolio, office is a decent chunk. Their office loans make up 9%. Mixed use office + retail make up another 8%.

The composition of those office loans is average at best. It is 2/3 suburban (so not big towers) but there is very little in the way of Class A properties.

EBC did say on the Q1 call that they don’t consider any suburban office to be Class A so that makes the Class A/B,C breakdown look a little bit worse than it actually is. But still, if 9% of their office loans are Class A and 38% of office loans are non-suburban, you can do the math. They certainly have some exposure to downtown Class B and C properties, which is where most of the CRE stress is.

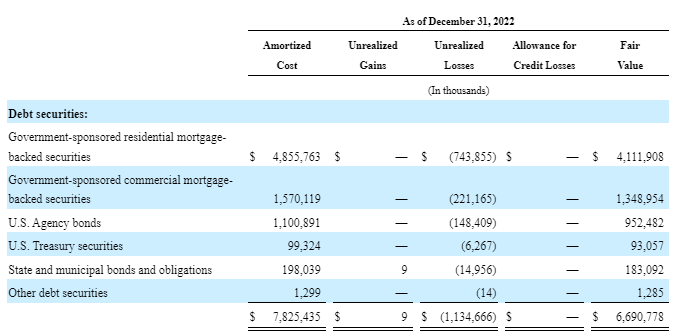

Finally, and this was the big worry going into 2023 – EBC had a big underwater securities portfolio. At the end of 2022 their available-for-sales securities portfolio was $6.7b and had a $1.1b unrealized loss on it.

The securities portfolio was 30% of assets, which is sizable. And compared to their $1.8b of tangible equity, the $1.1b unrealized loss was quite large (though because this is an AFS portfolio of securities, the loss has already been subtracted from tangible equity).

Ok, so those are the negatives. Why in the world would I find this bank interesting?

Flexibility!

It starts with what EBC did with their AFS securities portfolio. In March EBC sold a big chunk of it. They ripped the proverbial band-aid off.

EBC sold $1.9b of securities during Q1, taking a loss of $280mm after-tax in the process.

Here is where flexibility comes in. The reason EBC did this is because they could. I have already explained how EBC positioned themselves poorly by buying a whole bunch of low yielding securities. But they made up for this guffaw in another important way: by not levering up the bank risk and keeping around lots of excess capital.

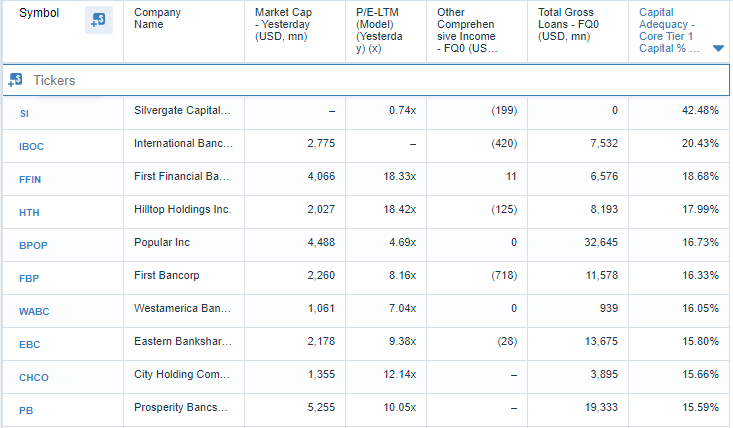

EBC has more capital than most banks. The median KRE bank has core tier 1 equity ratio of 11.12%. EBC has a CET1 ratio of 15.8% and that is after the sale of 25% of their security book. EBC would stand 6th in the KRE in terms of CET1 ratio:

Second, EBC is not a very levered bank. They have a loan to deposit ratio of 72%. As I noted in my last post, a loan to deposit ratio in the low 70s is on the low-end of banks. It is also far below where EBC was before COVID. Their loan to deposit ratio was 93% at YE 2019.

Having more equity at a time like now gives a bank options (you could say optionality but I hate that word). Options like taking a loss on a security portfolio that is yielding only a bit over 1%.

And if you can do that, you get even more options. Because now you can replace that asset with something yielding much more. Or you can remove some of your highest-cost borrowing.

After the securities sale EBC had cash of $2.1b. This is about 10% of assets. It is way, way higher than it needs to be for a bank in normal times. On an exchange with an analyst on the Q1 call EBC said they can reduce their cash level substantially:

Historically EBC has operated with a couple hundred million of cash. Right now, the sweet spot probably needs to be higher than that historic number, but still nowhere near $2.1b.

