Week 99: Patience

Portfolio Performance

Portfolio Composition

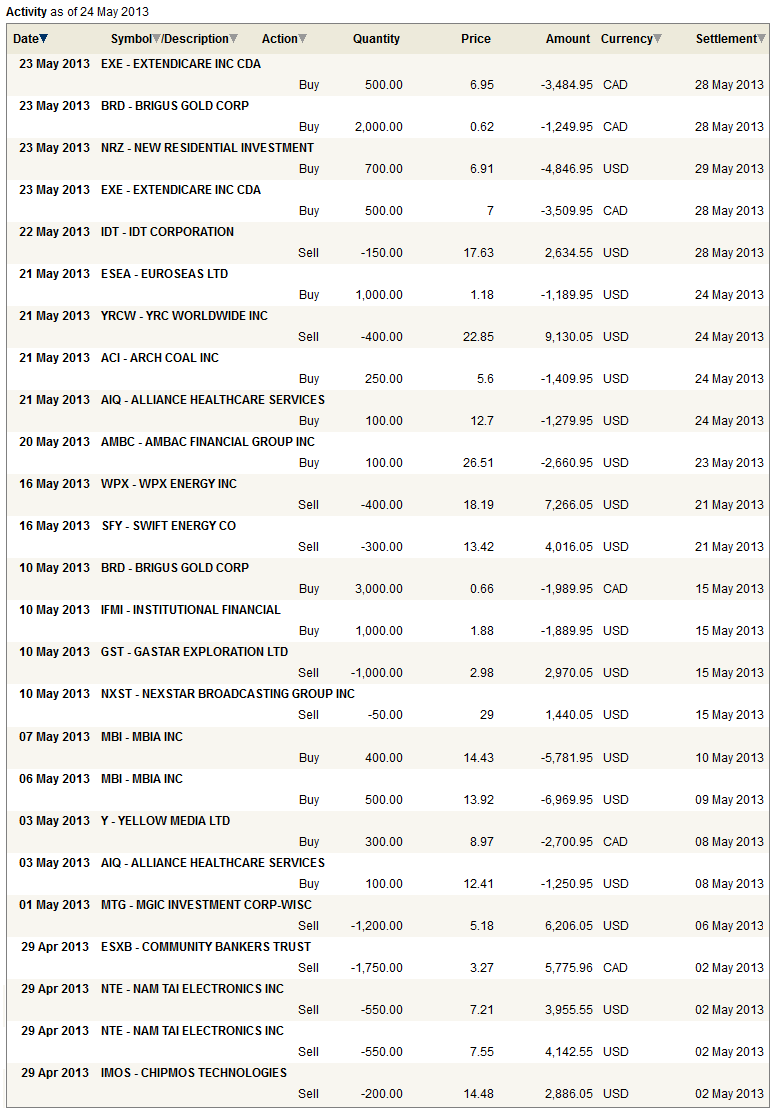

To see the last four weeks of trades, click here.

To see the last four weeks of trades, click here.

Update

Last month was an excellent month for my portfolio. I wrote about some of the significant moves that occurred over the first few weeks of May in this post, and I won’t repeat that discussion here. Apart from what was discussed there, I made only a few changes to my portfolio. I added Ambac (AMBC), which I wrote about here. I removed a number of the natural gas stocks, and I added a couple of new positions in the Health Care sector. I also subtracted and then added back some gold stock names, with the net sum of the moves being close to zero.

Not showing enough patience for Natural Gas

I had bought a basket of natural gas stocks (XCO, WPX and SFY) on the thesis that we could be about to see a turn in the supply/demand dynamic. As the weeks pass by, that turn didn’t seem to be materializing and so I sold (note that I still own Gastar and Equal Energy, which were not bought as “natural gas vehicles” but because of reasons specific to the individual companies). The unknown continues to be whether the rig count, which is languishing at extremely low levels, means anything anymore.

