Buying Gran Colombia Gold, A Levered, Free Cash Flow generating Gold Producer

I like the looks of gold right now. Short positions in the metal have been climbing for a number of weeks. Fred Hickey (of the High Tech Strategist) tweeted on Friday that “gold large spec future shorts at 157.4K contracts are second highest on record”. Anecdotally, the charts of many of the gold mining stocks have been depressed for some time. Often July is a seasonal turning point for the miners, as they perform well into the second half.

I took positions in Argonaut Gold and Klondex Gold a few weeks ago. Argonaut worked out, and I actually sold some of my position last week, but Klondex has not. To be honest, the more I look at both of these names, the less excited I am about them. They haven’t generated free cash in the past, so their projections about the future leave me skeptical. I have been searching for other ways to play gold (in addition to Gran Colombia I have bought Rox Gold and Americas Silver).

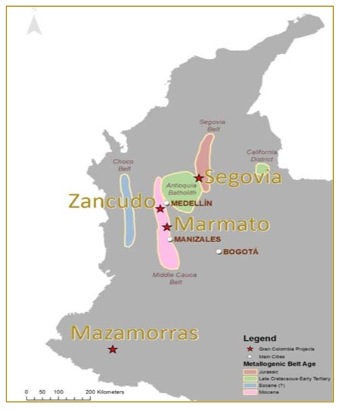

I found out about Gran Colombia from this tweet from Brown Marubozu. They are a tiny gold producer with two mines in Colombia. They operate the Segovia mine and the Marmato mine. They also have an exploration project called Zancudo.

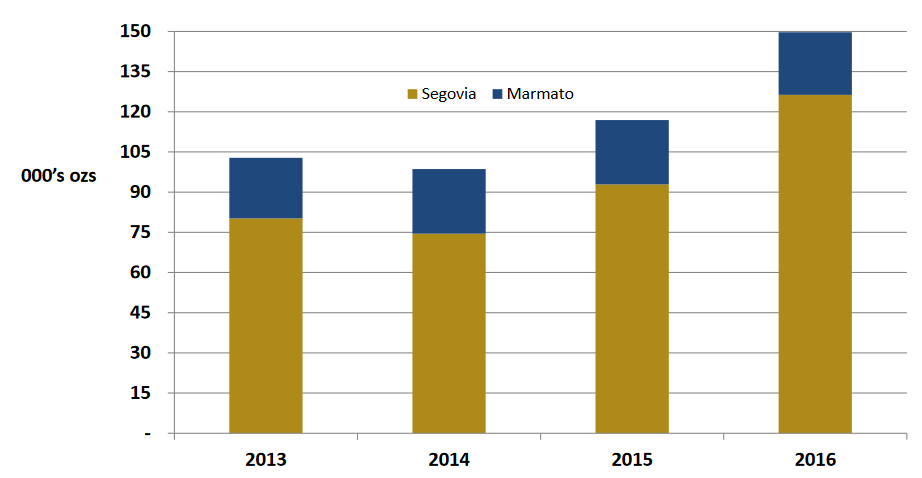

The Segovia mine is by far the bigger of the two mines. It produced 126,000 ounces in 2016. Marmato produced 23,500 ounces.

Costs at Segovia are much lower than Marmato. In 2016 cash costs at Segovia were $655 per ounce while Marmato cash costs were $981 per ounce. The company doesn’t break down all-in sustaining costs (AISC) on a per mine basis but over in 2016 they had AISC of $850 per ounce

For 2017 Gran Colombia is expecting production of 150,000-160,000 ounces of gold and AISC are expected to be under $900 per ounce. The rise in costs is because of more exploration at Segovia and a higher Colombian peso. AISC of $900 per ounce and under makes them a relatively low cost producer.

Debt and Cash flow

Gran Colombia is heavily indebted compared to most gold miners. The company has $145 million of debt outstanding, denominated in US dollars. They have 20 million shares outstanding.

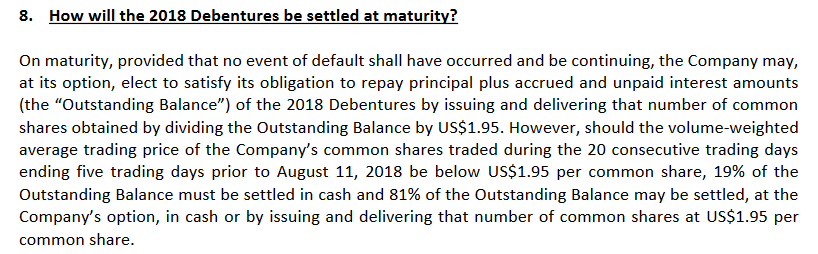

However, looking at nominal debt and shares outstanding is a bit misleading. The outstanding debt is comprised of 3 convertible debentures. There is a $46 million 2018 debenture, a $52.4 million 2020 debenture and a $47 million 2024 debenture. All of the debentures are convertible at $1.95 per share.