At the very least, EBC can use some of their cash to pay off some of their high-cost funding. If you look at EBC’s balance sheet in Q1, they had $1.1b of FHLB advances and another $1.97b of CDs:

The FHLB advances have an interest rate of 4.6%. The CDs have an average interest rate of 3.7%.

It is fair to assume (because they said so themselves) that EBC will use most of the cash to wipe out all their FHLB advances and let some of CDs run-off through to the end of the year.

Eliminating the FHLB advances alone would have a big impact on earnings. In my model of Q2 earnings, I calculate that simply moving excess cash to get rid of the FHLB advances (for the whole quarter) would move earnings from 29c EPS to 38c EPS. Not bad.

CD run-off would help even more. Because EBC has a low loan to deposit ratio, they can afford to let deposits run off without doing anything on the asset side. The only thing is that I’m not sure whether a run-off of CDs will just be offsetting other deposit mix shifts from non-interest bearing to CDs, meaning cost wise its a wash.

EBC had planned to use the cash right away to pay off high cost funding but the banking panic delayed that. On the Q1 call EBC said that after the banking panic in March they had decided to keep the cash on their balance sheet until things settled down a bit. My best guess is that we will see the cash be put to better use in the second half of this year (but I’d be pleasantly surprised if it happened sometime in Q2).

Once they do, earnings will benefit.

Which is why EBC was able to do something that few banks are doing right now. Raise guidance.

EBC said that they expected their net interest margin to increase through the rest of the year:

There aren’t too many banks that are seeing net interest margin going up. In fact, the late-quarter conference appearances of banks that I listened to had most of them making reductions to their Q2 NIM guidance.

Now remember, EBC is no perfect bank stock. Their CRE and in particular office exposure could be a problem. But even that might not be as bad as it looks. This Bloomberg article pointed out that Boston is one of the better performing cities:

These charts from Morgan Stanley, albeit from earlier this year, also show Boston performing well compared to other major markets.

EBC is a lesson I think – of what flexibility can mean for a bank. It was a bank in a tough spot to start the year. But they had one trick up their sleeve: they began the year with the flexibility that comes from having low leverage and excess capital.

They used some of that capital to take a loss on extremely low yielding securities, which in turn gave them the flexibility that comes with cash. Now they seem likely to use that cash to de-lever even further, reducing their high-cost borrowings.

But again, they have flexibility. If the economy accelerates there is nothing to stop them from deploying that cash into loan growth, where they could likely get 7%+ on new originations, which would be even more accretive to EPS than paying down the FHLB. Remember that EBC has a loan to deposit ratio of 73% vs. 93% pre-COVID. There is plenty of room to grow their loan book if they believe the economy supports it.

I research a lot of stocks. But I don’t write about most of them.

This is because most research leads to bland conclusions that aren’t really all that inspiring to write about.

For example, I spent a lot of time over the last two days learnign about Fastly. I wrote 4 pages of notes. I went through their investor day presentation, listened to the whole thing. Went through their last couple conference calls. Made a model.

But I’m not going to write about it. There is not much to say. At the end of the day, Fastly is going to be marginally profitable in 2026. If the stock got down far enough (maybe $12) I might buy it. But it would probably be for a trade. Fastly trades at 13x their long-term goal operating income, which might happen before the end of the decade. It’s a company worth following, but not exciting enough to write about.

To make an idea worth writing about you need some sort of tension. Someone is right and someone is wrong. Someone is missing something and here is what it is.

Otherwise, it is just Fastly should grow at blah, blah, blah and that gives us a positive operating earnings by blah, blah, blah and the discounted cash flow model says blah, blah, blah.

Boring.

Right now, a lot of my research is banks. Which is essentially me doubling up on the boring-ness. But there a few that make a good story.

There are two I plan to write about. Eastern Bankshares and Preferred Bank. This post is about Preferred Bank.

What makes Preferred a good story starts with it being a California bank. That puts it in the center of the crisis and a sorta-ish peer to other banks that have failed: SIVB and FRC.

Preferred operates in Los Angeles, Orange and SF counties. They also have one branch in NY. They are headquartered in Los Angeles.

Preferred was square in the headlights over the last couple months and you see that in the stock chart.

Top to bottom, Preferred’s stock price dropped 40%.

The other thing that makes Preferred a good story is that they exemplify a theory of mine. That’s right, I have a theory. It is unproven. My theory is that all regional banks are not actually the same.