In the article I wrote in April I expressed guarded optimism that production would shortly follow the rig count down, but at the same time I noted that the efficiencies being realized due to pad drilling, multileg horizontals, and longer horizontal lengths could mitigate the falling rig count, and that the end game between these two dynamics was not certain. A month later I remain with the same uncertainty. For now I decided to exit the stocks with intent to re-evaluate in a month or two

Extendicare (EXE)

I am going to write a full article on Extendicare at some point in the next couple of weeks, but for the moment let’s just summarize the basis thesis. Extendicare operates longer-term care facilities in both Canada and the US. The stock crashed at the end of April after the company announced a dividend reduction from 7c to 4c monthly. They reduced the dividend because of uncertainty surrounding their American operations, in particular because of Obamacare and worries about what the eventual profitability of the US business will be when it all plays out.

On the call to discuss the dividend reduction (the April 29th call) an analyst from GMP brought out an interesting discussion. He pointed out that there are companies that are direct comparables to the US and Canadian operations that Extendicare runs and that if you back out the value of Extendicare’s Canadian assets based on its Canadian comparables you realize that the US operations are being valued at a 50% discount to its peers. That 50% discount works out to $9-$10 per share that isn’t in the current stock price. His next comment was rather obvious: why don’t you try to realize this value? I would recommend listening to the dividend reduction call with about 15min left for the relevant discussion.

When the company released the first quarter results on May 9th they announced that they had hired Citigroup to explore strategic alternatives for the company, specifically a split of its Canadian and US businesses. It looks like they are going to try to realize this value. This isn’t something that was precipitated by a vocal analyst; they mentioned on their first quarter conference call that the Board of Directors had began the investigation into strategic alternatives back In 2012, and it was only recently that they reached the point where they felt it was prudent to take the next step and engage Citigroup. The company expects to have something by year end, with that something being either a spin-off or sale of the US assets.

So the scenario with Extendicare is a company that has operations with clear comparables that is undervalued based on those comparables by at least 50% and perhaps quite a bit more and they have set out to realize that discrepancy through either a sale or spinoff of the US operations. Seems like a pretty decent bet to me. I still have work to do on the comparables before I will be ready to put out a more detailed post, but the work I’ve done so far suggests to me that the GMP analyst was correct in his assessment.

Alliance Healthcare (AIQ)

Even though I have a position in Alliance Healthcare it still feels like the one that got away. I started buying Alliance in the low-$9’s. However it is a low volume stock and I was only able to acquire a small position. Soon after I started buying, the stock moved up into the high-$9’s and I decided to wait for a pullback. It never came. I have added since, but in the $11’s and recently more in the $12’s. But I sure wish I could have that $9 price tag back.

There was a very good Seeking Alpha article written about Alliance Healthcare in mid-April that was the original reason I became interested in the company. Unfortunately now that Seeking Alpha has moved to a “pay for” model, articles like this only last a month and therefore you can only read the first couple of paragraphs.

Fortunately Alliance Healthcare story is a straightforward one. Alliance provides radiology services across 45 states. They deliver MRI, PET, CT scans and the like. Their operations are located either at hospitals or nearby a hospital campus, and are they generally operate as direct partners with hospitals to whom they contract out their services, as opposed as to in competition. About 80% of their revenue being derived directly from hospitals.

Alliance Healthcare is a company with bad earnings and great free cash flow generation. The bad earnings are the result of massive depreciation and amortization charges that the company takes on its purchased imaging equipment. The upkeep and maintenance capital the company spends on this equipment is a fraction of its D&A.

At the current price of a little under $13, the company has a market capitalization of $130 million. Because of the debt incurred on the purchase of its imaging assets (there is about $515 million of net debt on the balance sheet), its enterprise value is about $635 million. The company generated EBITDA of $154 million in 2012 and $149 million in 2011. Operating cash flow for each of the last two years was around $100 million, and free cash flow was about $60 million in 2012, and $50 million in 2011.

