Over the course of last week four of the five regional banks in my portfolio reported first quarter earnings. Since that time I have been busy reviewing those earnings and drawing conclusions on whether the stocks should remain owned, or be punted out for other opportunities. Below I will go through my analysis and thoughts on each of these banks.

Rurban Financial (Ticker: RBNF)

Rurban Financial reported earnings last Tuesday. Rurban does not have a particularly troubling loan book, and while they do have some non-banking related problems (such a legacy data processing business that does not appear to be doing very well) they are mostly set to generate strong earnings going forward. So when I look at Rurban’s results, I focus on what they were able to earn.

Earnings per share came in at 20 cents. Because Rurban has a large mortgage servicing portfolio they are subject to big swings in earnings due to the GAAP valuation adjustments that they have to take on their portfolio of mortgage servicing rights. While these adjustments are GAAP requirements, they tell us nothing about the business and tend to obscure the true earnings of the business. Thus, I like to look at a “core” earnings number that eliminates the valuation adjustments as well as any other one time charges and the loan loss provisions. Core earnings came in at 19 cents. Core earnings for the past 5 quarters are shown below:

I’m not too worried about the decline in earnings quarter over quarter because a lot of it is seasonal. Rurban sold a lot less mortgages in Q1 2012 than it did in Q4 2011 and that is just the seasonal nature of that business. For some reason a lot of markets in the US experience high mortgage demand in Q4, and low demand in Q1. In most Canadian markets it is the opposite of that, with Q4 being the slowest of the four quarters.

I’m not too worried about the decline in earnings quarter over quarter because a lot of it is seasonal. Rurban sold a lot less mortgages in Q1 2012 than it did in Q4 2011 and that is just the seasonal nature of that business. For some reason a lot of markets in the US experience high mortgage demand in Q4, and low demand in Q1. In most Canadian markets it is the opposite of that, with Q4 being the slowest of the four quarters.

Another contributor to lower earnings was reduced revenues from the RDSI data processing subsidiary. RDSI provides data processing services for banks across the Midwest. RDSI lost $1.4M in 2011 and doesn’t appear to be doing any better in 2012. Its a strange situation because the big cause of the loss in Q1 were writedowns related to Rurban’s own bank deciding not to use RDSI for their banking related data processing needs. Clearly they are cutting ties (winding down?) and maybe that will be for the best in the long run. Below are revenues from RDSI less intercompany over the last 5 quarters. Its become small enough that going forward it should cease to be the drag on earnings that it has been. And that’s a good thing.

Mortgage revenue at Rurban continued to be strong; Rurban generated $1.2M in origination volumes in Q1 versus $420K in the same quarter last year. As I already mentioned originations are always down in Q1 versus Q4, so that number was a decline from $1.5M in the previous quarter. The year over year growth in origination led to further growth in their servicing business, which was up by another $20MM in terms of unpaid balance sequentially. Nonaccrual assets continue to fall, down to $6.5M from $8M in the fourth quarter of last year. And the company continues to rein in cost, witness by another drop in non-interest expense. Negatives for the quarter were pretty much the same as those I saw elsewhere in the banking sector. They are getting squeezed on interest margins (down from 4.07% to 3.64%), and loan growth was pretty flat quarter on quarter.

Overall Rurban announced pretty solid results and they are continuing to move towards their potential $1 per share of earnings. There is still work to be been, ROA remained poor at 0.60%, but that is why the stock trades at only 2/3 of book value, and why the opportunity for further price appreciation remains. I have been very happy to see the shares move up as they have over the last week.

Shore Bancshares (Ticker: SHBI)

Shore had a tough quarter. While I had been hoping that the company’s loan book was on the mend, the first quarter results showed that there is still some work to be done.

The loan book deteriorated over the quarter. The company had to put aside provisions for credit losses of $8.4M, which was way up from $4M in Q4 and $6.4M in Q1 2011. Nonperforming assets rose to 8.1%. I had been hoping that nonperforming assets had peaked in Q3 and would continue to roll over in Q1. Unfortunately not.

The company said that the rise in nonperforming loans resulted mainly from one relationship. 50% of the $9.1M in charge-offs were related to a single large real estate borrower.

If you can get past the loan book (and I wish they could get past their loan book), there were some positives for the quarter. While deposits increased 4.2% on a year-over-year basis and, notably, core noninterest-bearing deposits were up 17.4% year-over-year, so the company’s borrowing base continues to move towards lower cost loans.

If you look at Shore’s eventual earnings poential, if they could stop taking massive writedowns every quarter, it remains strong. Earnings ignoring the provisions were $0.39 per share. Over the previous twleve months Shore has put together earnings of $1.50 per share if you ex out the loan losses. So the potential is certainly there. Unfortunately loan book stabilization appears to be a bit further off then I had anticipated.

I’m not sure what to do with Shore. I am tempted to cut it and run. I originally got the idea from Tim Melvin of Real Money. He described the investment as a 5 year hold and a 3 to 5 bagger. Given that the bank trades at about 1/2 of tangible book value and that it used to be a $25 stock before the collapse of 2008, and you can see where he is coming from. However I am not quite as patient as Mr Melvin. I like stories that are in the process of turning it around, not just with the potential to turn things around at some point. I haven’t sold out of the stock yet, but I have an itchy trigger finger.