While the word “regional banks” has come to denote the group as a whole, essentially a Borg, it is my postulation that this characterization is missing in nuance.

It is just a theory. It is not widely accepted.

Let’s look at Preferred. Preferred is not the perfect, riskless, bank. This isn’t a story about that. It has risks. But most are different risks than say, FRC or SIVB. This is a story about how Preferred is very different than the two banks in California that failed.

THE BANK

Preferred was founded as a Chinese-American bank. They have evolved past that, they say they serve the “mainstream markets” of their areas, but they still benefit from migration from China and other parts of East Asia and I suspect a lot of their lending is to this demographic.

Geographically Preferred was in the middle of the crisis. That made those few days in March some tough days. The CEO Li Yu gave a lesson learned in the Q1 press release.

Nevertheless, the bank had a good first quarter. They had earnings of $38 million, EPS of $2.61 per share. Earnings increased 46% YoY but were $1.5 million less than Q4.

In Q1 Preferred had an extremely high ROA of 2.41% and an ROE of 24.47%. Their efficiency ratio in Q1 2023 was 26%.

While this performance was on the high-side of their historical results it was not that unusual. Historically Preferred has been a very strong performer, especially since 2017.

Return on assets since 2017 has been above 1.5% and return on equity above 15%.

Over the last 9 years Preferred has had an earnings CAGR of 22.5%. That seems pretty, pretty good. I’ve never quite been able to figure out banks in this respect. Earnings CAGR is earnings CAGR right? Yet banks that grow earnings by 20%+ for 10 years barely a get multiple above 10x.

Of course, I am comparing banks to the real world. In the bank valuation world the market has rewarded Preferred’s performance with a generous multiple well above tangible book value – generally between 1.5x and 2x, with a P/E of in the lofty range of 12-15x!

Now before I run away gushing about the bank performance, Preferred hasn’t always been an outperformer. During the Great Financial Crisis (GFC) Preferred did very poorly. They are California based lender, which was ground zero of the housing crisis. But what made matters worse is that Preferred lent to single family home builders. Obviously when the housing market turned, being long land and new construction housing in California was a disaster.

So take that for what you will. Either a harbinger of what may come or a lesson learned. They have made a point on past calls to say they keep construction loans below 10% nowadays. Though, as I will point out, their loan book is not without risk.

Preferred did seem to out-earn in 2022 and Q1 of this year. This is likely due to the interest rate lag (loans getting repriced right away while deposits reprice slower). But even if you plug in their historic ROE of 16.5%, in 2022 Preferred would have had $7.13 EPS – which at even 10x earnings would still be a $70 stock.

My conclusion? Since the GFC, Preferred has done well. They have a 10 year track record of growth. They seem like a well-run bank. They’ve certainly been a growing one, as assets have expanded about 4x since then.

THE LOAN BOOK

But FRC and, to a lessor extent, SIVB, were also well-run banks.

What makes Preferred different?

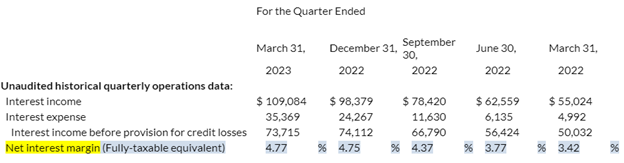

The first and main difference are what Preferred’s assets are. You get a hint that something else is going on when you look at their large net interest margin (NIM).

Preferred’s NIM has expanded every quarter since Q1 2023. It was 4.77% in Q1 2023. That is a high NIM. One of the highest. Remember that big banks like Comerica and Fifth Third have NIMs in the 3s. Keybanc is actually below 3%.

The big reason that Preferred has such strong NIM is that almost all their loans are variable rate loans. From an analyst question on the Q1 call:

I just wanted to get an update on kind of the health of your variable rate borrowers given that you got 80%, 85% of your loans variable rate, you’ve seen loan yields up 300 basis points from the lows.

Being so levered to variable rates means that Preferred is largely benefiting from the Fed tightening.

This is a bank that should like higher rates. If rates go up virtually their entire loan book reprices up. Their deposits? They will reprice higher too, but not nearly as much.

Think about it this way – banks are all talking about deposit betas. Analysts are fretting that deposit betas are now rising to 45 or 50. Everyone has been freaking out about that.

