Week 70: A stock pickers Market

Portfolio Performance

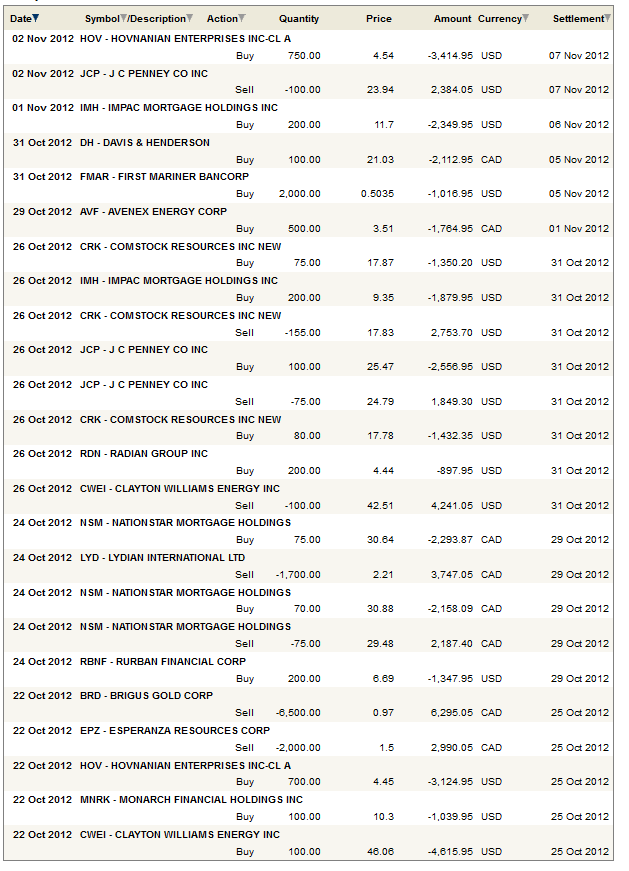

(Note that I am now posting my portfolio composition and list of trades at the end of the post)

Update

I didn’t get around to writing an update last week because I was busy with other research that could not wait. So its been 3 weeks since I updated my portfolio and transactions and quite a bit has happened over that time.

Over time my portfolio has slowly morphed into a vehicle for playing the housing recovery. I had large moves to the upside in a number of my housing related positions, with the most pronounced being of course Impac Mortgage (IMH), but also from Radian Group (RDN), MGIC (MTG) and a number of my regional banks with strong mortgage banking operations. Its been a good 3 weeks.

In this post I want to talk about some of the changes I’ve made over the last 3 weeks. To summarize:

- I sold out of all my gold stocks other then Atna Resources (ATN)

- I made a brief foray into, and then out of, US E&P’s

- I am out of JC Penney (JCP)… for now

- I am into Avenex Energy (AVF) and a homebuilder (HOV)

I will address each of these in order, followed by a brief discussion of what to expect from Nam Tai, which reports earning on Monday and of which I want to be clear of my expectations and actions. But first I want to talk generally for a moment.

I’m finding that I am using twitter quite a bit to post what I am doing on a more regular basis. Whenever I find a relevant article, or if I start to buy a new stock, I try to put a post up on twitter. I have also found a number of folks on there that have been useful to follow. Its a useful tool, and has the advantage over the traditional message board format in that you follow a person rather than a subject. So you aren’t wading through garbage to find nuggets. You can follow me @LSigurd.

Its a stock pickers market

I have heard a lot of negative comments about the market lately. That the market is broken, that a collapse is coming, that the money printing isn’t working and the bottom will fall out. I am not in that camp. While I have never been one to believe that the Federal Reserve could push the stock market into a new bull run only by printing dollars, I do believe that by doing so they can put a floor under the market. The Bernanke put analog is apt. I think we are likely in a market that, as a whole, is constrained to the upside by a weakly growing economy and buoyed from the downside by all the money being printed around the world. That one should not fight the Fed has been a true axiom for a very long time; that one should most definitely not fight the combined weight of the BOJ, ECB, BOE, and the Federal Reserve seems a sensible extension.

