Week 21: Getting Worried Again

(current positions shown at end of post)

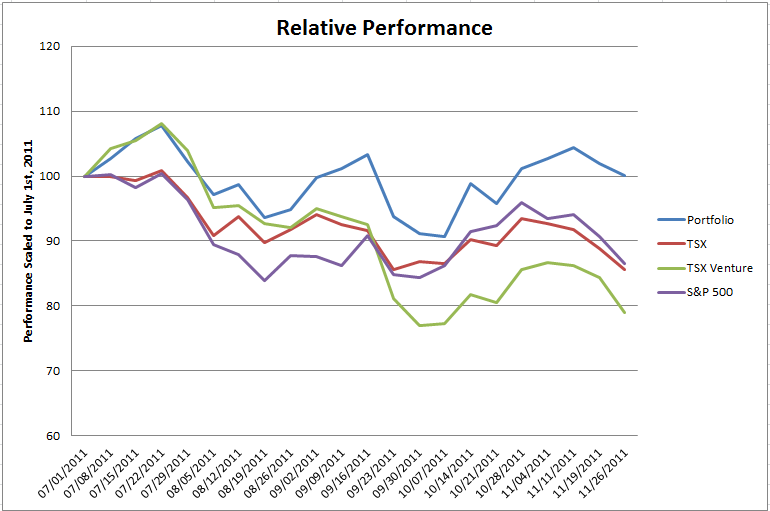

The benchmarks that I compare my portfolio performance to have begun to trend ominously down. I am a little concerned about what the market will do next week now that Thanksgiving is over and investors are looking more soberly at a pictrue of Europe that really should perhaps not be viewed without a good bottle of scotch. Of course the rumor making the rounds tonight is that the IMF is going to set up a massive bailout fund for Italy and that has the market soaring. Count me a skeptic here. Morgan Stanley put out the following note on the subject:

The Italian newspaper La Stampa reported over the weekend that the IMF is preparing a €400-600bn loan at a 4-5% interest rate for Italy. We would view this report skeptically, as even a credit line amounting to the lower end of the reported range would eat up the entirety of the IMF’s available $385bn (as of Sept ’11) forward commitment capacity. The only workaround would involve substantial IMF quota increases, a measure that would require the support of the US Congress.

The bottomline is that while stocks may be rising on the news, yields in Italy have hardly fallen this morning, an German yields are actually up. There simply is no easy Sunday night fix for this crisis.

Europe Still Dictates my Decisions

What worries me is that in the end it is the ECB that has to step up and fill the void and there is more than a little evidence out there that the ECB has no intention of coming to the rescue of profligate governments. There is a very good article in the NYT this weekend called As Crisis Mounts, Europe’s Central Bank Stands Back. The article explains the ECB position. Printing money to buy the bonds of countries facing funding problems does not solve the underlying issue. And the ECB is not necessarily going to step in. Witness the following:

“I think markets are going up a blind alley thinking there’s going to be a common euro bond or thinking that the E.C.B. is going to act as a lender of last resort,” Norman Lamont, the former British finance minister, told Bloomberg on Friday. “I think Germany would rather leave the euro than see the E.C.B.’s integrity affected.”

Instead, the E.C.B. insists, euro area governments must amend their errant ways. “Governments need to ensure, under any circumstances, the achievement of announced fiscal targets and deliver the envisaged institutional and structural reform programs,” Mr. González-Páramo said in London on Friday.

This is true. However what printing money does do is it avoids a full scale banking crisis and the commiserate deflationary recession brought on by the insolvency of Italy or Spain that results from the funding problems.

If the ECB chooses not to engage in significant bond buying, and to stand aside as Italian and Spanish yields march higher, markets will rightly conclude that a deflationary recession must be priced in. And this isn’t going to be goo for any asset, save perhaps US treasury bonds. It isn’t even going to be good for gold.

It is with that line of reasoning that I remain 50% cash, and while I am not allowed to short in my online portfolio, I am 50% hedged with shorts against my long positions. My long positions remain significantly skewed towards the gold stocks.

