Community Bankers Trust: As good as it gets?

Ever since Community Bankers Trust (BTC) announced that they were repaying the dividend on their TARP preferred , the stock has gone into the stratosphere. Its now become a double since my initial purchase.

What I want to do in this post is look at whether this move to the upside is all I should really expect, or whether this is the beginning of a larger, longer term move. The question is: Do I have a two-bagger here, or a potential five bagger.

A little history on the company

I bought Community Bankers Trust (BTC) as a turnaround story. They are a bank that has been trying to reincarnate itself after the first incarnation came close to an early death. My observation is that they have been successfully navigating this resurrection, and with the recent turn in profitability (and a helpful turn in the economy) the bank is on its way to realizing its earnings potential.

How did they get to here?

The original growth strategy was, as far as I can tell, to buy other banks and get bigger. Witness, the name of the original company was called Community Bankers Acquisition Corporation (CBAC). They weren’t exactly being subtle. Along with the acquisition strategy, the bank seemed to have a “worry about the profitability later” strategy. This may have worked ok if the economy continued to grow as it had in the early part of the decade but it fell flat along with the economy in 2008.

As best as I can discern the acquisition effort was spearheaded by Gary Simanson. He headed up the original company CBAC, and then moved into a position of Strategic Vice President, a position I don’t think I’ve ever heard of with any other company. According to this article, Simanson was responsible for subsequent acquisitions.

In truth, the timing was what killed the acquisition strategy. To quickly step through the timeline, in May 2008 the company began its journey by acquiring two local Virginia banks, TransCommunity Financial Corporation, , and BOE Financial Services of Virginia, Inc. In November the bank moved ahead and acquired The Community Bank, which was a little bank in Georgia. Finally in January 2009 they acquired Suburban Federal Savings Bank, Crofton, Maryland.

So you had 4 bank acquisitions in less than a year happening at the time of a 100 year financial tsunami. How do you think things turned out?

Change in Direction

By 2010 Simanson had left the company and the direction of the company was changed to the more pragmatic “we need to get profitable before we go belly up” strategy.

This was described pretty bluntly in the 2010 second quarter report. CEO Gary Longest said at the time:

Our strategy has shifted from that of an aggressive acquisition platform, to one that meets the banking needs of the communities we serve, while providing sustainable returns to our stockholders. To this end, we are taking the necessary steps to return immediately to profitability. We are actively analyzing our market base to assess the contributions of all branches to our franchise value and will take the appropriate actions in the third quarter of this year. Additionally, we will make aggressive expense reductions, and will look to restructure and strengthen the balance sheet. We are confident that the analysis of these potential critical paths and the resulting execution of these initiatives will lead us back to profitability quickly.” “Our goal is an immediate return to consistent quarterly profits. To accomplish this, we have no alternative as a Company but to make clear and intelligent decisions in the next 60 days, no matter how difficult, to accomplish that goal as soon as possible. That is our full focus.”

In a somewhat odd twist to which I’m sure there is a good story, Longest himself was gone only a couple months later. Nevertheless the interim CEO and soon to be permanent CEO Rex L. Smith took up the reins and has carried out the strategy quite well given the circumstances.

Why the TARP payment matters?

As the chart I posted at the start showed, the stock had been trending up for a couple of months but it was really the news of the TARP payment that has sent the shares to another level.

The amounts involved in the TARP dividend are fairly inconsequential. The accumulated payment is around $1.5 million. The deferred payments on the trust preferred capital notes looks to be significantly less.

What is consequential is that the regulators are putting their stamp of approval on the bank and giving it a clean bill of health. What is also consequential is that with the TARP funds being paid the company is setting itself back up towards the eventual issuance of a common dividend.

Where are they now?

Community Bankers Trust has done a lot to lower costs since the clean-up in Q2 2010. First, they have brought down the interest costs of their deposit base. Time deposits, which are expensive high interest bearing deposits, have decreased from 73% to 67% of total deposits since the end of 2009. As well, the cost of the time deposits has come down from 2.9% in 2009 to 1.6% in the third quarter.

The effect has been a step change in net interest margin (NIM) since the strategic direction change in 2010 (note that this graph is a simplified version of NIM calculated as a percentage of all assets rather than the more common formulation of interest bearing assets).

The company also undertook efforts to reduce operating expenses. The Effiency ratio, which is simply the ratio of the total non-interest expenses at the bank (so the salaries, building costs, lawyer fees, pretty much everything except the actual cost of borrowing money) to the net interest margin (so the amount of interest made minus the amount of interest paid), has fallen to a low level.

Two ways of valuing the company

First lets look at earnings. The chart below shows proforma quarterly earnings for the last couple of years. The proforma number strips out the provision for loan losses, the FDIC intangibles, losses on real estate and gains of the sale of securities. So basically I looked at the banking skeleton that is BTC.

The bank has consistently been pulling in more than 10 cents per share for the last 3 quarters. While the numbers ignore the rather large loan losses that the company has had to take, they make the point that once the bad loan book is worked through, the bank has significant potential for earnings.

Now lets look at book value. I’m going to take this straight from the company’s fourth quarter report. The bank sports a tangible book value that is much greater than the current share price even after it has double from $1 to $2:

How about the legacy loans?

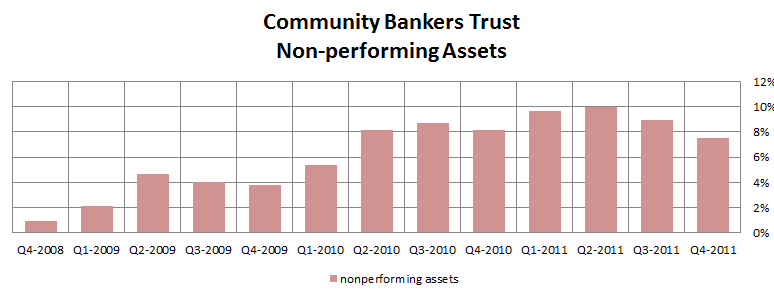

The remaining negative for the bank is that it still has an extremely elevated portfolio of non-performing loans. However there are signs that this is abating; the fourth quarter showed more progress in bringing down nonperforming assets. The bet with Community Bankers Trust remains what it was: the US economy is turning the corner, the Fed is not going to allow it to fall into another recession, and so the worst of the loan defaults are behind us.

To put these numbers in perspective, typically you wouldn’t want a bank to have non-performing loans in excess of a couple of percent. Many of the best banks I’ve looked at have nonperforming loans of well less than 1%. BTC, onthe other hand…

So can it go higher?

The question I set out to answer is whether I think the bank can continue to move higher. A double is great, especially when it happens this quickly, but keep in mind before the summer of 2008 this used to be a $7 stock. Based on what I have laid out above, I think you can make a strong case that it could go higher. Things have to go right to be sure, but if they do the earnings and the assets are there.

Bottom line: I’m not selling.