And I’m fine with that. It is a stock pickers market. There are sectors and stocks that will do well (ie. the housing industry) and those that will do poorly (witness the collapse of technology earnings witnessed in Q3). What I hated about last year was that all correlation had seemingly gone to 1. The movement of a stock on any given day was forecast best by understanding the latest move in Europe then it was by knowing the company itself. That, in my opinion, is broken market. When you can’t make a reasonable judgment about the future of a business and expect to see that judgment realized in the price of the stock over time, well when that happens it’s all out the window. That was the environment we were in. But it no longer appears to be the case.

Its fun again.

Barrons on Radian

There was a piece published in Barrons this weekend on Radian Group. Barrons is free this weekend so anyone can access it here. The article is basically a re-hash of the arguments written in this SeekingAlpha piece by Oliver Davies. Honestly, there is so much overlap between the two articles that I hope that the writer of the Barrons piece, Jonathan Laing, contacted Davies before writing it. It seems like it was taken directly from it in my opinion.

I have already considered the arguments and came up with my own spreadsheet model to see if they hold water in my post, Does Radian Guaranty have a liquidity problem? I have yet to hear of any major errors in my analysis, and it is an analysis I have went over a number of times since then in order to verify, so I remain of the opinion that my analysis is fair and that my conclusion that Radian Guaranty will not run into a liquidity problem absent another drop in housing prices stands.

I have to wonder whether Johnathan Laing ran his own cash flow analysis before publishing his work. Did he create a model that showed Radian Guaranty would run out of cash? I would love to see that model. I am not academic about this argument; if someone can prove me wrong I will sell my stock and move on. I really couldn’t care less whether I am right or not, I only want to make money on the opportunity. But it does irk me a little to see a publication like Barrons develop their argument around the circumstantial evidence of what management has said and done over the past year if they haven’t done the needed work of running out the Radian Guaranty portfolio and looked at what the cash actually turns out to be. And comments in the article, particularly the one’s which compare current cash against total future claims, seem to suggest that is exactly what they did. There was no mention in the article about the future cash flow coming into Radian Guaranty from new insurance written. In fact this cash flow was referred to as a “trickle”. My model estimated that cash flow from premiums at Radian Guaranty would be in the order of $750 million in 2013. Needless to say, this is hardly a trickle and has a significant impact on the analysis of whether the cash will be available to pay claims.

The Barrons article also focused on arguments that have been discredited since the second quarter. Radian released their third quarter last week, and some of the insights provided by the company were in direct conflict with the arguments made by the article. For instance, the article argues that Radian has been focused on the single premium business in order to raise cash up front (the single premium business results in a lump sum premium at the beginning of the policy, rather than a monthly amount paid over the life of the policy). While there has been some truth to this argument in the past in the third quarter Radian focused their business back to the monthly premium side, and they said on their conference call that they intend to continue to do this going forward. If Radian is truly using the single premium business as a way of raising cash up front (which actually, in my opinion, is not such a stupid thing to do given their circumstance. It was simply a pragmatic business decision) then stopping now, with this presumably gaping cash hole on the horizon, would be foolish.

The arguments Barrons makes that point to issues with the cure assumptions raise valid questions, and I have fretted over them myself in my piece “Things that worry me about the Mortgage Insurers“. But what I would have liked to hear was a rebuttal of management’s explanation as to why they believe their cure rates are appropriate. Radian Group has gone into much detail over the past 3 or 4 conference calls to lay out the case why they believe the late stage delinquency bucket assumptions are correct. Why not address these and rebut them in the article? Instead Barrons chose to use unqualified superlatives such as “wildly optimistic” and dismisses the subject as a con job. What good is that to me?

And really, that is my point here. As someone who is interested in making a decision to buy or sell, an unsubstantiated opinion is not useful to me. Circumstantial evidence is exactly that. I need an argument backed up by facts, that I can weigh and make a decision based on. I can do nothing with what they give me. It seems to me that the only way one can truly get comfortable with a conclusion that Radian is or isn’t on the cusp of a liquidity problem is by making assumptions about the cash coming in from premiums and the cash going out for claims and seeing how it plays out. I didn’t do that work for my own enjoyment, I did it because it seemed to me to be necessary. It still does. But Barrons seems to believe otherwise.

