Extending the idea of Extendicare

I am more superstitious than I would like to admit. For example, when I was a kid I used to take the same number of steps to my bedroom, close my door before bed to the same angle, and never step on a crack on my way to school.

Nowadays I’ve toned things down a bit but I still have a few little rituals, many of which revolve around investing. I always check MSFT when I log in before checking any other symbol (even though I don’t own it), I never check the price of a Canadian stock on Yahoo! Finance, and from time to time I “sacrifice” some stock to the gods when a particular security isn’t going my way.

While superstition can be dangerous if its left to run awry over one’s decision making, if its kept in check it is not entirely a bad thing. While we all like to believe that we are rational and objective and that therefore our conclusions always stand on their own accord, I think this is mostly a delusion. Our convictions are more based on faith than we would like to admit.

From this observation comes the usefulness of coincidence. If a leap can be made, even somewhat half-heartedly, that coincidence is born of some sort of necessary intent, its conceivable to think that this might bond you to the event that you would otherwise disregard. The result can be constructive: a firmer stand of integrity, an oath more closely held. Under less desperate circumstances, it may simply lead us to pursue an opportunity that we may have otherwise ignored.

What this has to do with Extendicare

A couple of weeks ago I was talking to a broker who had recommended Extendicare (EXE.to) to me. I asked him what he thought of the company now. He explained how he thought the market had this totally wrong, that the case could be made for a higher valuation, that the hidden value of the company may be realized in the next 6 months and that the case for its undervaluation had been laid out in some detail by an analyst (from GMP) on the conference call that discussed the dividend reduction that led to the recent collapse in the share price.

While I thought it sounded like an interesting scenario worthy of further investigation, I do not know if I would have pursued the idea (A healthcare company with a recently cut dividend and a complicated US/Canadian structure that is not easy to disentangle is not the sort of slog I put myself through merrily) had it not come up again the very same day.

A few hours later @petienne tweeted about a recent write-up of the company that laid out a convincing bullish case. To have lightning strike twice is enough providence for me, and I spent the night researching Extendicare in detail. I subsequently I wrote a short summary about the thesis in my monthly portfolio update.

Both the GMP analyst comments and the write-up, which I was able to review and has been made available here, pointed to the valuation discrepancy between Extendicare and its peers in the Canadian and US market. The essence of the comments made by GMP can be summarized by the following points:

- Extendicare has said that their U.S operations are not materially different than the other publicly traded skilled nursing companies in the U.S

- Other publicly traded skilled nursing companies in the US trade at well over $100K per bed

- Given the number of beds Extendicare has, if you look at your value for those beds it is at a 50% discount to what the market is valuing competitors

- That valuation discrepancy is $800mm which works out to almost $10 per share

A similar thesis was expressed in the aforementioned report.

The work that I have done is to evaluate both the Canadian and US operations against its competition and confirm the valuation discrepancy. For a guide to whom the competition is, I am indebted to the write-up provided by @petienne. The write-up referred to a number of close competitors on the US side, and I primarily used those companies as my comparatives. Apart from the names though, the rest of the analysis is my own and so I am responsible for any of its mistakes.

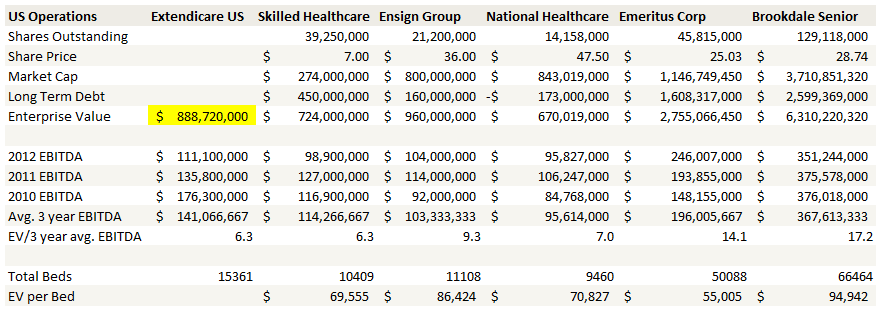

First, lets compare Extendicare to its US competitors.

Extendicare’s US operation enterprise value, which is highlighted in yellow, is based on the lowest EV/EBITDA of its competitors. This is conservative, but perhaps not as much as it seems because Skilled Healthcare looks to be the company with the closest comparables to Extendicare.

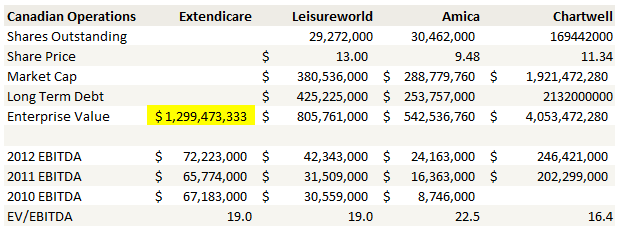

I made the same sort of comparison for the Canadian operations. Extendicare’s competition in Canada trade at a much higher multiple than their American counterparts. One could certainly argue that the entire Canadian healthcare sector is overvalued based on these multiples. But their justification is that Canadian health care system is a much more stable operating platform; these companies essentially trade on their dividend, which is sustainable. I chose the multiple of Leisureworld for my enterprise value since they are the most similar competitor.

At $6.80 (which is my average purchase price but above the current price of $6.50) the market capitalization of Extendicare is about $585 million. The company has long-term debt of $1.1 billion. Based on the low-end comparables in the above tables, the Canadian and US operation, valued separately, would be worth about $2.2 billion. At that valuation the stock price would be about $12.80, or double the current price.