Portfolio Moves:

I didn’t buy or sell any stocks this last week in my online portfolio. This was not entirely the case however for my actual portfolio. In particular, I sold some Arcan early in the week this week. My overall exposure to Arcan in my online portfolio is about 5%. In my actual portfolio it is now only 2%. In addition to Arcan, I have a small position in Midway (about 1%) that is not represented here. Let’s talk for a second about the problem with these stocks.

Why you should be Wary the Oil Juniors:

Both Midway and Arcan are junior oil producers. Arcan has a large (96,000 acre) position in the heart of Swan Hills. I have written extensively on the company here. Midway has a fairly large (33,000 acre) position in the Garrington Cardium and a reasonably sized position (23,000 acres) on the fringes of Swan Hills.

Both Arcan and Midway show strong growth in production, as witnessed below:

Based on their growth both companies look like great investments. And they are… in the right environment. The problem comes with the particular environment we find ourselves in. We live in a credit constrained world. Based on events of the last few months, most notably of late the escalating problem that even the Germans are having trying to raise money, and one has to wonder how well companies that are not self-financing are going to do.

The downfall of Arcan and Midway is that they are anything but self-financing.

With European banks teetering on the brink it just doesn’t seem like a great time to be taking much of a chance on companies that need cash. I have reduced my exposure to Arcan and have decided to leave my exposure to Midway at its current level unless we see some sort of resolution across the ocean (as if). I likely will wish that I had done the same steps here online. Unfortunately Arcan fell rather substantially last week and I am reluctant to reduce the position now at below $5/share.

New Short Position in Deutsche Bank:

The other move that I made that is not expressed in the online portfolio is that I add a short position to Deutsche Bank. I have been trying to add a short position in this stock for months. Its hard to get the shares to short with. I finally had some luck and shorted it at $34. I have been reading about the company regularly in FT. This is one leveraged bank. The tangible assets to equity ratio is 60:1. To compare, when researching the regionals, I wouldn’t look twice at a regional bank that had a ratio above 10:1, and many of the one’s I found most attractive (Home Federal Bank of Louisiana for one) had ratios of less than 5:1. This makes DB the most underfunded bank in the EU.

Secondly, DB relies on wholesale funding for short-term liquidity to a greater degree than most. Below is how Deutsche Bank stands in comparison to other EU banks with regard to the Net Stable Funding Ratio (NSFR), which is often used as a proxy for determining a banks reliance on wholesale funding.

It seems to me that the combination of high leverage and reliance on less than stable sources of funding are a recipe for a liquidity squeeze for DB as Europe continues to get worse.

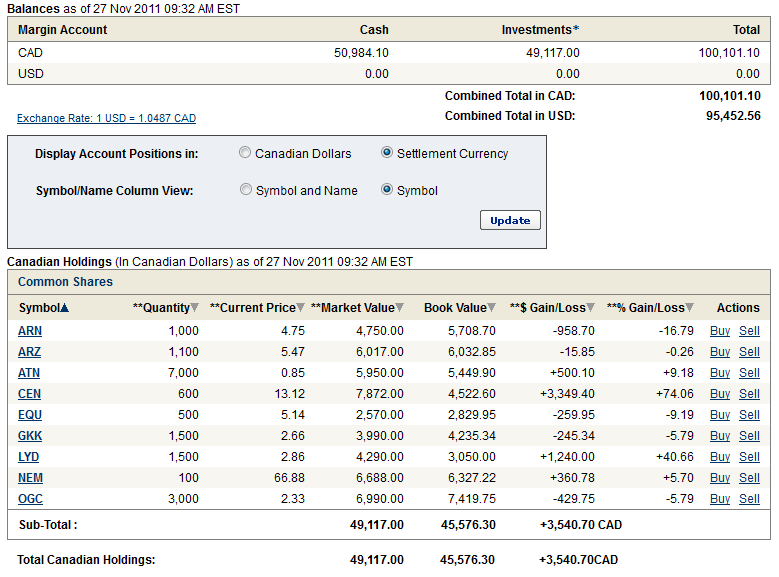

Current Portfolio: