Week 29: Conviction and Humility, Investigating PHH, Don’t forget about Atna, Buying Midway

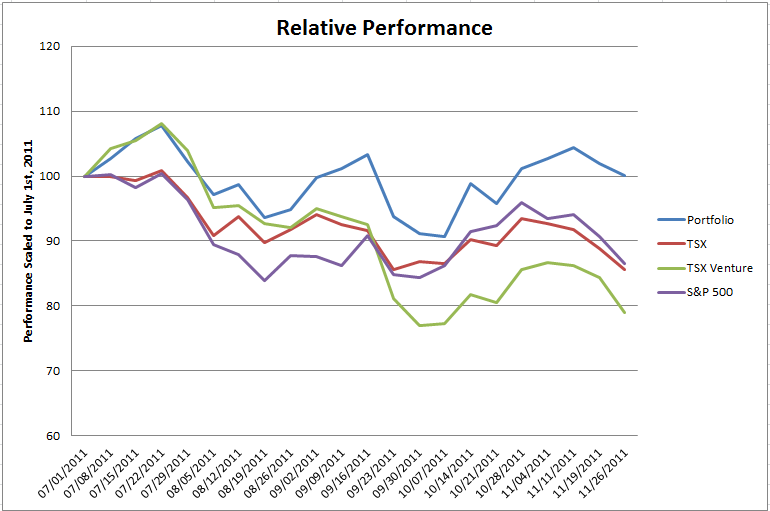

Portfolio Performance

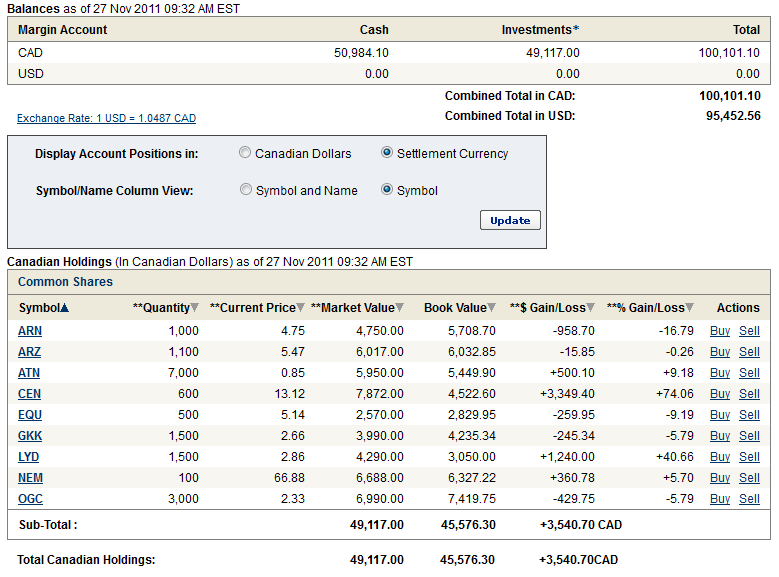

Portfolio Composition:

Portfolio Composition:

On Conviction and Humility

I find that investing in stocks is a constant antithesis/synthesis (to use a couple of terms from philosphy) between conviction and humility. Never is this more evident than when things aren’t going your way.

While the market has been up the last couple of weeks, and my portfolio has been up somewhat as well, it is not doing as well as I would like, not as good as the market even, and that makes me want to reevaluate.

Part of me wants to just get out and start all over again. Right now there are things of which I am wrong. Wrong about some of the gold stocks I own (while Atna continues to do well, Aurizon is not doing well, Lydian is not doing well, and a couple of my more recent purchases, Esperenza and Canaco, have stalled out). Wrong about some of the oils I own (I probably should have sold out of Reliable Energy at 30 cents) that aren’t doing much of anything. Certainly wrong about my big bad bailout bank short bet, which went quite far south last week.

The other part of me, pushing just as strongly, wants to stay the course and, more exactly, to ignore what the market might be telling me because the market is wrong and I am right and in time I will be vindicated.