Out of Gold Stocks (mostly)

On September 14th, the day after the Federal Reserve announced that they would be quantitatively easing indefinitely, I wrote a piece called Yesterday’s David Tepper Moment where I explained that I had made a broad move into gold equities on the expectation that gold prices would remain strong with so much easing going around.

To be blunt, it hasn’t worked out like I thought it would. I got a great move out of OceanaGold, which I sold a few weeks back, and a decent move out of Atna, but both of those moves could just as easily be attributed to company specific effects. The overall move in gold stocks has been lacklustre, and with the big companies reporting pretty blah results this week, its hard to imagine much excitement being generated.

I mentioned in my last write-up (Sitting Tight) that with gold now so dependent on Fed easing, that any improvement to the US economy would mean a hit to gold and that I was becoming uncomfortable with this.

I sold out of OceanaGold this week, and trimmed some Esperenza Resources. In both cases, the stocks have moved a lot in only a few months and have reached levels where, when I bought them, I would have been happy to have let them go. I also remain concerned (excited?) that the US economy may surprise to the upside over the next couple of months and that gold may take a hit when that happens so I wanted to take some profits before anything like that happens.

Last week and this I completed this thought by selling out of all my remaining gold stocks with the single exception of Atna Resources. While Atna and OceanaGold were bets on company catalysts, the other companies I bought (Lydian International and Brigus Gold) were more plays on a revaluation of gold stocks in general. That does not appear to be happening.

Atna I will continue to hold because I don’t belief the value of Pinson is reflected in the share price. I remain on the look out for gold producers that are about to make a step change in production and where that step change is not reflected in the market. The move in OceanaGold is evidence how this sort of step change is not always reflected in the price until very near the time that production has commenced. That you can front run this for a decent return is a good game to play.

As for the idea of gold itself, it is an interesting case of what to do when an idea makes sense, but simply isn’t working out. As much as I want to believe that quantitative easing throughout the US and Europe should mean higher gold prices, it isn’t happening. Whether that is because Indian demand is slow, because the US economy is recovering (though you’d hardly assume that from the stock market these days), because Romney is going to be elected or because of some other factor, I will leave it to others to pontificate. I just know that what should be happening hasn’t, so I obviously don’t understand all the factors at play. So I’m going to sit this one out until I get the response to confirm the thesis.

Into and then out of E&Ps

If you look at my transactions over the last three weeks, you will note the somewhat schizophrenic move into and out of a couple of E&P’s. I bought Clayton Williams, only to sell it four days later, and bought and sold, bought and sold Comstock over a two day period. Overall, apart from losing a few dollars it amounted to not very much at all.

On top of this, I actually spent a lot of my time over the last week researching Eagleford producers. But much like the above selling, very little in the way of pragmatic ideas came out of it.

The reason is this. I am having trouble getting comfortable with the natural gas trade and having trouble getting comfortable with the horizontal multifrac trade. While I see the story in natural gas, that of a reduced rig count finally working its way through to reduced production, compounded by large first year declines in horizontal multi-frac wells, potentially helped by a long overdue cold winter, I just can’t find that gas stock that feels right to me. Honestly, the closest thing I have found remains Equal, which with the sale of the Canadian assets and the Mississippian is now mainly focused on a Hunton formation that is most gas and light condensates. And its cheap. The other producers I see are either expensive, unless you start looking forward to $8+ natural gas, which is more like my end game than my starting point, or they are in honest to goodness trouble with massive capital spending and big debts that will barely be covered by a double in the price of gas.

With respect to the horizontal multi-frac wells, I did a bunch of work on the Eagleford over the last few weeks, work that started out as an investigation into the Pearsall shale that apparently Cabot drilled into and produced a boomer from. There was a post on investorsvillage that clued me into the story.

