A Bet on Housing Starts: Ainsworth Lumber

I have been waiting for the right time to get back into lumber stocks. I owned a number of the companies in 2010 and early 2011 but I sold too soon and missed the big moves in names like Western Forest Products, International Forest Products and West Fraser Timber. Since then I have been reluctant to start a position without a significant correction in the stocks first because I know that these companies are extremely volatile and will go into big corrections on the first whiff of macro-worries (because of their cyclical dependence on economic growth and the thin line separating over and under supply).

So I’ve waited and waited and was beginning to think that a correction would never come, but in the last couple of months the price of lumber came off significantly and so have some of the stocks. While the tree-cutting plays, like Western Forest Products and West Fraser, haven’t sold off enough to entice me in, the milling and manufacturing companies have seen bigger corrections.

So I took a position in Ainsworth Lumber. I tweeted the following last Friday:

Why only a half position? Well I’m still not sure about the velocity of the housing recovery. Those who have followed this blog for a while will remember that most of my housing plays over the last year and a half have revolved around the “things are not going to get any worse” idea, rather than the “things are about to get much better” idea (names like Nationstar, Newcastle, PHH Corp, Impac Mortgage, and more recently PennyMac Mortgage and New Residential). That’s why I missed out on the home builders, and why I missed out on the lumber companies and their first leg up.

My uncertainty stems from this: There are a lot of companies/partnerships/trusts buying homes, and to the extent that is driving the recovery will determine the recovery’s strength over the long term. While I suspect that we are seeing a real turn here, I’m not certain of that. So I am wading in, but not too deep. This position in Ainsworth is a bit of a “wait and see” position, as I will watch how things progress.

Manufactured Wood Products

Ainsworth produces oriented strandboard (OSB), which is mainly used in residential housing. The company has mills (I’ve stated the capacity in brackets) in Grande Prairie (730mmsf), Hundred Mile House (440mmsf), Barwick Ont (510 mmsf), and they are bringing on-line a mill in High Level Alberta (860 mmsf) in the third quarter.

The thesis behind Ainsworth is two fold:

- They are generating significant free cash from operations after maintenance capital at current OSB prices

- They are leveraged to further improvements in the housing market through price increases to OSB and through volume increases as they bring on shut-in capacity

Lots of Free Cash

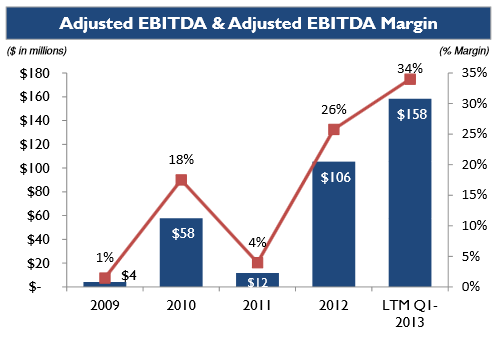

The chart below shows the company’s adjusted EBITDA for the last 3 years and the trailing twelve month period (from the May presentation). Adjusted EBITDA, which ignores one-time and non-cash charges like stock options, has historically been a good representation of operating cash flow for the company after you adjust it for interest costs, which are about $7 million per quarter (coming from $350 million of 7.5% senior notes).

Adjusted EBITDA in the first quarter of 2013, when OSB prices averaged around $420/msf, was $62 million.

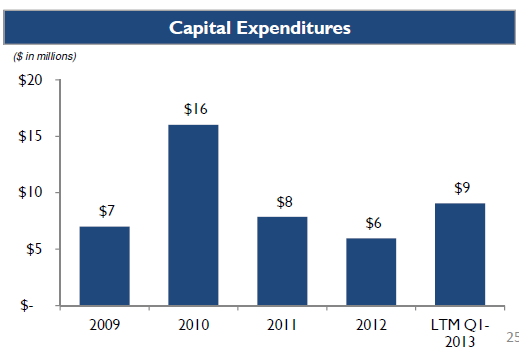

While Ainsworth is deploying a significant amount of capital right now as they bring on-stream the High Level mill, the maintenance capital for the mills, once built, is very low. Below are capital expenditures for the company over the same period.