The company was quite upbeat on its first quarter conference call. Last year they worked on bringing costs down and stabilizing their imaging business. One focus, for example, had been their hospital retention rate. Their retention rate had dropped as low as the mid 70%’s but they have turned that around to where it currently sits in the mid 80%’s and expect to have 90% retention rates by the end of this year. With the business stabilized the company expects to turn its focus to growth and they provided quite a positive qualitative assessment of the growth outlook on the call.

Alliance Healthcare reminds me a bit of Nexstar; both have a lot of debt on their balance sheet but both also have the cash generating ability to maintain it and hopefully bring it down to more acceptable levels. While the stock is not quite as good of a buy at $13 versus $9, I think there is still quite a bit of room left and if it can gain momentum in its move to grow the business, I may be pleasantly surprised. It is the sort of position I expect to keep adding to as it rises.

Patience and YRC Worldwide (YRCW)

I tweeted last week that I had sold about one-third of my position in YRC Worldwide. It simply was getting to be a very large position for me, and it wouldn’t have been prudent to take a some profits after the stock had nearly quadrupled. I was lucky enough to get out near the top, at $24 but because I still own a sizable position I have suffered with since as it has fallen 20% to $20.

A pullback had to expected given the size of the move up. Maybe I was foolhardy not to sell my entire position when it passed $24. The reason I didn’t is because I anticipate more positive news in the next few months. The second quarter earnings, absent any restructuring charges, are likely to be quite good. Word has it that Arkansas Best has initiated a rate hike and so a similar move from YRC Worldwide should not be far behind. At the end of May the company will start to see the fruits of the terminal restructuring that has been agreed to. And in what is probably the biggest potential catalyst for another share price revaluation to the upside, I think that an announcement on debt restructuring is not out of the question.

Last week I listened to YRC Worldwide participate in the Wolfe Trahan Conference. By far the quote of the day came from the CFO who said that the “capital markets are hot” and “grossly in favor of the issuer”, that “YRC Worldwide has more options than they have in the past”, that the company is “considering a variety of options” and “will take care of [the debt] before it comes due.” Obviously a reduction of interest paid and lengthening of maturities would be a huge positive for the stock. So I hold.

My Plight as a Macro-tourist

Kyle Bass coined the phrase macro-tourist to refer to those going long Japanese equities with little understanding of the machinations of the Bank of Japan and Ministry of Finance. While its a great phrase, connating just the right amount of contempt, I think the same phrase could be applied to most of us who are long equities, especially us retail suckers, your’s truly included.

As much as I have tried to understand the dynamics that govern the macro-economy I still consider myself only modestly equipped. Most importantly, I have little confidence in my own predictive capacity. Thus, while to me it seems all but certain that Kyle Bass will be proven correct about Japan at some point, I have no idea whether his moment of truth will come tomorrow or five years out. What I do know is that there is a lot of missed opportunities between the former and the latter.

I’ve come to accept my plight as a Macro-tourist. It won’t cause me to stop trying to understand the macro; I’ve been watching the JGB’s diligently since Abe first announced his money printing campaign and I’ve taken my exposure down accordingly as the JGB has collapsed. But I do accept my own limitation to discern the inflection point. As such, I have reconciled it with myself that when whatever it is does hit us, it is quite likely that it will have made an impact before I am able to react.

I think the best thing I can do to prepare for this likelihood is to accept ahead of time that some losses are going to occur and to not let those losses stop me from selling off of the highs. While this seems like a simple objective, it isn’t, and I therefore think it is worth preparing mentally for ahead of time.

{kind=link}

First time commenter – I love reading your posts, very well thought out. What are your thoughts on ESEA?