The well was a short lateral with 11 frac stages and produced a 24 hr IP of 1,400 Boe, over half of which was black oil. The nat gas part was also liquids rich. Cabot has joint ventured some of their Pearsall acreage with Osaka for $14,000 per net acre. The higher Eagle Ford, Buda, and Austin Chalk are not part of the joint venture.

I started to look for an angle of how to play this last weekend, searching through a number of companies including USEG, ECCE, MTDR, CRZO and CXPO. The end result though was that even though a lot of these stocks are down significantly from their highs, the capital expenditures required are so high (they approach $10 million per well in the Eastern Eagleford and are over $8 million in the west) that it is going to take one heck of a well to even break even. Just to throw some numbers at it to get a feel, if you can drill a well that on average produced 200 bbl/d of oil at a $50 netback for the first year, you would return $3.65 million of cash.

And while I see all of the very high IP’s that are published from the Eagleford producers, I don’t see much information with respect to how wells are producing 6 months or even a year out. There are a few exceptions, but usually these come from known sweet spots like where EOG has drilled. The little bit of anecdotal evidence I was able to dig up left me with more questions then answers.

Its not so much that I have a negative opionion of the Eagleford producers as much as it is that I can’t get comfortable with them given the information that is available. $8 million or $10 million dollars is a lot of money to be putting out up front, and so you need to see some very good production rates for a sustained amount of time to justify that capital and that risk. In the end, I just couldn’t justify mine.

Out of JC Penney

I have a write-up of my reasons for getting into JC Penny in the first place which I never published because I just couldn’t get comfortable enough with the idea to make it a decent sized position (if you want a copy, just email me). This is mostly because I don’t understand the retail business all that well, and so though I expect that in the long run JC Penney puts together a strategy that leads to profitability, I’m not really sure what happens in the mean time. With the Christmas season approaching and with some other new stocks appearing more clear to me, I decided to let this one go for the moment. However I expect I will be revisiting the story before too long.

Into Avenex

I will do a full write-up on Avenex at a later date. I took a look at Avenex originally after someone pointed out to me that it had a dividend over 13% and asked whether it was sustainable. My answer at the time was “I’m not sure”, an answer that still stands by the way, and that I didn’t love their oil and gas assets. What I did like, and what really kind of surprised me, was that Avenex is a players (albeit a small one) in the oil by rails business. I’ve been doing more research on oil by rails and it looks to me like a case of the temporary-permanent solution. The more I look at the business Avenex has, the more I think they may be on to something. This is a situation where I have established a starting position, and have done enough research to get a sense that there might be something here, but I’m by no means confident in my decision. More digging is required.

Into Hovnanian

I bought a homebuilder! After missing most of the move over the last nine months, maybe I will regret doing this. Nevertheless, when I look at Hovnanian, what I see is the leverage to improved housing starts that seems likely to occur next year and thereafter. The basic idea is that increased starts are going to help a company like Hovnanian both on the volume and the margin side, and that we’ll see the same sort of dramatic swing to profitability that we saw to losses in 2007. After listening to the last few Hovnanian conference calls I was encouraged by the comments explaining how the private builder business was basically dead, which has eliminated significant competition for the remaining builders, and that new land purchased and developed is seeing return on investment above 20%. The company still has a terribly ugly balance sheet (with a negative book value) and is only making money because of tax considerations, but that’s why the stock is $4. I was also somewhat encouraged to see Arne Alsin pick Hovanian as one of his top 10 picks on Friday. I have found Alsin to be an astute picker of stocks in the past.

What to expect from Nam Tai

In short, I don’t know what to expect from Nam Tai. The company reports earnings on Monday. The stock shot up to over $11 early last week, only to fall again on Friday. The fall was caused by this Seeking Alpha article on the company. The article outlined 4 reasons why guidance going forward may be somewhat lacking. The reasons were:

- There appears to be excessive IPad inventory out there, which may lead to slower orders in the near term

- Apple is having trouble with IPhone manufacturing and this may slow orders for the IPhone displays

- There is evidence that Apple is squeezing margins on its suppliers

- Sharp’s going concern risk

I have been following the space pretty closely and so I knew about the IPad inventory issues and the going concern clause that Sharp disclosed. But the stock was looking healthy and so I didn’t really pay it that much attention. I read the article early on Friday before the stock responded and thought about lightening up, but decided that I would wait it out until earnings on Monday to see what management had to say.