The 2018 debentures have a unique feature that I have not seen before. If the share price of Gran Colombia at the debenture maturity is less than $1.95, the company has the option to repay up to 81% of the debentures with shares at $1.95. It’s a very odd clause, and it factors into debt and outstanding share calculations. . Nevertheless it is clearly stated in note 8 from the debentures FAQ:

The 2018 debenture pays only 1% interest.

The reason that the 2018 debentures have such a strange structure is because they are the result of a restructuring of debt in early 2016. The company exchanged two sets of existing notes (called the silver and gold notes) for debentures and shares. The silver notes, which presumably were subordinate (I admit I haven’t looked into all the details of the old securities) were given poorer terms than the gold notes, including this odd repayment clause. The 2020 and 2024 debentures, which are the successors of the gold notes, are payable in cash at maturity and carry an interest rate of 6.5% and 8.5% respectively.

Assuming the conversion of 80% of the 2018 debentures into stock at $1.95 per share, the true amount of shares outstanding is 39 million, so a market capitalization of $58 million. Likewise, true debt is $108 million USD, which is still a lot of debt, but not quite as much as it appears at first glance.

How about Cash Flow

Gran Colombia has a lot of debt but they also generate a lot of cash flow. Looking at cash flow from operations before working capital changes and capital expenditures, I calculate that the company generated $17 million in free cash flow (I am calculating this before working capital changes, just to be clear) over the last four quarters. In 2017 the company has given rough guidance (slide 19 of this presentation) that “excess cash flow” will be “at least” $15 million.

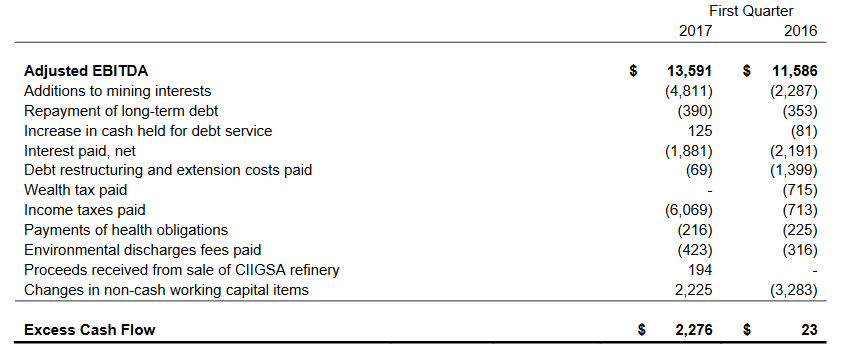

I actually think that may understate free cash flow. The company includes debt repayments as part of their calculation of excess cash flow. Below is a reconciliation of excess cash flow to EBITDA for the first quarter of 2017. Note that excess cash flow is calculated after subtracting $390,000 of debt repayments. This repayment is likely to a small term loan they have with a Colombian bank that is paid down on a quarterly basis. There is $700,000 remaining on this loan that will be repaid this year. True free cash flow would be $1 million higher after accounting for this.

Guidance suggests that excess cash flow may exceed the $15 million minimum that the company has guided to. The midpoint of the company’s production guidance is 155,000 ounces for 2017. AISC is expected to be $900 per ounce. At an average price of $1,200 per ounce gold, the company generates an AISC margin of $300 per ounce, or $46.5 million. If I assume the same level of cash interest and cash taxes as 2016 I deduct another $26.5 million. This would leave $20 million of excess cash flow.

The company is likely to have a very strong second quarter. On the 12th of July the company announced second quarter production of 46,000 ounces. This is significantly above the 39,000 ounces that they produced in the first quarter and is more than 10% higher than any quarter in 2016.

Summing it up

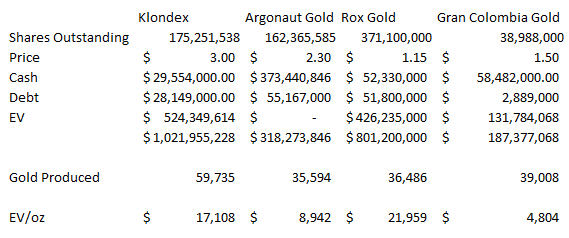

I find it very hard to resist a gold miner trading at less than 4x free cash flow (I’m using a market capitalization of $60 million Canadian which includes conversion of the 2018 debentures and free cash flow of $15 million USD for 2017, which I believe to be conservative). To say it is unusual to find a miner with this sort of free cash yield is an understatement. Unheard of is more like it.

Gran Colombia compares well to the peers I have looked at. Below is a table of 4 other gold stocks that I liked because I didn’t think they were exorbitantly expensive. Gran Colombia is the cheapest of the bunch.

However I know there have been issues with management. They clearly got themselves into way too much debt and had to restructure once already. The shares had to be consolidated due to the fall in the stock price. Management may be the Achilles heel of the idea. But the last few quarters they have produced solid, if not stellar results. So maybe the past is the past.