What this is really saying is that the deposits will reprice to 45% – 50% of the rise in the Fed Funds rate. Which is a lot higher than what was being said a quarter ago. But for Preferred, their loan book is already repricing 80-85% of the Fed Funds rate. They have a loan book beta (I’m making this term up) of 80-85.

That is not to say that Preferred doesn’t have rate risk with the loan book. It does. But it’s the opposite risk. If rates come down, those loans will price down immediately and deposits will likely be more sticky.

The other risk, which is also a real one, is that their gain is their customers loss. Their customers are hurting by paying high variable rate loans. Now Preferred says this isn’t a problem, that all their clients are dealing with the higher rates, but you have to wonder how much stress it is causing.

Regardless, this is a bank that is geared to higher rates. So you would think that when the Fed talked about raising rates further that would be good for Preferred.

Yet what did the stock do after Powell talked rates up this week?

It went straight down with all the other banks that are negatively correlated to higher rates.

Ok, so that’s the rate sensitivity of the loan book at a glance. Now let’s look at the loan composition.

First the bad news. Exhibit A: their loans are largely real estate.

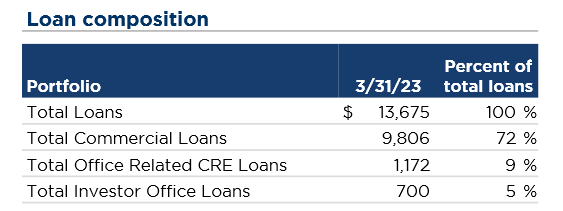

Exhibit B: Of those $3.4b of real estate loans, $2.8b are commercial real estate. And of that, Preferred has 10% of their loan book in office, or about $500mm. This is quite a bit.

But just like all banks aren’t the same, all CRE is not the same and neither is all office CRE. Where is Preferred’s office CRE?

First where they are not. They are not in downtown Los Angeles and only a very small amount is in downtown San Francisco. They said they have one $8mm loan in SF which is not really made to anyone in the office-space maelstrom:

Of this amount, roughly $8 million is in the downtown area. We have faithfully have tried to avoid especially Los Angeles urban area for the past 20 years. And most of our office properties in the suburban area that in California, especially in Los Angeles, it’s a big, really suburban area. So there’s little communities everywhere and basically the property there is a lot more stable than the downtown area. And when we have the $8 million in downtown area is really in San Francisco that was leased and in the long-term lease to, I think, one of the famous university over there. It is very, very, how should I say, underwritten quite well is loan-to-value ratio probably less than 40% in any event.

Their office portfolio has an average LTV of 61% and average loan size of $4.1mm. The largest 3 loans average about $40 million a piece.

Preferred went into a lot of detail on their top-4 office loans on the call:

The office building that is — one of the office building in the $50 million range is in one of the hottest areas in Los Angeles core, Culver City, which we have the creative and entertainment district, the first floor are all upscale — I mean they have upscale, good restaurants that do a bustling business. The second third floor is rented out to a new credit card type of company with LC support from a major bank. So that’s one. And also that we have a very rational, very reasonable sponsorship behind it.

The next largest one is in — is one of the buildings in Koreatown, the owner of that is rearranging the office building, making that office building near fully occupied and underwritten.

The owner of this office building is very, very, very substantial, very, very successful. And his credit in Los Angeles is it’s tough notch. Okay? Its cash flow is huge. So these are the top 2 as you have wanted to know, okay?

And I might explain the third one is in a very rich area of Newport Beach, where a group of people bought office building and my view, that group of people have dealt with us for many, many, many, many projects there. And a substantial group of people bought the office building and vacated everything and it’s going to demolish it and convert into apartments.

The fourth biggest office building is in the same category as the third. It is being torn down to put up condos.

To sum that up: of the four biggest buildings, two of them are really construction loans where the office buildings are being torn down for condos. One is a three story building in Culver City, a “hot” area of LA’s entertainment district with upscale restaurants and then offices above rented out to a credit card company. And the last is in Koreatown and is fully occupied.

Just generally on how their credit is doing, Preferred said they “don’t have any nonaccrual or classified or even 30 to 89 days…in the office sector”. There are no immediate credit concerns at least.

That doesn’t mean there won’t be though. The real risk with Preferred is credit risk – in a downturn. Banks are all about trade-offs and the trade-off Preferred makes is take rate for risk.

