Argonaut Gold

Over the past couple months I have put together a fairly decent sized position in Argonaut Gold. I’ve taken advantage of its dip below $5 (who’d a thunk it?) and the stock now makes up my largest gold stock position. In preparation for the companies coming Q3 release (operating results will be released October 15th if history is any guide) this last weekend I sat down and listened to Argonaut Golds Denver Gold Show presentation and re-listened to their Q2 conference call.

Now I want to talk for a second about capex. A lot of the simpler analysis that you will read on the web will provide a valuation of the company on a EV/oz basis. In the case of most micro-cap evaluations (pumping?) this is usually followed by a comparison to the EV/oz value of a number of competitors, and then a conclusion that the stock in question is undervalued by some multiple of its current price.

So the unwitting gold mining investor jumps on this yet-to-be-discovered-by-the-market gem and proceeds to agonize over the fact that years later the value has yet to be realized and the stock, which has likely been diluted by multiple share offerings at this points, is still languishing at or below its current price.

Such is the agony that most of us gold stock investors have gone through when we first began investing in the sector. Unfortunately, it seems that many continue this mistaken evaluation technique until they either give up or lose all their money. I myself got tired of losing money and instead decided to try to understand why some gold stocks go up and others seem to do nothing for years.

One of the main differences between the winners and the losers of gold mining are the capital expenditures that it takes to bring the mine into production. Mining is a process that takes place over many years, but the costs to build a mine are incurred mostly up front. In any discounted cash flow model, those costs loom particularly large in determining whether a project is economic.

The cheapest type of mine development (as a general rule), is a heap leach mine, particularly if the ore does not have to be crushed before being taken to the pad. All a heap leach mine requires are a bunch of yellow trucks and some cyanide solution to leach the gold out of the rock. Lydian’s Amsular project is an example of a heap leach development. Argonaut says that a typical heap leach project can usually be built for about $50/oz. That means a 2Moz deposit can be built for $100M. That’s about 1/4 of the costs it would take to build a mine of similar size that requires a mill and circuit.

During the Denver Gold Show presentation Argonaut put a lot of emphasis on the fairly minimal capital costs that it will take to bring on their two advanced stage projects. Argonaut can bring on a lot of production for what amounts to a relative pittance of capital expenditures. How can they do this? The company was smart in acquiring a couple advanced stage projects when they bought out Pediment Gold. The projects they bought were heap leach projects.

