Tying up Loose Ends with the last of my June Position Changes (FFEX, IMH, MBI, TVL,)

As I mentioned in my June update, I was away on vacation for a couple of weeks and at the same time the city I live in was hit with the flood of a century, and these two events transpired to put some delays on the posting all the details of the monthly portfolio update that I put out.

In subsequent posts I have talked about the two major theme changes that I made in June, with those being that I sold all of my gold mining stocks with the only exception being Midas Gold (the decision to sell is looking rather prescient right now) and that I had bought a number of REIT’s that I believed were being sold off indiscriminately by investors lumping together all REITs into a single bucket (maybe not quite as prescient as the gold miner sell but I’m doing okay on this one so far).

There were, however, a couple of other portfolio changes that I made in the month of June that I didn’t get a chance to mention. I want to use this post to do some house-cleaning, talking about the remaining portfolio changes I made in June.

Taking a Position in LIN TV

Nexstar Broadcasting (NXST) has been an excellent stock for me. I’ve seen returns of greater than 100% in 6 months. When I first bought Nexstar I listed it as one of the stocks I was buying as part of my “big idea” for 2013, which was companies that were thought to have too much debt but could now leverage that position as the economy improved.

I have just recently sold Nexstar (something I did only last week) but in June I took a position in and am still holding a very similar company called LIN TV (TVL).

Though it has moved since my purchase, I think that LIN TV is a bit behind the curve price-wise when compared to Nexstar, and I’m hoping that the stock can reach $20 in the next few months.

With both Nexstar and LIN TV, I have to admit that it took me a long while to really “get” the thesis. This is probably one of the reasons that my position in Nexstar was never really that large, and why it took me so long to buy into Lin TV.

The story with both of these names is really the synergies that can be achieved when they take over television stations in the same or adjacent markets. What made this crystal clear to me was when Gannett took over Bel0. The following is an excerpt from the press release by Gannett:

“The transaction valuation implies a 9.4x average 2011/2012 EBITDA multiple prior to synergies, and a 5.4x multiple assuming expected synergies. “

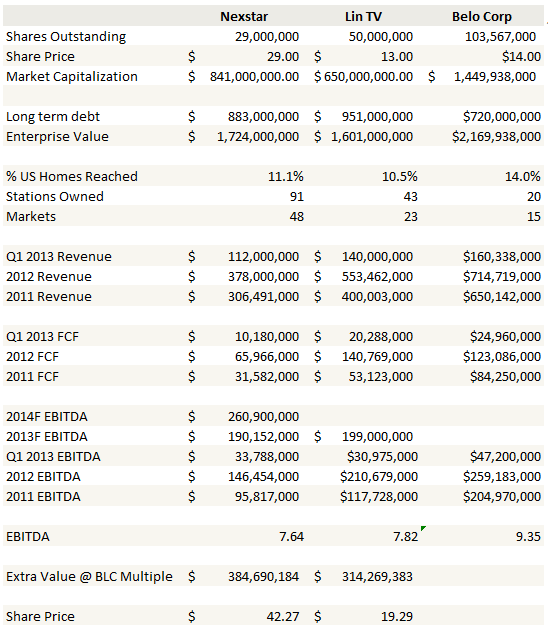

Based on the metrics of the Belo/Gannett transaction, a spreadsheet I made at the time I purchased LIN TV suggested it was significantly undervalued versus the transaction, and even now it remains somewhat undervalued. I have reposted that spreadsheet below. Note that I have left in the original share prices of each company from June when I did the work. With both LIN TV and Nexstar, my EBITDA estimates had to be based off of forecast numbers (which I’ve taken from brokerages that cover the stocks) because both companies have had significant accretive acquisitions so their past performance doesn’t reflect what earnings will be like going forward.

Based on these metrics I’m looking for something around $18-$19 to put LIN TV on par with the Gannett/Belo transaction.

Frozen Food Express and Inteliquent

There are two more stocks that I added in June, Frozen Food Express (FFEX) and Inteliquent (IQNT).

Most of my thesis with Inteliquent has already played itself out so I won’t talk about it too much here. At the time I added the stock it was trading at $5.75 and was about to release a special dividend of $1.25. Since that time the stock gave out the dividend, fell and then subsequently recovered to its current price of $5.90. At this level it is pretty close to what I had been hoping for, so I expect to sell my shares in the near future. Dedwardssays has a good summary of the investment idea behind Inteliquent here.

As for Frozen Foods Express, it’s a pretty straightforward idea. The company is (another) struggling trucker with some potential to turn things around as the economy improves. The stock is reasonably inexpensive based on its assets (at $1.75, which is what I purchased the stock at it is a little above the book value of $1.43).

But unlike YRC Worldwide, Frozen Food Express has really shown nothing to suggest that it is making progress towards profitability. Instead, what drove me into the stock were the overtures of the Duff Brothers, who are the CEO and Vice President of the private company Southern Tire Mart. More importantly, the Duffs own KLLM, a temperature-controlled nationwide carrier, and competitor of Frozen Food Express.