Community Bankers Trust (Ticker: BTC)

BTC’s earnings are always obscured by the effect of the indemnification asset that the company carries as a result of an agreement to take over a failing bank, SFSB, back in 2009. The indemnification asset is an accounting tool that accounts for the FDIC guarantee that BTC received when they took over the SFSB loan portfolio. Unfortunately, the accounting of the asset it such that when there is better than expected performance in the SFSB portfolio, the company has to amortize the indemnification asset on their income statement. The size of these amortizations is extremely large relative to earnings. In Q1 the amortization was $1.9M versus net income of $0.9M.

I always ex-out the effect of the indemnification asset when I look at BTC’s earnings. The asset says nothing about their cash generation and earnings ability. In fact it actually works in reverse to that underlying ability.

Ignoring the indemnification asset and a few other small one time gains and losses, BTC earned 13 cents in the quarter. On this core earnings metric BTC has earned 52 cents over the prior twleve month, which means it remains an incredibly cheap stock trading at a little over 4x earnings. Looking at the same sort of “core” earnings number that I did for Rurban, you can see that the bank is consistently been pulling in 10-15 cents of earnings a quarter for the last 4 quarters.

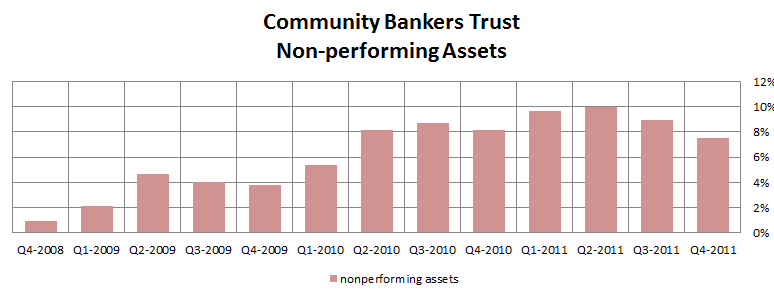

BTC has done an excellent job of pulling itself back from the brink of bad loan losses, and this continued in Q1. Nonperforming loans on its non-covered portfolio (non-covered refers to loans not covered by the FDIC loss sharing agreement) decreased 13% or $4M quarter over quarter. Nonperforming assets have fallen from a high of 9.7% of total assets in the second quarter of last year to 6.9% of assets in the most recent quarter.

Meanwhile the company grew its loan book marginally in Q1, which is traditionally a slow time of the year for loan growth for the company and a quarter where their loan book shrank last year. It is also interesting to note that unlike most of their competitors, BTC managed to maintain a flat net interest margin in the quarter, at 4%.

I really like the turnaround that is taking place at BTC. Having bought the stock at a little over a $1, I am sitting on a double already. Yet I have no plans to sell. BTC was a $3.50 stock as recently as the beginning of 2010 and was a $7 stock before the financial crisis hit in 2008. I don’t see any reason why they can’t return to a level somewhere between those two numbers.

Bank of Commerce Holdings (Ticker: BOCH)

I learned about Bank of Commerce Holdings from a BNN Market Call with Benj Gallander, the Contrarian Investor guy. He had BOCH as a top pick and I was looking for regional banks at the time so I took a look at the stock and bought some at $3.25. Watching Market Call is a hit and miss time investment, you can sit there and watch episode after episode and get nothing out of it, but every once in a while there will be a gem. BOCH was one of those gems.

Bank of Commerce Holdings is steady as she goes. I’m not quite sure how they have done it, but BOCH has managed to keep nonperforming assets at reasonable levels (2.45% in Q1 which was down from 2.68% in Q4 2011) while operating in one of the hardest hit real estate markets (Sacramento). To be fair they also operate in a second market, Redding California, which didn’t have quite as bad of a housing decline.

The company has been consistently reporting return on assets (ROA) of 1% and return on equity (ROE) of 8-9% for the last 3 quarters.

Much like Rurban, the first quarter seasonally has lower mortgage banking revenues than does the fourth quarter so I am not concerned about the decline in ROE and ROA sequentially. Mortgage banking is a big part of Bank of Commerce Holdings banking business so they are subject to these seasonal effects. What is more relevant is the trend in mortgage banking revenues. They have climbed substantially from $2.5M in Q1 2011 to $5M in Q1 2012.

Much like Rurban, the first quarter seasonally has lower mortgage banking revenues than does the fourth quarter so I am not concerned about the decline in ROE and ROA sequentially. Mortgage banking is a big part of Bank of Commerce Holdings banking business so they are subject to these seasonal effects. What is more relevant is the trend in mortgage banking revenues. They have climbed substantially from $2.5M in Q1 2011 to $5M in Q1 2012.

Bank of Commerce Holdings earned 35 cents per share in 2011 and 31 cents per share in 2010. I would expect them to earn over 40 cents per share in 2012. BOCH is not going to be a shooting star type of a performer. Its not going to double in a year. But the company is consistently profitable and consistently adding to shareholder value. There is also the chance for them to raise ROE above 10% and ROA above 1% by increasing their operational efficiencies. I hope to see this occur over the next year as the economy improves and opportunities present themselves. I think it is reasonable to expect the stock to trade to the $5.50 range by the end of 2012. That is good enough for me.

Bank of Commerce Holdings earned 35 cents per share in 2011 and 31 cents per share in 2010. I would expect them to earn over 40 cents per share in 2012. BOCH is not going to be a shooting star type of a performer. Its not going to double in a year. But the company is consistently profitable and consistently adding to shareholder value. There is also the chance for them to raise ROE above 10% and ROA above 1% by increasing their operational efficiencies. I hope to see this occur over the next year as the economy improves and opportunities present themselves. I think it is reasonable to expect the stock to trade to the $5.50 range by the end of 2012. That is good enough for me.