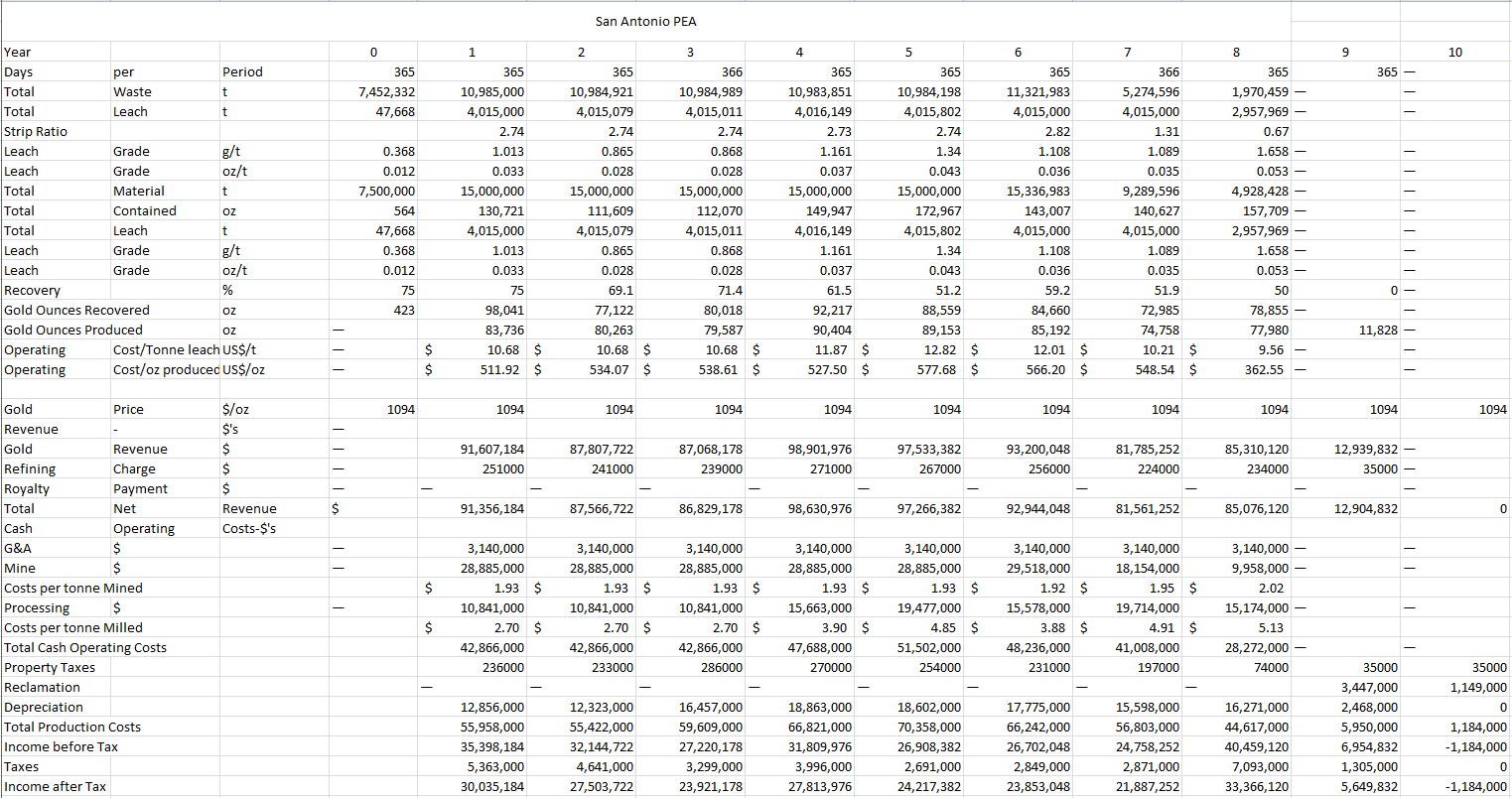

Management said during the presentation that an SRK estimate done by Pedimont (previous owners) suggested that La Colorada could be brought into production for around $25M. I took a look at the PEA released for the San Antonio project and the CAPEX for that project is estimated at $70M.

There are not many companies that can boast near term production potential with so little up front costs.

Both of these projects will have a material impact to Argonauts production profile, but the San Antonio is the bigger of the two. Once built, San Antonio has the potential to produce 80,000-90,000 oz of gold a year at $500/oz. The study (by AMEC) that developed that production profile was based on a resource of 1.2Moz. Recent drilling at San Antonio has discovered an additional new zone with potential and the resource has grown to 1.6Moz.

I wrote an article the other day where I quoted from a recent Rick Rule interview. One of the points he made was that pretty much all the PEA’s that are coming out these days are being done at $1100/oz gold. Impressively, many of them are showing good economics at this price, but they would show much better economics if something approaching the forward strip price was used. Most juniors are being evaluated and priced on this much lower gold price.

While Rule was referring to non-producing juniors, the same could be said for producing juniors with a pipeline of projects like Argonaut Gold. And San Antonio is a poster child for just that kind of valuation mismatch.

I spent a couple of hours working through the August 2010 PEA that Argonaut released on San Antonio. I looked at how the economics of the project would be affected by higher gold prices. Below are the NPV10 results that I determined (the full analysis is available here).

I think you could make the argument that right now, Argonaut is getting minimal or any value attributed to San Antonio. The stock is trading on par or at a discount to peers based on metrics of current production, when those peers have nowhere near the growth profile that Argonaut has.

This is particularly perplexing, I would say, given the relatively low capital cost associated with bringing the mine into production. Below is where Argonaut sits on an earnings and cash flow basis in the BMO universe.

And San Antonio is not the only growth opportunity that Argonaut has. La Colorada is smaller, and it seems like the company is still trying to get a firm understanding of the mineralization, but the project does boast over 600,000 oz of resource, and there was mention made that this probably exceeds 750,000 oz now with the recent drilling. As I mentioned already, a mine can be built at La Colorada for the paltry sum of $25M.

It looks like La Colorada has a bulk tonnage deposit at about 1g/t, but with a couple thin but very high grade veins fairly close to surface. There should be a new resource estimate on La Colorada coming out shortly. The advantage of La Colorada is that it is a past producing mine, so it is fully permitted and partially developed.

Together the two projects will cost about $90M to bring into production. Argonaut should be able to generate in the neighbourhood of $70M cash flow from El Castillo if gold prices stay around these levels. Thus, Argonaut should be able to substantially grow its production with little, if any, share dilution.

The key to this though will be El Castillo. El Castillo is an extremely low grade (0.33g/t) heach leap mine, also in Mexico. Argonaut has been very successful at producing fairly low cost ounces (~$550/oz) at El Castillo.

I have to admit that the low grade ore at Castillo scares me some. Such low grade leaves little margin for error.

The reason Argonaut can mine cost effectively with such low grades is because the deposit has a very low strip of less than 1. I grabbed the following screen capture from a presentation on El Castillo.

If you were to extend the graph into 2011, the strip would be even lower. In Q1 the strip was 0.88 and in Q2 it was down to 0.78.

During the Denver Gold Show presentation management went on to point out that the mine plan should allow them to lower the strip further in the coming yeasr. The strip ratio is expected to drop further as they progress deeper into the pit. The company has also recently built a processing facility on the east side of the mine. This should not only expand capacity, but it will help reduce costs. One of the biggest expenses in a low grade mine is the transportation costs. Having processing on either side of the pit should help reduce those costs.

When you put it all together you have a company with decent positive cash flow trading on reasonable metrics and with a tremendous growht profile that can be funded without dilution. It seems like a reasonable investment to make as long as the fundamentals remain in place for gold to stay at these levels.

{kind=link}