It goes without saying that this last attraction is a dangerous one. Surely we all have listened to the expert that held his conviction against all evidence to the point where his credibility was lost forever.

The truth between these two extremes lies, of course, somewhere in the middle. The difficulty is figuring out exactly where that is.

The basic long term investment theses on which I am currently holding stocks (and shorts) are as follows:

- Europe is on an inevitable course to dissolution, with a collapse in Japan not far behind

- Gold is the only asset that is no one’s liability and it will gain respect as a store of value as these events unfold

- The US, while troubled, is muddling through, and the US housing market has likely had, as Kyle Bass has put it, the pig go through the python

- Oil is harder to find and harder to get out of the ground then most people appreciate, and its price will prove sticky to the upside

- The hz-multifrac is a revolutionary technology and so you want to own oil companies that can take advantage of that technology

I think its helpful to review these basic points on occasion, particularly when things are not going my way. If I can still stand by these tenants then the rest is just a matter of evaluating if the individual stocks themselves are decent businesses (or perhaps more importantly good stories) in their own right.

And, having thought about it over the weeked, I wouldn’t stand away from any of the above.

Two weeks of a market moving up with many of my stocks doing nothing can seem like an eternity. Sitting with as much cash as I currently have (though I have reduced that cash level somewhat, mostly in response to specific opportunities and a recogntion that the deterioration of Europe no longer seems imminent) while the market rises, can be tough to bare. But I can’t just abandon what makes sense because of a few tough weeks. If the facts change, certainly I have to change with them. No doubt about that. But when the main fact that has changed is that the market is not going down any more, I think it is wise to respect that fact (no sense doubling down and some sense in lightening up with what doesn’t work) but not so wise to change course entirely. Better to move as a big ship might, slowly inching it way towards a new course, ever on the lookout for signs on the horizon that might make the destination more clear.

Wading into the Mortgage Market

On Tuesday this week a 13-G was issued that Hayman Investments (the hedge fund run by Kyle Bass) had purchased over 7% (4,448,751 shares) of PHH Corp. I got a google alert on the news almost immediately. It still wasn’t soon enough. The stock was up 10% within minutes and closed up 12% on the day.

I sat down on Tuesday night with the intent of understanding what Bass what was up to.

I don’t think this is just Bass buying a cheap company (which they are) and hoping for the best. I think there is more to this story, as I will explain below. But first, lets talk a bit about where I think we are in the housing cycle.

First of all, I am no blind optimist here. I don’t think for a second that housing is about to make a robust 180 with rising prices and robust new builds. That’s not happening for a long time yet.

But that does not mean that all housing company’s should be left in the trash bin. No I think that those that rely more on volume then price may find themselves doing better this year, and may be ripe for a move.

Why? Because I think prices have fallen enough in many markets. Most of the damage in terms of declines appears to have been done. There was a great graph provided by Core Logic a couple weeks ago that showed prices both including and excluding foreclosures.

Illuminating! If you ignore foreclosures, prices nationwide are on the verge of going positive. If you look at the regional data, prices are actually up in many locales. And while some areas are still bogged down in foreclosures, many have worked through the worst of it. Those are going to be the areas where we start to see a turn.

So it makes sense to look for companies that stand to gain from these first signs of stabilization.

And with that, onto PHH…

PHH is in the business of mortgage origination. They are in the business of mortgage servicing rights. Tthey are also in the business of commercial vehicle fleet management but I don’t think that’s the story here so I’m not going to dwell on that. Lets talk for a minute about the two former businesses.

Mortgage Origination

Mortgage origination basically consists of finding a person that needs a loan to buy a home, showing that person a list of mortgage options of how they could finance that loan, qualifying the borrower for loan guarantees such as those from the GSE’s, and then processing the loan through (doing all the paperwork) and passing it through to the eventual lender institution (usually to Fannie, Freddie or a bank that will either keep it on their books or sell it to another investor). PHH takes a cut in the process, or an origination fee, that is typically between 1/2% and 1%. In the third quarter the company said that their “pricing margin also expanded by more than 47 basis points as compared to the second quarter.”