There is a lot of heresay going on with Nam Tai right now, and we will know a lot more after management weighs in. Waiting it out may mean that I will be exiting at a lower price, but its equally possible that I will be holding at a higher one. Either way I will be able to make a more informed decisions than I can right now.

I think that what is useful, and why I wanted to write this piece, was to clarify the reasons for investing in the stock. I don’t have a particularly strong belief in the long term potential of the contract manufacturing industry. I don’t like the business; I think its continually getting its margins squeezed and its often at risk of being pulled for the lower cost supplier. Nam Tai has a strike against it for this reason. The investment idea was that the Apple contracts would improve earnings substantially, and that the continuing ramp announced along with the third quarter and the guidance going forward would be strong enough to support a higher stock price.

If something to this end does not play out on Monday I think we are playing a waiting game. That is not as enticing to me here because of the business. I can be very patient when I feel like I have the business on my side, as I have been with the regional banks I own, as I have been with the mortgage insurers. But I don’t feel that way with contract manufacturing. It may be my own bias, or my own ignorance of the business model, but sitting on a contract manufacturer waiting for some good news to materialize doesn’t strike me as an enticing proposition.

Anyways that’s where I stand. I hold my position. I will be watching closely on Monday. I will be hoping for the best. But I will exit without prejudice if this isn’t playing out the way I expected.

Looking Ahead

In my inexhaustible attempt to come up with the next big idea, here is a brief list of the stocks I am looking at now:

- Davis and Henderson – one of their businesses is mortgage origination and compliance software

- IDT – long story but I like how cheap it is, and they have this funny little cloud based video business that seems to be deriving a surprising amount of cash

- Oil by rails – looking for other ways to play this

- Natural Gas – if I could ever find a natural gas company that is not deeply in debt, spending obscene amounts of capital that it does not have the cash to cover, or trading at some ridiculous multiple to cash flow, I would be happy

- Another Impac Mortgage – If known of, please contact me…

Portfolio Composition

Note: I have begun to add all new US holdings in US dollars. This will make it easier to distinguish between US dollar and CDN dollar holdings. However, I cannot move currencies for existing stocks and preserve gains so existing US stocks in the portfolio will continue to show up in the CDN Holdings portfolio

Also note that the Nationstar % Gain/Loss is wrong. There has been a glitch in this number since I sold half of my position.

Click here for the last two weeks of trades.

{kind=link}

If you like oil by rail plays, check out Ceres Global Ag Corp (CRP.TO). This used to be a listed closed-end fund investing in Ag stocks, but in 2010 they bought grain storage facilities from a hedge fund and now they are more or less an operating company (although they still own a few stocks like ECO.TO). Riverland has a capacity of 55M bushels (wheats, oats and barley). They have been struggling the last few quarters to refill the silo’s, but my guess is that they have turned the corner. The ending of the Canadian Wheat Board monopoly is bullish for Riverland as well as it gives them more sourcing options.

Book value of their storage facilities is over $ 10 per share, but the replacement value is probably much higher. Current share price is $ 6.. And there is a lot of M&A activity in grain storage. Ceres is actively buying back shares. Ceres is managed by Front Street out of Toronto. The partners, Frank Mersch, Gary Selke et al, have a significant ownership in Ceres (>20% combined), so their interest is more into an accretive deal in the future than to just ‘milk’ this with the yearly management fee).

Now for the oil by rail play, Ceres has an 25% investment in Stewart Southern Railway. It turned a profit in the last quarter. Ceres is looking to expand their emerging commodity logistics division. In june about 13,000 barrels of oil per day were transported from Saskatchewan over this Railway.

So the oil is still a bit of a side show, but that might chance. It gives me an excuse to bring up CRP 🙂

Thanks for your contributions, it is a great pleasure to read your investment analyses.

Cheers.

Thanks for the idea. It sounds interesting. I’ll try to take a look at it in the upcoming weeks.