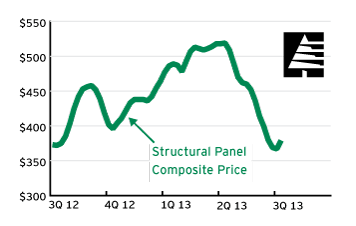

At higher OSB prices such as those realized in the first quarter, Ainsworth would be netting free cash flow of about $52 million per quarter. That would make the current enterprise value about 5x its free cash flow. Of course OSB prices have dropped significantly from their highs and are currently at $270/msf. I haven’t been able to find a good historical chart of OSB prices that I can put up (Madison’s does put a historical chart up periodically but you have to make a copy of it because they refresh which charts on a weekly basis and I’m not quick enough for that) but below I’ve included a structural panel composite price index (from randomlengths.com) that includes both OSB and plywood. You can get a sense from it the trajectory over prices over the last few months.

If the US housing market continues to pick up steam, I don’t expect this downtrend to last. The amount of OSB mill capacity being brought on in 2013 and 2014 will be quickly used up as housing starts in the United States climb towards the 1.7 million level that would be normalized with household formation. But even at these lower OSB prices, Ainsworth does not look overly expensive to me. The current OSB price of $270/msf is approximately the same as the price was in 2012, when Ainsworth generated EBITDA of $106 million. That would put free cash flow generation in the range of $70 million, or 14x the current share price. Given my (rather tentative) expectation that this is the new “trough” in prices, that doesn’t seem like a bad valuation to me.

The second way that Ainsworth can benefit from the improving US housing market is through volume. The company is currently operating at about 2/3 of capacity.

In addition, in the May presentation the company outlined additional capacity additions that could be brought on at Grande Prairie. With expenditures of $80 million and a 12 month lead-time, the company could add another line at Grande Prairie, which would increase OSB production by 600 mmsf annually.

Why Ainsworth and not Norbord?

I don’t have a really strong reason for picking Ainsworth over Norbord. It could easily be said, why not both? The answer I will give is that Ainsworth has come off quite a bit more than Norbord (they are down about 15% in the last 3 months versus only 5% for Norbord from where I purchased, though it has admittedly moved up some since my purchase and tweet on the 5th of July). Ainsworth also appears a bit cheaper on an EBITDA basis than Norbord, and in the near-term there is a production bump from High Level that might be a catalyst for the shares once it is producing OSB.

But from what I can tell, they are quite similar companies and if housing is indeed a one way ticket, you can’t go too far wrong with either.

Risks

The big risks here, and they are one’s I remain wary of, are macro. First is that the housing recovery in the United States is a mirage created by investors and once that demand dries up housing slumps back into a multi-year trough. Second is some sort of external shock to the system; every few months I come back to Japan and how much the Kyle Bass thesis that Japan is going to implode at some point in the next two years makes sense to me. That concern remains out there like some foreboding storm cloud on the horizon, and if it does come to pass, lumber companies, like all other commodity producers, are going to get hit hard. But there isn’t a lot of evidence that this moment is upon us, and so it looks safe to continue to pick up dollars (not pennies) while the bulldozer remains idle. Ainsworth looks like a reasonable place to do this with success.

{kind=link}

Interesting post. As a UK investor not sure I’m familiar enough with US housing to take a punt though.

Do you have a link to a good article on the Kyle Bass thesis on Japan you mentioned?

I would go to youtube and search for Kyle Bass Americatalyst. There are two or three good interviews there at the Americatalyst conference where he outlines his idea in detail.

Interesting idea. Looks cheap with a turn in OSB providing nice upside. You say you are concerned about macro, understandably. Aside from the US housing recovery and its questionable sustainability, there are a lot of grumblings about a US-style housing bust in Canada on the horizon. Being a Canadian citizen, do you have a read on that, and to what extent do you think that type of scenario would affect Ainsworth? Have you broken out Ainsworth’s distribution/sales by region?

I haven’t looked at Ainsworth’s sales breakdown between Canada and US, but what you are saying could be a worry down the road. I’m not really seeing much evidence of a US style collapse here in Canada though, and Canada accounts for about 20% of the demand of the US for lumber in general. I would be more worried about Canada if interest rates rose – at these levels everyone can still afford their home.

@ Lsigurd

I found you blog by chance since we made some similar investments. Great work!

1. Can you be reached by email?

2. Any opinion on CPF:NYSE ?

Thanks – I can be reached by email at liverless at hotmail.ca I haven’t looked at CPF but it looks cheap at a glance. What’s the story?

Ainsworth Lumber ANS is minus 20% in less than two weeks, specially yesterday and today. What’s wrong with this company?