Mortgage Servicing

Mortgage servicing happens after the loan is made. The servicer is responsible for calculating how much the borrower owes and collecting that amount. If a loan is not being paid then the servicer takes on additional responsibilities such negotiating a workout upon default, looking after the foreclosed property and such.

PHH refers to these businesses as a natural hedge of each other. Why? Because they are inversely correlated with respect to interest rates.

Let’s say interest rates fall. What happens? People with mortgages at higher rates refinance those mortgages. That’s great for the origination business. They are writing up refi’s and taking in the fees.

Not so great for the servicing business. Those refi’s mean that the mortgages that PHH has the rights to service no longer exist. Now ideally PHH originates the refi and thus takes on the servicing rights for that refi so the old mortgage servicing right (MSR) is replaced with a new one. But there’s no guarantee of that.

Rates go up and the opposite situation occurs. Origination suffers, no one is refinancing at the higher rates, but that also means the MSR’s are not being lost either.

As it is, PHH has proven to be pretty good at holding on to more MSR’s then it loses. Forthe 9 months ending in the 3rd quarter the company had a replenishment rate on MSR’s of 167%.

Ok, back to Bass. There are a number of things happening in the mortgage business right now from which PHH stands to benefit. Let’s go through them one by one starting with Harp II.

HARP II

Harp stands for the Home Affordability Refinance Program. Harp II is the name that has been coined for the new version of HARP. It supersedes the original Harp. Harp I was a total failure.

The HARP program has helped far fewer borrowers than its proponents estimated — roughly 894,000 borrowers since Aug. 31, 2011. — and many less than the estimated 11 million U.S. homeowners who owe more than their homes are worth.

Why was it a total failure? A few reasons:

1. Put back risk: Basically when a bank participated in the original program they were worried that they would get stuck with the original mortgage. I think what happens here is that to rewrite the original loan to new terms, the loan is going to be scrutinized. The banks and other underwriters know that the quality of many of those original documents are sketchy at best and they would rather not have to pull out the skeletons.

2. LTV Limits: This is probablythe biggest problem. The original HARP program dealt with current loans with LTV’s of 80-105. That was expanded to 125 in 2009, but that still wasn’t enough. I was surprised by that until I read this:

This should have a big impact in certain parts of Nevada, Arizona, and Florida where many borrowers owe more than 125% of the value of their homes. In Nevada, for example, two thirds of all loans backed by Fannie Mae are underwater, and half of all loans are above the 125% loan-to-value cut-off.

3. Appraisal costs: the borrower had to have an appraisal done to qualify for the original program. That appraisal could cost $400. Borrowers were reluctant to take this cost on when there was no guarantee they would be accepted by the program

HARP II aims to correct these mistakes. The LTV limit is gone. Appraisals are no longer required. And banks are protected against the put backs.Says Brian Ye, analyst at J.P Morgan Chase & Co:

“We are of the opinion that there are enough changes to the program that bank servicers could really change their behavior, and this could be one of the first times that the administration has under-promised and over-delivered,”

The two tiers of HARP II

There is one particular element of the new program that helps out PHH is that servicers get a head start over third party originators. I confess I don’t know just what of impact this is going to have, but it is interesting and potentially significant, so I think its worth mentioning. Servicers like PHH have been writing borrowers up for the program since the beginning of the year. A third party originator cannot submit any documents to Fannie or Freddie until March. This was done to entice the banks into the program, but the corrollary is that a company like PHH can capture business up front without the competition.

There is more interesting information on the new HARP program here.

What’s it going to mean?

This is, of course, the big question. The program is aimed to attract two million borrowers by the end of 2013. This would be a little more than twice what the original program attracted.