Kyle Bass IS a macro tourist, so take no offense. http://www.businessinsider.com/kyle-bass-macro-tourist-2013-5

Do you have any idea what happened to Atna? I understand they modified production but this smash in the price seems to discounting something else…any ideas? Thanks

I think it was the CC. They put out numbers that didn’t totally reconcile with one another. At one point they said they had 100,000t of development ore and 80,000oz of gold they can develop but that grade didn’t seem consistent, Sprott questioned them on this and they revised their comment to being 40,000 oz of gold and they also said they have 6-12 months of ore at this rate and the rate they said they are mining at is 3,000t/m but if you do the math on that its only about 1,000oz/m which, if there is 40,000oz available, is a lot more than 6-12 months worth. So I think selling is just people fed up.

For me its a mistake I made. I did sell about 1/3 my position back in March when I sold out of most gold stocks but I kept the other 2/3 so I have been hit. I should have sold out completely like I did with others but I think I had developed a sot spot for the company, which is not a good reason to hold. At this point I haven’t sold the other 2/3 yet b/c its market cap is so low (~$30mm I think) that its not really pricing in any success. Not sure what to do at this level.

Thanks… I emailed the company and this is their reply.

We typically only record quarterly earnings calls, I’m sorry I don’t have a link. During the call we reiterated that we are looking and many options for Pinson including financings or partnerships.

We felt scaling back on operations was the best course of action given that the current mining method and costs were not acceptable. It was a proactive step in not depleting the treasury while we are trying to determine what is going to work best at Pinson. This may involve re-engineering as mentioned in the release before we will know more detail. That is the reason we withdrew production for now until we take a more in depth look. We may decide to use our people instead of contract mining as it may prove to be at a lower cost. We will absolutely convey information as we know more.

Thank you,

Valerie

I guess you’re right….

Disgruntled shareholders issued a stinging rebuke to Atna Resources Limited (TSE:ATN) Friday, saying their trust and confidence in Atna’s management is now “between zero and nothing” following the Golden, Colorado-based company’s announcement two days before that it was downsizing mine operations at its Pinson gold mine near Winnemucca, Nevada, and withdrawing its previous production guidance.

In a newsletter sent to subscribers entitled “Goodbye Atna Resouces”, Gecko Research, a small group of Swedish private investors, wrote: “It’s with a lot of anger and extreme disappointment that we have decided to sell our stake in Atna Resources. The last drop of patience we had left was lost in Wednesday press release.”

Atna’s press release, issued Wednesday, advised that mine operations were to be downsized in light of the current gold market, which came barely two weeks after Gecko had been reassured of the imminent commencement of commercial production. Thus, the Swedish investment group says it was misled and subsequent forecasts were predicated on faulty information.

http://www.stockhouse.com/bullboards/messagedetail.aspx?p=0&m=32629431&l=0&r=0&s=atn&t=LIST

Yah I posted this article on twitter – which is referencing same research: http://www.proactiveinvestors.com/companies/news/44509/shareholders-upbraid-atna-resources-citing-outright-lies-44509.html

I’m not as upset as Gecko – these juniors are speculative, you never know what to expect and so I can’t be surprised when they surprise. I play a lot of speculative/turnaround/developing story stocks so I’m going to get kicked every once in a while. Got kicked with NTE and now with ATN but I’ve had a number of winners too. Its not going to cause me to change my strategy.

Just looked at stockhouse link. Its the same article.

My problem with all this is not the surprise. We’re trading at a level not consistent with the fact that major expenditures for this operation are past and the resources proven. They have a land package and operations yet the stock trades below 2008 levels all because gold corrected? So if gold went up to 1600 we’re back on plan and everything is swell? I just hope they’re not trying too hard to bk the company and transfer ownership again.

I don’t understand why Atna didn’t hedge if their cash/production costs are super high and cant withstand a correction. Or hedge 75%

Why does management look to lower costs (re-engineer their mine) after prices have dropped. If I was management I would be saying to myself each day, how can I produce at a lower cost. Instead management says after gold drops hmm you know what we can re-engineer the mine and save some money.