Gran Colombia’s Debenture Redemption looks favorable

On Thursday Gran Colombia announced the warrant terms of a $152 million USD senior secured note offering. Attached to the notes the company is offering 124 warrants priced at $2.20 per share per $1,000 of note principle.

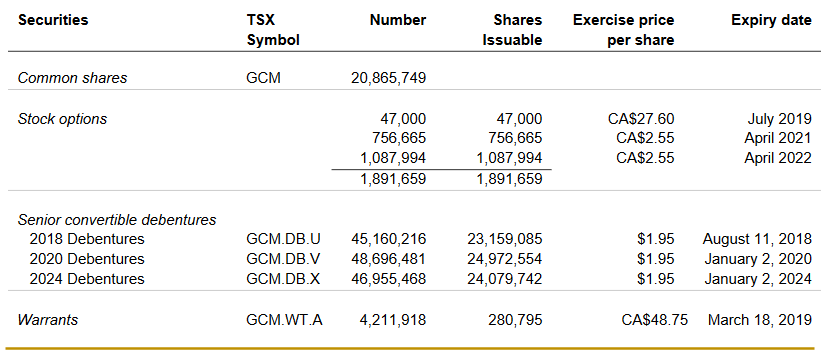

Dilution amounts to 18.8 million shares. This compares to 72.2 million shares that would have been issued under the existing 2018, 2020 and 2024 debentures if they were fully converted (the table below is from the third quarter MD&A filing).

I think the deal, if it is approved, is pretty positive. Consider:

Under the prior share structure, a $2.50 share price translated into a market capitalization and enterprise value of about $230 million (~92 million x 2.50 = $230 million).

Under the new notes, and considering redemption of all of the existing debentures at par, the share count is roughly 39 million and the market capitalization is $97.5 million (39 million x 2.50). The enterprise value is $202 million (97.5 million + $150 million (x 1.25 CAD/USD exchange) – $45 million (assuming in the money warrant conversion of the 18.8 million warrants) – $9 million).

Debenture Holders can participate

As a debenture holder (I own both the stock and some of the X and V debentures) I’m interested in what my options are with the debentures.

The terms gives existing debenture holders the right to participate in the offering:

Existing holders of the Company’s Outstanding Debentures that are eligible to participate in the Offering may (subject to complying with certain procedures and requirements) be able to do so by directing some or all of the redemption proceeds from their current debentures into Units on a dollar-for-dollar basis.

I’m not entirely sure how to read this. Does it mean that existing debenture holder gets preference to convert their debentures into new notes or is this just on a best efforts basis where an over-subscription to the notes would mean partial allocation?

I’m hopeful that I can direct my debentures into the new notes, but I’m not counting on it.

Its still cheap on Comps

Gran Colombia continues to compare favorably to other gold producers.

One of the quick scans I like to do compares companies on a simple EV/oz produced basis. I’ll do the comparison and then weed out why some companies trade at lower multiples than others. Usually there are good reasons.

At $1,400/produced-oz Gran Colombia trades at one of the lowest multiples of the group. Only the really poor operators that are cash flow negative at current prices (an Orvana Gold for example) are cheaper. Most of the companies I compare to are in the $4,000 – $6,000 per produced-oz range. Even the lower tier companies like Argonaut Gold or the struggling one’s like Klondex trade at over $2,000 per produced-oz.

Its still cheap on Cash flow

Even forgetting that it is a gold stock, Gran Colombia remains reasonably priced as a business.

On the third quarter conference call Gran Colombia reiterated guidance for $16 million USD of free cash flow in 2017. In the fourth quarter they produced 51,700 ounces versus an average of 40,700 ounces per quarter in the first three quarters.

The indication after the strike at Segovia was that new agreements with artisanal miners should lead to more processed ore at the plant. Based on this and progress at the Segovia mine, my expectation is that 2018 free cash guidance will exceed 2017.

I suggested in my original post on Gran Colombia that I thought $20 million USD of free cash flow was not an impossible goal. I still think that’s possible. Assuming the note and debenture deals go through, the market capitalization of the company will be a little under $100 million CAD at current prices. Even though the stock has climbed since my original post, this still means the stock is at less than 4x free cash flow.

Conclusion

Eventually the note offering and debenture redemption should be positive for the stock. But it might take a few months.

What’s tricky is that at $2.40 the stock price is right about where the debentures convert. It isn’t really in anyone’s interest (other than the current debenture holders, though even that is debatable) to see the stock price rise too much above the convert price until the deal is done.

I’ve been adding to Gran Colombia all the way from $1.40 to $2.20. I see no reason to take any off the table yet. The company is doing everything right so far. Hopefully with the new capitalization and simpler structure the market will continue to recognize this.