However if the program works, and if JP Morgan turns out to be right and the administration “under-promised”, there is certainly a lot of room for upside. According to CoreLogic:

10.9 million, or 22.5 percent, of all residential properties with a mortgage were in negative equity at the end of the second quarter of 2011. Eight million borrowers with negative equity, or nearly 75 percent of all underwater borrowers, have above market rates. The disparity is even greater for those with severe negative equity. More than 40 percent of borrowers with 125 percent or higher loan-to-value (LTV) ratios have mortgages with rates at 6 percent or above, compared to only 17 percent for borrowers with positive equity.

Apart from the obvious fact that these numbers show just how staggeringly bad housing has become, if you prefer to see the glass half full those numbers also suggest that there are a lot of borrowers out that could benefit from a program like this.

I was listening to this week’s Lykken on Lending and they were talking about Harp II. Lykken said that listeners (brokers and third party originators) needed to gear up for the “mother of all refinancing booms”. In another segment a couple of weeks earlier Lykken and his guests spoke quite excitedly about the impact of no LTV limits. The one guest talked about how common it is to have to turn away borrowers because they are too far under on their home. HARP II should help with that.

BOA and correspondent lending – another tailwind

So first of all, what is a correspondent lender?

Consider a broker who develops significant business volume, has earned the confidence of wholesale lenders who will authorize him to approve their loans, and has accumulated some capital. He can now obtain a credit line from a bank that can be drawn against to fund loans, repaying the loans when they are sold to wholesale lenders. Under the law, the broker has morphed into a “lender” – the type called a “correspondent lender”.

This has been a business the big banks have taken a large piece of. Until now. In August BoA reported that they were exiting correspondent lending.

This isn’t small potatoes. It accounted for”47 percent of Bank of America’s mortgage originations, or $27.4 billion, in the first quarter of 2011, the Wall Street Journal said citing Inside Mortgage Finance.”

There are rumors others are leaving the business. Its a low margin, highly competitive business but it could become less so with some of the big players moving on.

In comparison, for PHH total mortgage closing volumes for 2011 so far were $36.3 billion of which approximately 70% were retail and 30% were wholesale/correspondent. Here is what management said on the Q3 conference call:

Yes I’m going let – yes the answer to the question is yes, we think there are better opportunities but once again we’re really pretty opportunistic in that channel. So we pay close attention to margins in that channel. As you know it’s probably the most cost competitive channel, it is the most cost competitive channel that we operate in and we’ve seen some really strange behavior in that market in terms of where margins are being priced. Some of our competitors are in the market, when they are in the market they’re very aggressive in terms of their pricing and then they back off and they’re out of market and that’s why we stay really opportunistic in that market. Luke, do you want to add anything?

The company made a total of $95M off of mortgage production, meaning off of fees for new originations of that $36.3B of loans they processed. The company doesn’t break down the margins between the retail and the wholesale/correspondent. Total revenue from the segment was $264M, which suggests that the fees on average are around 0.7% of total loan value.

Tailwind 3: Signing up new partners

The last tailwind for PHH is that they are having success signing up some big partners for their origination business. From the Q3 CC:

We also made significant progress in growing our nationwide sourcing footprint over the past two quarters signing five new private label accounts. The new relationships include Barclays which we mentioned on last quarter’s call and today we’re pleased to announce that we’ve added Ameriprise and Morgan Stanley Private Bank along with two other financial institutions all as new PLS partners.

They also lost one significant client in Charles Schwab but over all the company expects to gain significant production:

We expect the five new PLS accounts in the aggregate based on their 2011 production and taking into account ramp up time and anticipated launch schedules to produce about 7 billion in closing volume in 2012, about double what we predicted for Schwab.

Twisting in the (tail)Wind

The Donald Coxe conference call this week was very good, and it produced one particularly enlightening graph.

Long term rates, both treasury and mortgage, are at all time lows. When the Fed embarked on operation twist, it was with the intent of bringing down the long end of the curve, and by doing so, propping up and ideally pushing ahead, the housing market.

I would say this was a success.