To recap the chronology of the Duff’s involvement in Frozen Food Express.

On March 4th the Duffs acquired 1,050,124 shares and said the following:

The Reporting Persons have expressed an intent to discuss with the Issuer a possible negotiated acquisition or other transaction between the Reporting Persons or an affiliate and the Issuer. The Reporting Persons intend to have further discussions and communications with the Issuer regarding a possible acquisition of the Issuer or other extraordinary corporate transaction, such as a merger; however, no commitment, binding or non-binding, has been made in accordance with such intention and no specific proposal has been made.

On May 8th the Duffs made a non-binding proposal:

Thomas Milton Duff and James Ernest Duff (the “Duffs”) made a non-binding proposal to the Special Committee of the Board of Directors of the Issuer (the “Special Committee”) to acquire all of the remaining issued and outstanding shares of the Issuer’s Common Stock not owned by the Reporting Persons. This non-binding proposal is subject to various conditions, includingg further due diligence. The Special Committee has not yet provided a response to this non-binding proposal.

On June 3rd, the Duffs said the following:

The Duffs continue to negotiate with the Issuer. As of the filing date of this Schedule, the plans or proposals of the Reporting Persons are otherwise consistent with previous disclosures.

While none of this suggests that its a done deal, things appear to be progressing in the right direction for an eventual take-over of the company. There is some good work done in this SeekingAlpha article to try to quantify what that takeover price might be, in particular the comparison to their closest publicly traded competitor, Marten Transport. The conclusion is that its likely to be above $2, which would be a nice profit from here.

MBIA

I sold out of MBIA because there is no immediate and clear catalyst. The stock never really approached the level I would have expected it to once the Bank of America settlement arrived. Based on the settlement I expected $18-$20 and the stock only briefly traded above $16. As the weeks passed by it became clear that the market had no intention of revaluing MBIA to its adjusted book value (which is above $30 per share) without further evidence of a viable, ongoing business.

I think the problem, which I admittedly did not consider during my adventures in the stock over the past 2 years, is that with rates as low as they are there is little need for municipalities and public works projects to get bond insurance. The rates they can obtain in the market are adequate. The market is therefore questioning what MBIA is going to do going forward. There is plenty of speculation about what that might be, and an announcement that the company is making endeavors into the mortgage business, for example, will undoubtably send the stock higher, but this remains a possibility more than a likelihood. The other possibility is that not much of anything happens at all and the stock sits at these levels for months (years?) to come. I lack the patience, and so I moved on.

Out of Impac Mortgage

Lastly, I sold out of Impac Mortgage (IMH).

![]()

I tweeted the following comment to summarize my thoughts:

I’ve talked in the past about my concern with gain on sale margins and refinancing volumes and how that will affect Impac’s earnings. I had been hoping that Impac would have some news, perhaps the diversification into a new mortgage businesses, that might offset the declines. But instead its been very quiet. Meanwhile, in June I spent a great deal of time researching PennyMac Mortgage (PMT), and the more I understood about their businesses (investing in distressed housing assets, mortgage servicing rights and correspondent lending with the eventual intent of securitizing their own non-agency loans) the more it became clear to me that PennyMac was already successfully operating in the areas that I was hoping Impac would begin to get into. It wasn’t a one for one trade but I did exit my position in Impac Mortgage and enter into my position in PennyMac at about the same time.

With the sale of Impac comes some humility. I was wrong about the stock. Back in October, when the company produced stellar earnings of $1.50 per share for the third quarter, I thought the stock could continue to produce earnings of this magnitude going forward and that I was looking at a potential 4-5 bagger. That turned out not to be the case.

I think the problem with my thesis lay in my lack of understanding of the origination business at the time, and I think that I have learned a lot since then. Perhaps the biggest eye-opener to me was a Lykken on Lending broadcast (which I can’t find at the moment) where comments were made about origination businesses being fairly sold for 2-3x earnings. This was followed up by Nationstar’s purchase of Greenlight Financial Services, an $8 billion originator in California and Nevada, for $75 million.

Clearly mortgage originators are valued at low multiples. It has low multiples because it has fairly low barriers to entry and is typically (though not recently) a very tight, low margin business. Thus, maybe it is reasonable for Impac Mortgage to trade at a low multiple. When you add to this realization the uncertainty surrounding the eventual level of gain on sale margins and origination volumes now that mortgage rates have risen, you arrive at reasons not to hold the stock. I will continue to keep an eye on Impac and if they announce details of expansion that look to gain them a foothold into other segments of the mortgage market, I will re-evaluate.

IMH is holding an increasing amount of MSRs now that they are not capital constrained. I realize more of their business is tied to origination (now) but it could change in the future. I am guessing that is why you exited the position and went more into the mortgage REITs?