I also understand that the debt level remains quite high. It makes them a leveraged bet, no question. And that leverage can go both ways if they fail to perform. However because it is convertible debt, it can easily play into the company’s favor if the stock price moves up.

Let’s say the stock goes to $2 USD. I have a nice return from my recent buys (60%). The convertible is now in the money and is exchanged into stock at $1.95 USD. The result is dilution of 55 million shares. Total shares outstanding are 94.4 million, so the market capitalization is $190 million. Free cash flow increases by $10.5 million because cash interest goes to zero. So free cash flow is somewhere between $25 million and $30 million.

At this point, do you think a gold miner with $25 million plus in free cash flow and no debt is going to trade at a multiple of 7.6x FCF? I highly doubt that. The reality, whether you agree with it or not, is that historically gold miners trade at above market multiples. Most miners (at least those not currently at depressed levels caused by in discriminant GDXJ selling), trade at 10x operating cash flow, not free cash flow.

My point is that the share price could be its own best friend. Confidence that the company can generate the free cash needed to deleverage could quickly cause that deleveraging to occur and in turn cause a revaluation to a level consistent with other miners. I think the path is there. If the company executes, and the gold price stays at this level (or even better, moves higher), I think we will see this process occur over the next 12-18 months.

Hi, just wondering why the shares of this gold Co are losing even though the gold price appreciates.

Its because of the mine strike. Its not their miners that are striking, but local individual miners that they and the gov’t have been trying to negotiate mining rights with. As I look into this further its clear that Gran Colombia has a spotty record with the local miners. I think a lot of investors are wary of the stock because of this concern and this is probably why it trades so cheaply. I’m not sure what ends this discount? I’m still holding though.

Thanks for this report. See you have a good long term record. Gran is a mystery stock, but have bot a lot of it. It simply has the best value metrics of any gold miner out there. Agree with your analysis and am spreading it on SeekingAlpha. I have talked with CFO and think he is sharp.

Their operations have been amazingly good for 2 years now. JMHO the reason the stock is low is because it is low, most investors want momentum and presume if a stock is not going up, there is a reason for that. Often there is not. So when it starts going up it will zoom. As you mention there is an advantage to it being low, allows them to prevent dilution.

What most people miss if it does get big dilution from conversion, that eliminates the debt and skyrockets the book value and aids profits. You do get that so am why am spreading your analysis. A stock selling at roughly 1X FCF is ridiculous.

On USAU the geologist looks great (found out about it here) but some people say the stock is being promoted and rest of management is sleazy. Any thoughts on that?

Also on USAU the memory side, is that providing cashflow for USAU? It is hard to find any books on the stock, maybe some restructuring has eliminated the account history?

Thanks for a great blog, Darp

What has kept my position relatively small here is their track record with local miners. They don’t seem to have worked well with locals. Take a look at the IKN blog and what he has written. I’d be interested in hearing your thoughts. Its given me pause and made me keep a small position only.

Thanks Lsigurd, will check that out. Have asked questions on USAU over there. I have been in Gran maybe 1.5-2 years and been impressed, no hiccups. They have had “mountain of gold” mine semi stolen from them, that is mine they do not have in operation. Not their fault, but CA/Colombia trade deal means gov owes them.

The traditional illegal mining is maybe their biggest problem, again to not see it as their doing, just the situation. Will check out IKN.

Cheers

Hi Lsigurd,

Have checked out that site. Quite a bit of info had not seen before. Maybe worst thing is the guy they hate is still co-chairman. The results is past were terrible, $140 to 1.40 in last 5 years, and it was high cost money losing operation.

In last two years amazingly good results, hence why still in biz and throwing off high FCF. In last 18 months, the stock is up. Had 45 min conversation with Mike Davies the CFO last year. Things have worked out inline with their plans. So major shift from prior results.

On Marmato, to best of knowledge they bot it and gov considered them owners. They do want to mine entire mountain, locals do not want that. Locals use mercury and dump in river and are considered illegal miners by gov. But politics, lots of votes behind locals even though many locals also work for Gran. Best solution? Gov buys out Gran, and treaty with Canada seems to obligate them to pay them back for taking something away.

On Segovia, just amazing results and they keep getting better. That is gov and locals fighting over illegal miners and Gran gets in crossfire. And they have IAM Gold as partner on Zancudo http://www.grancolombiagold.com/operations-and-projects/colombia/default.aspx#zancudo

Am surprised no one has not bot them out yet. Segovia is wonderful mine. The Providencia sub-mine there is runing over 20 grams now. 150 years old too, Colombia mines have amazing long lives, Marmato over 400 years.

Am still positive on Gran, but thanks for info, was not up on some of prior history, and that prior history may be why is so low now.

Cheers

On Marmato (mtn of gold), did not say that right, the mine is in small operation and think they let locals mine it for a cut, but their plan is to open pit entire mountain, and that has no started