When you add to the fact of HARP II that interest rates are at all time lows and really, given the decline in house prices in many markets, are basically creating the conditions where you would be crazy not to buy a house, you just have to think that this is going to help origination activity in 2012. I think the point that is sometimes forgotten is that the downard spiral of housing is really caused by the foreclosure mess. Its the lynchpin. If you could create the conditions to stem that flow, I think the situation would right itself a lot faster than is appreciated.

When core earnings matter

A lot of the time when a company is reporting some sort of non-GAAP earnings, its in order to hide something. A good example of this is Salesforce.com. They report non-GAAP earnings that exclude certain costs (particularly stock options) that they would rather ignore.

PHH reports a core earnings number every quarter but for a very good reason. Core earnings is a far better representation of the company’s profitability than is the GAAP number.

The problem with the GAAP number is that it is obscured by changes in the mark to market value of the MSR portfolio. PHH has to write up and down their mortgage servicing rights with changes in interest rates and to a lessor degree credit quality. When rates go down they have to write down the value of the rights and when rates go up they have to write up the rights.

The fluctuations on the income statement caused by these mark to market moves are huge. Up to $400M in some quarters. If you look at quarterly GAAP earnings over the past couple years they look like a scatter chart.

The reality of the MSR’s is that as long as the company is replenishing the existing pool with more rights from new originations then its losing to payoffs of its existing pool, its all good. As I already noted, PHH is doing that.

The core earnings number takes out that effect. And if you look at that core earnings number you see a pretty cheap looking company.

All that, and discount to book…

The last point I would like to make about PHH is the discount relative to book value. You can get the shares at a pretty substantial discount, even after the post-Bass run up:

What’s even more interesting is that this discount exists even after the valuation of the MSR portfolio has been clobbered by falling interest rates. It is not impossible to imagine a scenario where the MSR’s add book worth $500M plus, or another $10 per share.

What’s even more interesting is that this discount exists even after the valuation of the MSR portfolio has been clobbered by falling interest rates. It is not impossible to imagine a scenario where the MSR’s add book worth $500M plus, or another $10 per share.

So what does Bass see?

To sum it up, with PHH you are getting a cheap company that has earned decent money of late and that should benefit from the tailwinds of HARP II, weary competitors and a rebounding housing market.

The negative with PHH is the debt they have coming due, and whether they will have the cash to pay it off. That debt is an issue I believe is worthy of a post in itself, and I will try to get around to that next week.

Europe is still a problem

…it just doesn’t seem like it right now.

I have a few other things I was hoping to talk about this week but I’m running out of time and this letter is getting quite long already. But I do want to talk a bit about some of the reading I have done on Europe the past week.

It seems what with the stock market rising every day that Europe is old news now. Yet I think that to ignore the risk of Europe right now, to go all in, is still at best a gamble. It may turn out, you could do it and cash out big in 6 months. But to say you knew it would turn out that way would be kidding yourself. We could just as easily wake up tomorrow in crisis mode again as in the happy-happy-risk mode that we’ve been in the last couple weeks.

Europe hasn’t gone away.

The S&P downgrade of a number of European countries been widely reported already so I’m not going to dwell on it, but I do want to point out that the language used. In particular:

We also believe that the agreement is predicated on only a partial recognition of the source of the crisis: that the current financial turmoil stems primarily from fiscal profligacy at the periphery of the eurozone. In our view, however, the financial problems facing the eurozone are as much a consequence of rising external imbalances and divergences in competitiveness between the EMU’s core and the so-called “periphery”.

This strikes at the basic point that I have made in past posts. Austerity measures are not going to fix the problem with Europe because the problem is not a one time spending binge that just has to be paid off. The problem is much deeper, relates to inherent inequities in the productive abilities of the economies, and is quite possibly not solvable without a break up.

As John Maudlin said in his piece “End of Europe”:

For most of the past two years, European leaders have tried to deal with the problems as though they were short-term liquidity problems: “If we just find the money to buy some more Greek bonds, then Greece can figure out how to solve its problems and then pay us back. Given enough time, the problem can get solved.”