Its worth noting that Leisureworld pays a dividend of 90c annually. At the current share price that is about 7%. On the conference call Extendicare suggested that their current dividend (48c annually) was effectively that which was sustainable for the Canadian operations. Given the same yield, that would put the stock price at about $7 per share (which of course gives no value to the US operations).

Its also worth noting that I am making all of my comparisons based on a US company model whereby the operations and real estate reside within a single company. There appears to be further upside if you make comparisons to US companies that have split the operating company from the property holding company (this is something that was discussed in some detail in the note I linked to). The extra value is associated with the property holder, who gets a premium multiple because the risk of vacancy is low and so a steady income stream is fairly certain. But I haven’t done the work on this so I am going off of second hand knowledge here. I view this as a nice surprise if it happens but I will be happy if my returns in the stock approach the more conservative value above.

What are the Risks?

There are a number of risks associated with the US operations. These risks are the reasons Extendicare gave for reducing its dividend. They can be distilled down to the following points:

- Uncertainty about future government funding levels due to the inability to pay (this has been realized to some degree already with sequestration)

- Uncertainty with respect to the changes in the funding model brought on by Obamacare

- A secular shift towards alternative care; the use of home-care and assisted living to provide a broader range of services

With respect to the third item, the company provided a lot of color on where their industry is going on the last few conference calls. The secular shift mentioned above is the movement of longer-term patients away from the skilled-care setting (which Extendicare provides) into lower-care (and presumably lower cost) alternatives. Extendicare is thus undergoing a change to their patient mix; they expect that stays of their patients will be shorter, that this will likely result in lower occupancy rates (called the occupancy census) but that the amount of care required by the patients staying with them will go up (referred to in the industry by the skilled census).

The company admits that this industry shift is creating uncertainty, and that participants will have to adjust. I thought it was interesting that Tim Lukenda, the CEO, gave some color to the unfolding scenario, saying that the change was “causing providers across the continuum to figure out how to align with each other and carve out their piece within the continuum”. This seems a like clear (well maybe a little less than clear) way of saying that a merger wave is about to occur.

I would be less sanguine about the risks if it was not for the direct comparables in the public market that are being valued every day at a significant premium to Extendicare. In particular, Skilled Healthcare is very comparable to Extendicare, being a similar size (~10,000 beds versus ~15,000 beds), having much of their operations in northern states (though Skilled Healthcare does also have operations in Texas and California) and deriving the vast majority of their revenue from skilled nursing facilities (about 10% of Skilled Healthcare’s beds are assisted living, which is one step down the care ladder from skilled nursing).

The Long-term remains Attractive

While there are short-term funding concerns with the skilled-care industry, there can be no doubt that over the long run owning beds that care for the elderly is going to be a growth business.

While I would not invest in a company based on such a long-term trend (events that are going to play out over a 30 year horizon are a bit too slow for my liking), there are plenty of others that would happily take the long-term above average returns that it should garner. I really need just one, maybe a private equity firm, or a consolidator looking to “align themselves to the continuum”.

Management has said that the board has been investigating the split of the Canadian and US operations since late-2012 and that they have had Citigroup involved in that process since that time. Recently they took on Citigroup in a more formal role. Listening to their comments and reading the following excerpt from the first quarter news release makes it clear to me that the separation of the two businesses is a matter of time and not a question of “if”.

The Board has been reviewing strategic alternatives relating to the separation of the two businesses and has made substantial and significant progress to date to identify and execute on a realignment of the Company’s businesses. Last year, the Board appointed a Strategic Committee to focus on this initiative which has retained CitiGroup Global Markets Inc., as a financial advisor. The Strategic Committee is in the process of evaluating th e specific technique and form of the separation, which may take the form of a sale of the U.S. business or, alternatively, a distribution by the Company of the Canadian or U.S. business (which would give shareholders the flexibility to participate in two companies – one company, which would own and operate the Canadian business and a second company, which would own and operate the U.S. business). The Board will adopt the structure that it concludes would be in the best interests of the Company and its shareholders.

The process is expected to conclude before year-end, meaning our window is less than 6 months. Meanwhile, the stock pays a dividend over 7% and I think there is a reasonable chance that the same dividend keeps getting paid after the split. In their report Hawk Ridge Partners called Extendicare “the single biggest valuation anomaly” they had ever seen. Being a smaller investor who is able to search out tiny companies overlooked by the market, I’m not sure I would go that far, but it is nevertheless a compelling opportunity with a short time horizon. Event driven I would say, if I were in the biz. But I’m not in the biz, so I will just call it an opportunity to make money.

Clear thesis, thanks.

User petienne on Twitter does not appear to be a stock blogger. Do you have another Twitter ID?

Do you have any updated thoughts on this? It seems like a timely idea.

I’m still holding and waiting. The company said they expected a deal by YE so I’m hoping for something in the coming days. We will see.

10 points for your thesis and explanation, well done.

Is there any news about the sale?

Greetings from Spain.

Its drags on infinitum

What do you think of last Q’s earnings? I wonder if performance would have impact on valuation. Right now, they’re only negotiating with one party and no timeline. Someone thinks this could be a change of control transaction, which should unlock more value.

Can you explain what a change of control would mean here? I’m not sure I understand.

I honestly have no idea either. That’s just something the Hawk Ridge guy said on his VIC write-up.

Good update. I suppose a sale should happen soon.

See my post on the weekend.