Week 59 Optimism

Portfolio Performance

Portfolio Composition

(note that US stock prices are converted to equivalent Canadian dollar prices)

(note that US stock prices are converted to equivalent Canadian dollar prices)

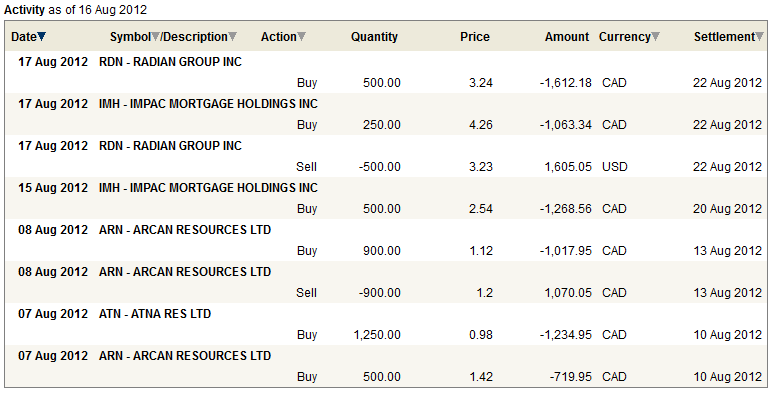

Click here for the last two weeks of trades.

Portfolio Summary

If we lived in a world where we could have perfect understanding, there would be no such thing as an optimist or a pessimist. In such a world we would be able to comprehend the extent of all current conditions and evaluate the events to come by extrapolating those conditions into the future.

Instead, however, we live in a world that is too complex to understand with much certainty at all, and therefore our predictions are at best educated guesses.

Of course there are times when pessimism is warranted. Times such as the fall of 2008, where, if you understood the intricacies of the mortgage market and the speculative excesses that it had come to embody, you could have drawn a number of pessimistic conclusions with sufficient certainty, and having that pessimism would have been profitable.

And, to be sure, there are many times when the best course of action is to shrug your shoulders and walk away. I’ve done just that on more than one occasion over the course of my investing life and over the life of this blog. There is little tolerance for a hero in this game.

But you can’t walk away from everything, and rarely can conclusions be clearly drawn. If a choice is to be made, the eventual direction often comes down to whether you look upon the current set of conditions optimistically or pessimistically. And I think in the end the choice is as much determined by the view of the world you wish to embody than your evaluation of the cold, hard facts.

As a general rule, while I allow myself to be swayed from optimism to pessimism with the market, I prefer to be on the optimistic side and I tie my rope securely to that dock for the long run.

The reality is that focusing on the negatives is a tough way to make money. How many great ideas are conceived within the depths of despondency? I think it’s a rare soul that has the constitution of someone like Jim Chanos; to devote themselves to the discovery of the flaws created by others and use that to their own advantage.

I think that when I am too pessimistic I have a lot of difficulty seeing the potential of what something might become. And because of that I will err on the side of caution and miss out on opportunity. While caution is often prudent, caution alone will not beat the market. Caution will doom you to a life of mediocre returns.

It simply does not pay to be too pessimistic. For every 2008, where the bears rule the day and laugh at the collapsing bulls, there are years upon years of bull markets, in this sector or that, usually born out of the depths of a pessimistic bottom. I realize that we can focus today on the outsized debts and unfixed Europe, and we do indeed need to keep a ready eye on both. But are we really so sure the dire ends we are told these debts forebode is so inevitable? I think we often forget just how much healing a good dose of growth can do, how little we understand what truly underpins growth and how often our expectations of growth turn out to be wrong. In particular, the United States is now 7 years into a massive and probably once in a life time housing correction. What if it ends?

We rarely ever identify the turn ahead of time. It is only looking back that we can point to signs that in retrospect appear unmistakable. But at the time those signs appeared as a one-off fluke to the upside or a dead-cat bounce. It is only after a stock breaks out that it becomes inevitable that it would do so.

Yesterday I posted about Impac Mortgage, which I bought last week. Two weeks ago I talked extensively (and hopefully realistically) about the problems that MGIC and Radian have and why I was willing to optimistically bet that they will find a way out of what still remains quite messy. I am finishing up a piece on PremierWest Bancorp, which looks to me to be turning around after a miserable performance over the past year. In all cases I am carefully weighing my conclusions, never getting to zealous in my conviction, but, above all, I am trying to look optimistically at what might happen if things start to go a bit right.

It is a strategy that has worked better for than a pillow.

{kind=link}

Jim Chanos, not John. I think being overly optimistic or pessimistic clouds thought and insight. You bring up a good point about focusing too much on cold hard facts, however I argue that having an ability to correctly predict where things (companies, economies, etc) are going is a better strategy than making determination based on how one wishes to embody the world. This can often be seen in the angel and VC space where an overly optimistic thinker wishes to create a revolutionary product (or just a basic product) and ultimately fails.

I don’t disagree with your argument. I just think that we often think that are conclusions are more objective than they actually are. Thanks for the correction.