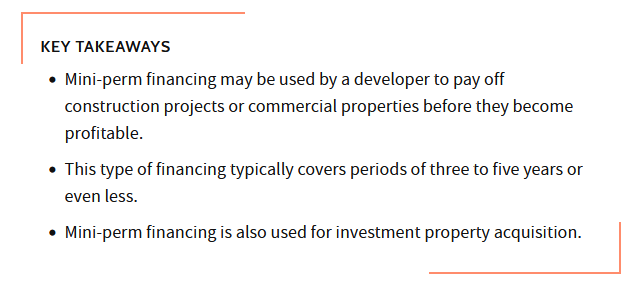

Preferred has reduced their exposure to construction loans since getting bowled over in the GFC. But they remain a heavy lender of real estate perm-loans.

Perm-loans are bridge loans made after construction. They are short term (3-5 years, thus the term mini-perm which is short for mini-permanent).

These are higher risk loans because they are being made to newly constructed buildings that are not yet occupied. There is no cash flow at the start.

Mini-perm loans are about 60% of Preferred’s book. In a true downturn, this is definitely a risk.

So it’s not that there isn’t risk with Preferred. It is just that it is not at all the same risk as SIVB or FRC. And Preferred shouldn’t be trading in lock step with fed funds, as if it were a bank that had half their portfolio in mortgage-backed securities.

Speaking of securities. Preferred is the opposite of the failed banks. While SIVB and FRC owned a lot of government securities, Preferred doesn’t own much at all:

Preferred has a grand total of $400mm of securities at fair value. $40mm of embedded losses. The entire value is less than 10% of their balance sheet. They have more cash than securities.

Given the lack of securities, they really don’t lose any meaningful book value (real or marked) on rising rates. Which is kind of the point here. This bank has positioned themselves to rising rates. Yet the stock is behaving like they aren’t.

DEPOSITS

On deposits, Preferred is like other banks. Deposits are the one place where all banks (other than the largest regionals – like PNC and the money center banks like BofA and JPM) are the same. All banks are experiencing higher deposit costs, fewer non-interest bearing deposits, and more CDs.

Preferred’s non-interest bearing deposits declined in Q1 2023. Their non-interest bearing deposits are below anywhere they have been in the last 10 years.

And that has impacted their cost of deposits. Preferred’s cost of deposits rose to 2.49% in the first quarter.

Preferred said on the Q1 call that in March their cost of deposits was 2.63%. That means average costs for January and February was 2.46%. It looks like their Q4 2022 average rate was 1.66%.

The conclusion? Deposits costs are most definitely increasing. But that March number is not crazy high. And given their loan book, it is going to take a much larger rise in their deposits to really bite into their earnings.

Being in California, Preferred did lose some deposits during those few days in March after SIVB collapsed. But they have already gained some of those back. From their Q1 call:

During the 3 days in March, March 9, March 11 and March 12 and March 13, okay? The 3 working days. Preferred Bank also experienced deposits outflow. The good news is we have a total of less than 10 accounts that pull the money out. The bad news is that 3 of them is very precised. For the quarter, our deposit reduced or decreased by 2.7%. As of yesterday evening, which is April 18, we have our deposits increased 1%, back increased 1%.

FWIW they are still advertising for new accounts at pretty decent rates. But so is just about every other bank not named JP Morgan or Bank of America (though I read even that is changing). So I don’t really know if this is saying as much as some suggest:

SUMMING IT UP

There are two points I’m trying to make here.

First, there is more nuance to banks than is given credit for. All banks have risk. But those risk are not all the same. Not every California bank should be lumped in with FRC and SIVB just because they are in California. I was listening to the Michael Campbell show this weekend. He had Jim Thorne on, who btw made a nice case for a continuing bull market. But at one point Thorne and Campbell start talking about regional banks, and it was the usual: The banking crisis is not over… commercial office buildings with loans coming due… there will be defaults… all of this falls at the feet of the regional banks. It was the usual refrain.

Everyone talks about “regional banks” as though they were some kind of monolithic entity that moves as one. The Borg.

Yet here is a bank that a Raymond James analyst said was “one of the most rate-sensitive banks around”. Like I said at the start, between 80-85% of their loan book is variable rate. Is this really the same risk?

My second point is rather simple. Preferred is a bank with a 10 year history (really more) of growing EPS and the last 9 years it has done that at a 22% CAGR. A week or so ago you could buy Preferred at about 1x TBV and well under 10x PE. Today it is 1.1x TBV and still well under 10x PE.

In a world where tech is valued at well over 10x sales for a revenue CAGR that is equal to or less than Preferred, and even after considering the risks in office, the risks in deposits, the risks in California, that doesn’t seem like a bad price.