They have now arrived at the understanding that it this not a short-term problem. Rather, it’s a solvency problem of the various governments, which of course creates a solvency problem for their banks. They are now addressing the problem of solvency and providing capital until such time as certain countries can get their budgets under control and the bond market sees fit to provide the capital they need.

But they are completely ignoring the third and largest problem, and that is massive trade imbalances. Germany exports products to the peripheral European countries, which run trade deficits. As I have shown in several letters, a country cannot reduce private-sector leverage, reduce public-sector leverage and deficits (balance its budget), and run a trade deficit all at the same time. That is simple, unavoidable math, based on 400 years of accounting understanding. Ultimately, there must be a trade surplus if leverage and debt are to be reduced.

There is a great model that Maudlin creates in the post that summarizes the situation of Greece, Portugal et al to a tee. I would recommend reading the piece in its entirety. One last point from the piece:

Prior to the euro, the imbalances would be handled by currency exchange rates. The value of the drachma would go down relative to the value of the deutschmark. Things would balance over time. Now, all of the eurozone countries are effectively on a gold standard, with the euro standing in for gold this time. Britain, the US, and Japan print their own currencies. Their currencies can rise or fall over long periods of time, based on national accounts and the desires of foreigners to buy goods or invest in their countries.

He is retreading the old Jane Jacobs idea that I brought up a couple weeks ago:

What Europe has embarked on with the Euro is the exact opposite of what is needed. Currency regimes need to evolve to produce better feedback, not worse. The Euro currency feedback mechanism is skewed by the strength of the German economy (actually more exactly the economy of its one or two prime export replacing cities, Berlin and Frankfurt). Peripheral countries like Italy, Greece, Spain and Portugal are doomed to receive faulty feedback rather than the natural “export subsidy” that would occur if those countries had (lower value) currencies of their own.

To think that all is well is to mistake the calm eye of the storm for the end of it.

Meanwhile, I’ll end my Europe talk with this: There seems to be a growing recognition that Greece needs to exit the Euro. The chief executive of Germany’s natural gas firm Linde’s chief executive Wolfgang Reitzle was quoted as saying the following in Reuters:

“In the medium term Greece needs to exit. And the writedowns on Greek debt will not be between 50 to 70 percent, but in the end will be written down by 100 percent,” Reitzle said.

Asking Germans to pay more than 50 percent taxes to help fund other euro zone countries will erode the will of the German electorate to support rescue measures, Reitzle said.

Although this scenario is not desirable, he felt that German industry would survive working in a new currency.

Atna’s jump in reserves (and share price)

I haven’t spent as much time as I should writing about Atna. I tend to ignore the stocks that I am right about. This is perhaps not the best way to self-promote, but since I’m not really in that ballgame anyways, who cares. I learn more from my mistakes.

But don’t take that for disinterest. I watch Atna like a hawk every day. As I pointed out a month ago, I think that if Pinson works out the stock is worth somewhere between $3 and $6. I know that there is some skepticism around Pinson, that there may be rock stability issues, but I’m of the mind that the current stock price is more than pricing in that risk.

It feels to me like a stock being accumulated before a break-out. Perhaps we got a taste of things to come this week when the stock popped over $1 and up to as high as $1.05.

On the news front, Atna released an updated resource at Briggs on Thursday.

There is not too much to get too excited about, though it is nice to see that they managed to move about 50,000oz to measured and indicated, basically replacing production. Overall they showed a slight increase of about 14,000 oz all in. At the current production rate (45,000 oz), Briggs is good for another 10 years. That alone is probably good for the current share price.

Buying Midway Energy (Again)

The other move I made this week was to reinitiate a position in Midway Energy. I decided to pull the trigger here because the other Swan Hill players showed signs of moving up towards the end of the week.

I already own positions in Second Wave and Arcan (though the Second Wave position didn’t get taken in the practice account due to an unfortunate glitch in the order fill). I did not own Midway and it had not moved higher and it seems a reasonable presumption that it will follow suit eventually.